Get the right experience for you. Please select your location and investor type.

Worldwide Leaders

The strategy was launched in November 2013. It invests in the shares of between 30-60 global companies.

A Leaders strategy generally invests in market leading companies which means, for this strategy, that they are valued at over US$5 billion.

You can see all of the companies that this strategy invests in by filtering on our Portfolio Explorer tool.

- We define investment risk as losing clients’ money – this means we focus on looking after your money as well as growing it

- Companies must contribute to sustainable development and make a positive impact towards a more sustainable future. Portfolio Explorer >

- We invest in high-quality companies with exceptional cultures, strong franchises and resilient financials. How we pick companies >

- We avoid companies linked to harmful activities and engage and vote for positive change. Our position on harmful products >

Quarterly updates

Strategy update: Q1 2025

Worldwide Leaders strategy update: 1 January - 31 March 2025

“Only two things make up a railroad: a track and a locomotive.” Amid the constant news about tariffs, trade wars and global political realignment, this recent comment – by the chief financial officer (CFO) of one of our companies – provided a timely reminder that things are sometimes simple. It also underscored why we are glad that our focus is on seeking to understand individual companies rather than trying to predict global events. Through all the noise of the first quarter of 2025, we focused on finding companies with experience in navigating unpredictable political and economic conditions and who keep their eyes firmly fixed on their long-term goals.

This quarter saw a significant ‘first’ for Worldwide Leaders – its first investment in a Chinese company - Alibaba (China: Consumer Discretionary). We approached our assessment of Alibaba as we would with any company, by considering the quality of its people, its franchise and its financials. Alibaba is led by a highly capable management team that combines a private-sector mindset alongside alignment with the goals of the Chinese government. It is reinvesting cashflows from its mature retail business in building a new cloud business. It has plenty of cash and a share-buyback programme (when a company buys back its own shares) that is friendly to smaller shareholders. In our view, the combination of an attractive valuation with the potential for Alibaba’s technology to help China meet some of the development challenges it faces provides a strong investment case.

We also added a new position in ABB (Switzerland: Industrials). This high-quality engineering business is a market leader in electrification, motion and automation. Its motors, drives and transformers are a small but critical part of its customers’ overall budget, and the depth of the relationships ABB has fostered with them puts it in a strong competitive position. We believe the combination of increasing demand for electricity worldwide and the company’s focus on improving profits puts ABB in a good position to perform well over the next 10 years.

We continued to grow the size of our holding in a number of recent additions such as Brown & Brown (United States: Financials), NVR (United States: Consumer Discretionary) and Carlisle Companies (United States: Industrials). The attractive valuation of Samsung Electronics (South Korea: Information Technology) also encouraged us to add to our position.

During the quarter, we sold Costco (United States: Consumer Staples). This is still a high-quality company but the high valuation of its shares suggested that future returns may be lower. On a similar note, we also trimmed the size of our holdings in Fortinet (United States: Information Technology), Copart (United States: Industrials) and Watsco (United States: Industrials) due to high valuations. Rising global political risks led us to trim the size of our holding in TSMC (Taiwan: Information Technology).

We continue to find opportunities to invest in the shares of reasonably valued companies from around the world that we believe can (profitably) help to solve a range of development challenges. Our focus on individual companies allows us to capture those opportunities wherever they arise. At a time of rapid economic and political change, we continue to apply our investment philosophy consistently and to focus on the things that we believe matter over our investment timeframe. As for what comes next? Another comment from the CFO we quoted earlier sums up our view: “there’s only one way to go in rail, and that’s forward!”

Source for company information: Stewart Investors investment team and company data. This stock information does not constitute any offer or inducement to enter into any investment activity. Portfolio data shown is from representative strategy accounts of the strategy shown above. Named new investments disclosed relate to holdings with a portfolio weight over 0.5%. It is not a recommendation or solicitation to purchase or invest in any fund. Differences between the representative account-specific constraints, currency or fees and those of a similarly managed fund or mandate would affect results.

Strategy update: Q4 2024

Worldwide Leaders strategy update: 1 October - 31 December 2024

“We are allocating our own money, we act like owners.”1 It’s always pleasing to meet with a company that thinks similarly to us. We are stewards of our clients’ capital, aiming to look after our clients’ savings as well as we would look after our own. Our Hippocratic Oath is is our pledge as an investment team to uphold the principle of stewardship through our conduct and work practices. One key point in the oath is “We will not forget in our search for returns that the primary risk faced by our clients is losing their capital”. The oath underpins our investment philosophy, which is based on identifying quality leaders and stewards of strong business franchises with good long-term growth prospects.

During the quarter we bought five new companies and the quote above is from a meeting with the company management of the first of them. Brown & Brown (United States: Financials) was founded in 1939 and is still led and stewarded by the Brown family. Over the past 85 years, the competent, ambitious and long-term management team has enabled it to grow beyond its Florida base to become the sixth largest insurance broker2 in the United States. The company has also been expanding to Asia and Europe and as the insurance brokerage industry is made up of many small companies, there is plenty more room to grow in the decades ahead.

Carlisle Companies (United States: Industrials) make and sell construction materials, particularly the products needed to roof and waterproof buildings. Using high-quality products in houses leads to better ventilation and protection from weather as well as reducing energy usage and improving longevity. The high demand for new housing across America will provide strong long-term growth opportunities for this company as well as another new purchase, NVR (United States: Consumer Discretionary). Based in Virginia, NVR is the fourth largest homebuilder3 in the United States, focused on building high-quality homes for first-time owners. The management team have lots of experience and a history of using periods of slowdown in the industry to expand their business in a controlled way. This allows them to benefit when housing demand increases.

Wabtec (United States: Industrials) is a leading provider of components for rail transportation and can trace its roots back over 100 years. The rail industry is as important now as it was then, as it plays a crucial role in reducing global carbon emissions in both commercial freight and passenger transportation. Rising investment in rail infrastructure along with Wabtec’s increasing position size in the market and improving profits provide positive long-term opportunities for growth.

Synopsys (United States: Information Technology) is the market leader4 in software for the design of semiconductors, with their products being used by almost all major semiconductor designers and manufacturers. The founder continues to lead and steward the company as Chairman of the Board, enabling them to make long-term investments in research & development (R&D). This ensures that their products remain relevant for decades and also provides excellent growth potential.

The new positions were funded by selling Edwards Lifesciences (United States: Health Care) which manufacturers artificial heart valves and Halma (United Kingdom: Information Technology) which holds a portfolio of companies targeting solutions for safety, health, environment and testing. In both cases, we felt that there were greater opportunities for growth in other companies.

The US election took place in November, sending Donald Trump back to the White House along with a Republican Party majority in the House of Representatives and the Senate. There have been many news stories written about taxes, tariffs and other general speculation about what the incoming administration might do. We don’t have any insights into the workings of a Trump presidency, instead, we focus on finding companies that are good at navigating difficult situations and experienced at generating growth from the opportunities in front of them. Another point of our Hippocratic Oath is “We will strive to achieve, through hard work, sober analysis and sound judgement, the best risk-adjusted returns possible for our clients.” This focus means we will continue to seek companies like, Brown & Brown, who we believe will be excellent stewards of our clients’ savings.

[1] Source: Stewart Investors company meeting with Brown & Brown, February 2024.

[2] Source: Brown & Brown website - https://www.bbrown.com/us/about/

[3] Source: Builder. https://www.builderonline.com/builder-100/builder-100-list/2023/

[4] Source: Synopsys company data - https://s201.q4cdn.com/778493406/files/doc_earnings/2024/q4/presentation/InvestorOverviewPresentationFinal-Q4.pdf

Source for company information: Stewart Investors investment team and company data. This stock information does not constitute any offer or inducement to enter into any investment activity. Portfolio data shown is from representative strategy accounts of the strategy shown above. Named new investments disclosed relate to holdings with a portfolio weight over 0.5%. It is not a recommendation or solicitation to purchase or invest in any fund. Differences between the representative account-specific constraints, currency or fees and those of a similarly managed fund or mandate would affect results.

Strategy update: Q3 2024

Worldwide Leaders strategy update: 1 July - 30 September 2024

We bought one new company during the quarter. Rentokil Initial (United Kingdom: Industrials) is a global leader in pest control services, a necessary and critical health and hygiene service to secure homes, hospitals and businesses against disease and damage.

Its business model is local in nature and generates lots of income through resilient and regular, repeating sales. The management team is focused on growth by increasing the density of its route network to drive improvements in profitability and earnings.

During the quarter we sold completely out of four companies as we grew concerned about their ability to grow their end customer markets. These include: Midea (China: Consumer Discretionary) which makes home appliances for the Chinese market; Infineon Technologies (Germany: Information Technology) which makes semiconductors for electric vehicle and renewable energy markets; Hamamatsu Photonics (Japan: Information Technology) which makes equipment to generate, detect and filter light for scanners, x-ray machines and automation devices such as barcode readers; and Graco (United States: Industrials) which specialises in paint sprayers and products that manage corrosive and other difficult-to-handle fluids.

We are always looking at new companies and recently visited Sweden to meet with some new and some old businesses, including Atlas Copco (Sweden: Industrials), the world's leading manufacturer of air compressors, which is held in the strategy. The opportunity to meet with company management on their ‘home turf’ is invaluable; it is much easier to get a sense of how culture and people have shaped a company and its future return profile when sitting within their offices; or, in the case of Atlas Copco, 20 metres below their office in a test mine. We continue to find excellent investment ideas by focussing on the impact that outstanding people can have on businesses with strong business franchises and resilient financials.

Source for company information: Stewart Investors investment team and company data. This stock information does not constitute any offer or inducement to enter into any investment activity. Portfolio data shown is from representative strategy accounts of the strategy shown above. Named new investments disclosed relate to holdings with a portfolio weight over 0.5%. It is not a recommendation or solicitation to purchase or invest in any fund. Differences between the representative account-specific constraints, currency or fees and those of a similarly managed fund or mandate would affect results.

Strategy update: Q2 2024

Worldwide Leaders strategy update: 1 April - 30 June 2024

“We know we’re not going to get our money out, so we’d rather burn it up in paying our employees1”.

For Lincoln Electric (United States: Industrials), getting out the Russian market was an easy decision, the only question was how. They stopped production in April 2022 and have focused on supporting their former employees as they look for options to divest their facility. Meeting with companies in person helps us to understand the quality of management through the decisions that they take.

We recently visited the United States to meet with a wide range of industrial and consumer companies across Chicago, Cincinnati, Columbus, Cleveland, Boston and New York. In total we met with 50 companies, many of them leaders in their industries. We highlight some of the companies we met with in more detail here along with the reasons why we believe they fit so well with our investment approach. The trip was a great reminder of the number of excellent companies out there with competent and ethical company leaders that generate returns by focusing on building long-term business franchises in profitable niches.

During the quarter we added a new position in Ashtead Group (United Kingdom: Industrials), an industrial and construction equipment rental company with a long-tenured leadership team. Despite being founded in the UK in 1947, Ashtead Group currently derives more than 80% of its sales from the United States. This comes from its company Sunbelt, which it bought in the 1990s1. Renting equipment reduces the need for companies to own equipment that sits idle and leads to improved resource efficiency and reduced environmental impact. The rental equipment market is currently divided among many smaller providers which offers room for successful businesses to grow. We continued to add to our position in TSMC (Taiwan: Information Technology) reflecting our confidence in the long-term potential of its business. We also added to positions in MonotaRO (Japan: Industrials), Fortinet (United States: Information Technology) and Old Dominion Freight Line (United States: Industrials).

We sold two companies, Samsung C&T (South Korea: Industrials) and EPAM Systems (United States: Information Technology), in preference for other ideas. We also trimmed exposure to Mahindra & Mahindra (India: Industrials), and Infineon Technologies (Germany: Information Technology).

During the quarter, one of our companies was targeted by an activist investor (an individual/group that buys a large number of a company's shares and uses that ownership to put pressure on the company and change how it is managed) who was concerned that the company was overbuilding manufacturing capacity. Their concerns were based on near-term sales expectations in an industry that is expected to grow by multiples in the coming years. We disagreed as the company’s record during economic down periods and industry leading investments has handsomely rewarded patient shareholders. We wrote to offer them our support.

The market concentration we highlighted last quarter shows no sign of reducing with continuing excitement about any company connected with building Artificial Intelligence (AI) infrastructure. We do not know how new technologies work through an economy or where the main sales or profits will appear. Instead of focusing on a single growth driver, we aim to build a portfolio of companies that can benefit from a variety of diverse growth drivers, as we believe that this is the best way to protect and grow over the long term.

1 Source: Stewart Investors investment team and company data

Source for company information: Stewart Investors investment team and company data. This stock information does not constitute any offer or inducement to enter into any investment activity. Portfolio data shown is from representative strategy accounts of the strategy shown above. Named new investments disclosed relate to holdings with a portfolio weight over 0.5%. It is not a recommendation or solicitation to purchase or invest in any fund. Differences between the representative account-specific constraints, currency or fees and those of a similarly managed fund or mandate would affect results.

Proxy voting

Proxy voting: Q1 2025

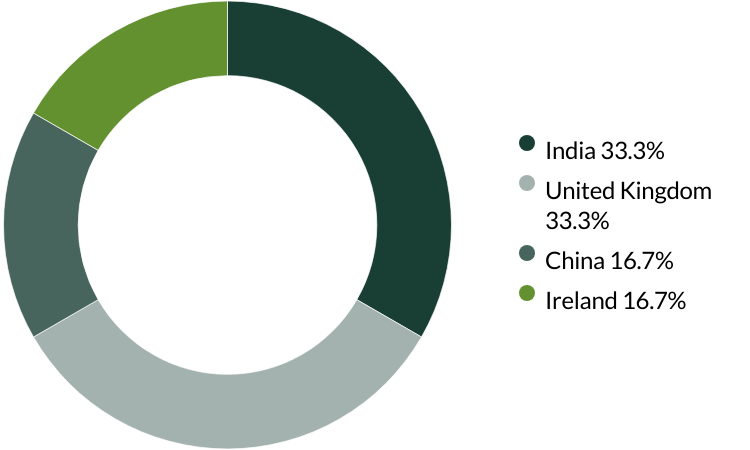

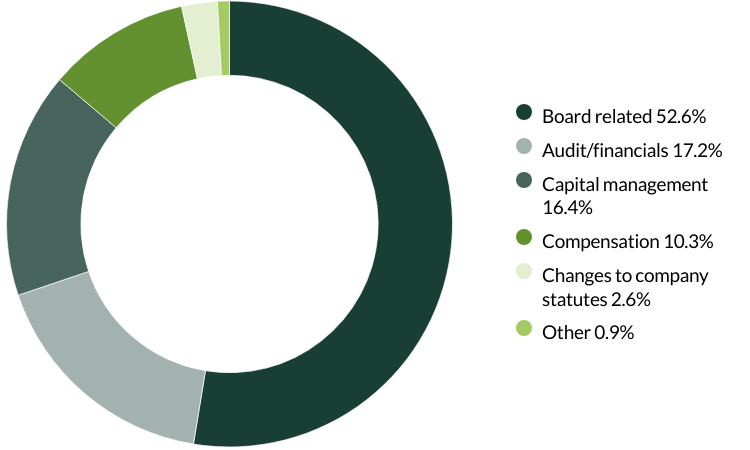

Worldwide Leaders proxy voting: 1 January - 31 March 2025

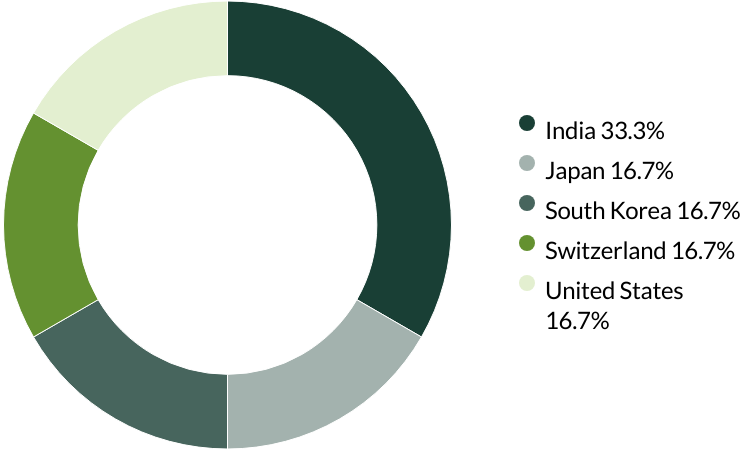

Proxy voting by country of origin

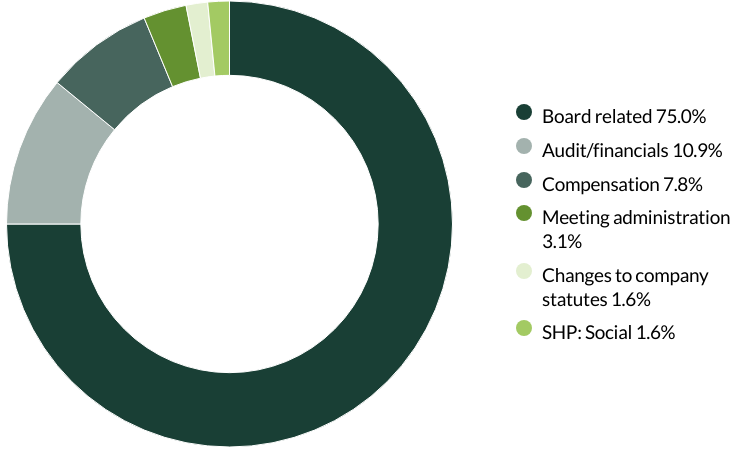

Proxy voting by proposal category

During the quarter there were 64 resolutions from five companies to vote on. On behalf of clients, we voted against six resolutions.

We voted against a proposal on transaction of business at ABB, as they did not provide enough information about the proposal. We wanted to avoid giving them unrestricted decision-making power without sufficient clarity. (one resolution)

We voted against the appointment of the auditor at Costco as they have been in place for over 10 years. The company has given no information on intended rotation, which we believe is important to provide a fresh perspective on the accounts. We voted against a shareholder proposal requesting the company publish a report assessing the risks of maintaining its current diversity, equity and inclusion (DEI) roles, policies and goals as we support the company in their commitment to obey with the law and that their DEI efforts are legally appropriate. (two resolutions)

We voted against the election of two directors and an audit committee member at Samsung Electronics as we do not believe them to be truly independent. (three resolutions)

Source for company information: Stewart Investors investment team and company data. This stock information does not constitute any offer or inducement to enter into any investment activity. Portfolio data shown is from representative strategy accounts of the strategy shown above. Proxy voting chart numbers may not add to 100 due to rounding. SHP means: Shareholder Proposal.

Proxy voting: Q4 2024

Worldwide Leaders proxy voting: 1 October - 31 December 2024

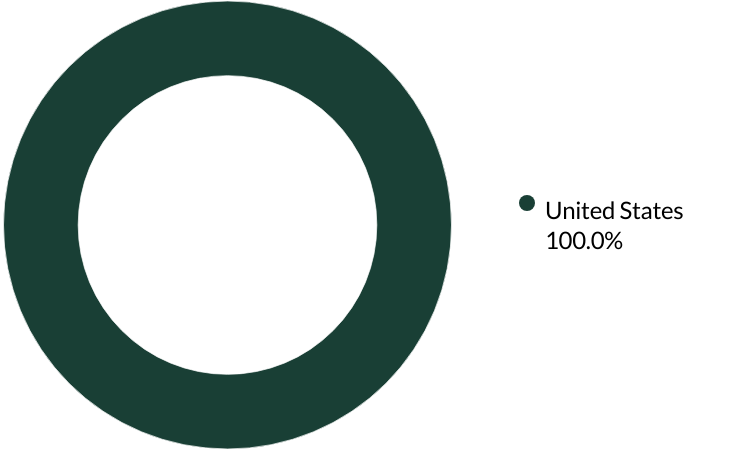

Proxy voting by country of origin

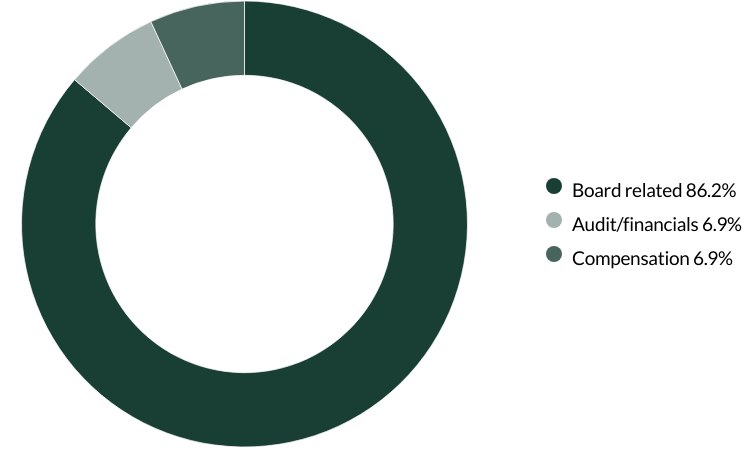

Proxy voting by proposal category

During the quarter there were 25 resolutions from two companies to vote on. On behalf of clients, we voted against one resolution.

We voted against the re-appointment of the auditor at Copart as they have been in place for or over 10 years and the company has given no information on intended rotation which we believe is important for ensuring a fresh perspective on the accounts. (one resolution)

Source for company information: Stewart Investors investment team and company data. This stock information does not constitute any offer or inducement to enter into any investment activity. Portfolio data shown is from representative strategy accounts of the strategy shown above. Proxy voting chart numbers may not add to 100 due to rounding. SHP means: Shareholder Proposal.

Proxy voting: Q3 2024

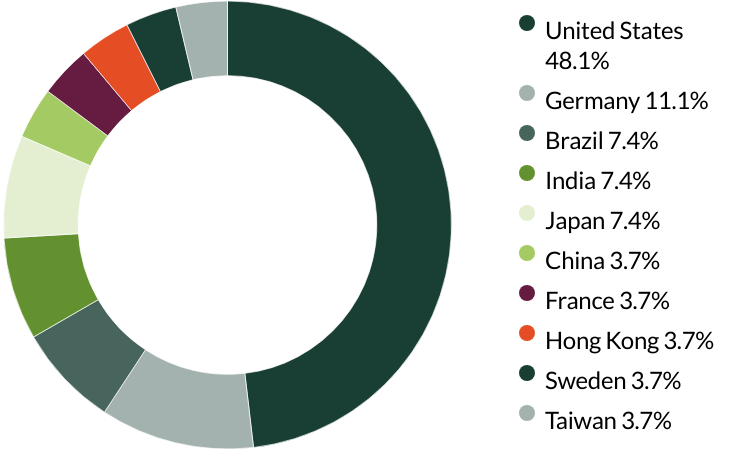

Worldwide Leaders proxy voting: 1 July - 30 September 2024

Proxy voting by country of origin

Proxy voting by proposal category

During the quarter there were 116 resolutions from six companies to vote on. On behalf of clients, we voted against four resolutions.

We voted against remuneration motions at Ashtead Group as we were concerned about excesses in CEO salary. (two resolutions)

We voted against the appointment of the auditor at Linde as they have been in place for over ten years. The company has given no information on intended rotation which we believe is important for ensuring a fresh perspective on the accounts. (two resolutions*)

*The same proposal was voted on different stock lines.

Source for company information: Stewart Investors investment team and company data. This stock information does not constitute any offer or inducement to enter into any investment activity. Portfolio data shown is from representative strategy accounts of the strategy shown above. Proxy voting chart numbers may not add to 100 due to rounding. SHP means: Shareholder Proposal.

Proxy voting: Q2 2024

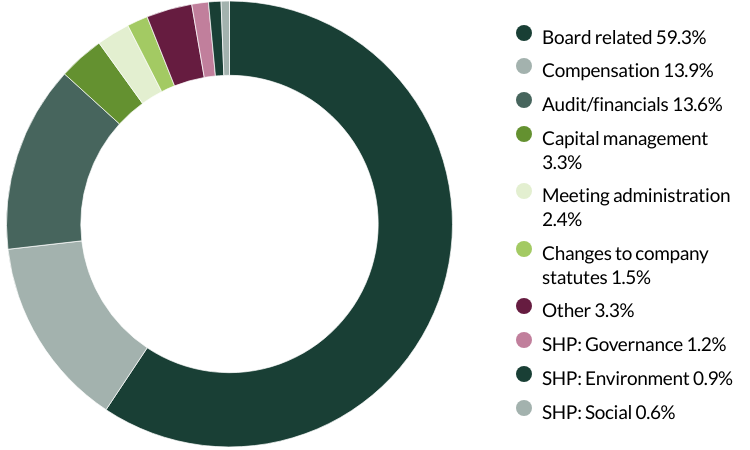

Worldwide Leaders proxy voting: 1 April - 30 June 2024

Proxy voting by country of origin

Proxy voting by proposal category

During the quarter there were 332 resolutions from 26 companies to vote on. On behalf of clients, we voted against 23 resolutions.

We voted against the appointment of the auditor at Arista Networks, bioMérieux, Edwards Lifesciences, EPAM Systems, Expeditors, Fastenal, Fortinet, Graco, Lincoln Electric, Markel, Old Dominion Freight Line, Roper Technologies and Texas Instruments as they have been in place for over 10 years and the companies’ have given no information on intended rotation. We believe rotating an auditor on a relatively frequent basis (e.g. every 5-10 years) helps to ensure a fresh pair of eyes are examining the accounts, and follows best practice. (13 resolutions)

We voted against the proposed employee stock ownership plan at Midea as we believe that involving non-executive directors in the plan could create conflicts of interest and would not be in the best interest of the shareholders. (three resolutions)

We voted against recasting (where previously cast votes on a particular matter are reconsidered or revised) and cumulative voting at WEG as this would allow the board to make changes without shareholder assessment or knowledge of the candidates. (three resolutions)

We abstained from voting on requests for a separate board election and the election of a supervisory council position at WEG as there was not enough information and we would prefer the current family stewards remain in place. (two resolutions)

We voted against a shareholder proposal about board declassification at EPAM Systems as we do not believe it is necessary for all directors to stand for election annually and have concerns that this could destabilise the board by allowing excessive turnover. (one resolution)

We voted for a shareholder proposal encouraging alignment with the Paris Agreement and greenhouse gas (GHG) emissions targets. We voted against a shareholder proposal requesting a diversity & inclusion report at Expeditors as we believe this issue requires wider discussion and cannot be resolved through disclosure alone. (two resolutions)

We voted against a shareholder proposal on simple majority voting at Fastenal as it was covered by the company's own proposals. (one resolution)

We voted against a shareholder proposal on GHG emissions disclosure at Markel as the proposal called for disclosure of emissions from underwriting, insuring and investments, which is not yet widely reported or reliably reported in the insurance industry. We would prefer to discuss the issue with the company. (one resolution)

We abstained from voting on a shareholder proposal on the adoption of greenhouse gas (GHG) emissions targets aligned with the Paris Agreement at Old Dominion Freight Line. We have previously engaged with the company on this issue and prefer to continue this dialogue directly. (one resolution)

We abstained from voting on a shareholder proposal to remove supermajority requirements for certain issues at Roper Technologies as the board didn't provide a recommendation. (one resolution)

We voted for shareholder proposals on the right to call a special meeting and requesting a report on customer due diligence at Texas Instruments as we found both proposals to be sensible. (two resolutions)

Source for company information: Stewart Investors investment team and company data. This stock information does not constitute any offer or inducement to enter into any investment activity. Portfolio data shown is from representative strategy accounts of the strategy shown above. Proxy voting chart numbers may not add to 100 due to rounding. SHP means: Shareholder Proposal.

Sustainable investment labels help investors find products that have a specific sustainability goal. This product does not have a UK sustainable investment label as it does not have a non-financial sustainability objective. Its objective is to achieve capital growth over the long-term by following its investment policy and strategy.

Portfolio Explorer

If you are unable to view the portfolio explorer, please re-open in Google Chrome, Edge, Firefox, Safari or Opera. IE11 is not supported.

For illustrative purposes only. Reference to the names of example company names mentioned in this communication is merely for explaining the investment strategy and should not be construed as investment advice or investment recommendation of those companies. Companies mentioned herein may or may not form part of the holdings of Stewart Investors. Holdings are subject to change.

Certain statements, estimates, and projections in this document may be forward-looking statements. These forward-looking statements are based upon Stewart Investors’ current assumptions and beliefs, in light of currently available information, but involve known and unknown risks and uncertainties. Actual actions or results may differ materially from those discussed. Readers are cautioned not to place undue reliance on these forward-looking statements. There is no certainty that current conditions will last, and Stewart Investors undertakes no obligation to correct, revise or update information herein, whether as a result of new information, future events or otherwise.

Source: Stewart Investors investment team and company data. Securities mentioned are all investee companies* from representative Asia Pacific All Cap Strategy, Asia Pacific & Japan All Cap Strategy, Asia Pacific Leaders Strategy, European All Cap Strategy, European (ex UK) All Cap Strategy, Global Emerging Markets (ex China) Leaders Strategy, Global Emerging Markets Leaders Strategy, Global Emerging Markets All Cap Strategy, Indian Subcontinent All Cap Strategy, Worldwide All Cap Strategy and Worldwide Leaders Strategy accounts as at 31 March 2025. *Assets that the strategies may hold which an active decision has not been made, and sustainability assessment does not apply, include cash, cash equivalents, short-term holdings for the purpose of efficient portfolio management and holdings received as a result of mandatory corporate actions. Holdings of such assets will not appear on Portfolio Explorer.

The Stewart Investors supports the Sustainable Development Goals (SDGs). The full list of SDGs can be found on the United Nations website.

Source for Climate Solutions and impact figures: © 2014–2025 Project Drawdown (drawdown.org). Source for Human Development Pillars: Stewart Investors investment team.

Source for climate solutions and human development analysis and mapping: Stewart Investors investment team. Contributions are defined by the team as demonstrable contributions to any solution, either direct (directly attributable to products, services or practices provided by that company), or enabling (supported or made possible by products or technologies provided by that company).

Investment terms

View our list of investment terms to help you understand the terminology within this website.

Fund data and information

Key documents

Fund prices and details

Click on the links below to access key facts, literature, performance and portfolio information for the funds and share classes available in this jurisdiction:

Stewart Investors Worldwide Leaders Fund

| Fund name | Fund type | Currency | Price | Daily change | Price date | Factsheet |

|---|---|---|---|---|---|---|

| Stewart Investors Worldwide Leaders Class I (Acc) | Irish UCITs | USD | 20.68 | -0.05 | 09 May 2025 | |

| Stewart Investors Worldwide Leaders Class III (Acc) | Irish UCITs | USD | 17.57 | -0.04 | 09 May 2025 | |

| Stewart Investors Worldwide Leaders Class A (Acc) | OEIC | GBP | 709.24 | -0.14 | 09 May 2025 | |

| Stewart Investors Worldwide Leaders Class B (Acc) | OEIC | GBP | 851.49 | -0.14 | 09 May 2025 |

Share prices are calculated on a forward pricing basis which means that the price at which you buy or sell will be calculated at the next valuation point after the transaction is placed. Where a fund price is marked XD, this means that the fund is currently Ex-Dividend. Past performance is not necessarily a guide to future performance. The value of shares and income from them may go down as well as up and is not guaranteed. Please note that the yield quoted above is not the historic yield. It is considered that the yield quoted represents the current position of investments, income and expenses in the fund and that this is a more accurate figure. Investors may be subject to tax on their distribution. The yield is not guaranteed or representative of future yields. You should be aware that any currency movements could affect the value of your investment. The Funds within the First Sentier Investors Global Umbrella Fund plc (Irish VCC) are denominated in USD or EUR.

Strategy and fund name changes

As of end of 2024, please note that Stewart Investors strategies and the Funds within the UK First Sentier Investors ICVC, First Sentier Investors Global Umbrella Fund plc (Irish VCC) and First Sentier Investors Global Growth Funds (Singapore Unit Trust) have been renamed. Please refer to our note via the link below for further information.