Get the right experience for you. Please select your location and investor type.

Global Emerging Markets All Cap

The Global Emerging Markets All Cap strategy invests in between 30-75 high-quality companies that are contributing to a more sustainable future.

Download overviewOur Global Emerging Markets All Cap strategy was launched in 2009 and invests in between 30 to 75 high-quality companies that are contributing to a more sustainable future. The strategy’s bottom-up approach allows us to find only the very best businesses from an investable universe of some 65,000 companies. We are looking for companies well positioned to contribute to long-term sustainable development; businesses with high quality management teams, franchises, and financials.

Strategy highlights: a focus on quality and sustainability

- Companies must contribute to sustainable development. Portfolio Explorer >

- We invest in high-quality companies with exceptional cultures, strong franchises and resilient financials. How we pick companies >

- We avoid companies linked to harmful activities and engage and vote for positive change. Our position on harmful products >

- Our approach is long-term, bottom-up, high conviction and benchmark agnostic

- We focus on capital preservation as well as capital growth – we define risk as the permanent loss of client capital

Latest insights

Quarterly updates

Strategy update: Q2 2025

Global Emerging Markets All Cap strategy update: 1 April - 30 June 2025

The announcement of President Trump’s ‘Liberation Day’ tariffs on 2 April and the short, sharp trade war with China that followed ensured a volatile start to the quarter for emerging markets.

The uncertainty drove share prices sharply lower until the announcement of a 90-day pause on the introduction of the tariffs helped to calm investors. That calm endured even when Israel took direct military action against Iran, with the oil price spiking higher only briefly. Perhaps the most interesting development from our perspective, however, was that the US dollar had its weakest start to the year since 19731. We think the pressure on the dollar could persist and may, in time, encourage capital to flow into emerging markets.

We added two new holdings over the quarter: one in China, one in India. Trip.com (China: Consumer Discretionary) is the country’s largest online travel-booking platform. The company’s founders remain involved in the business and have seen it grow organically as well as through mergers and acquisitions. It survived the dead stop in tourism prompted by the covid pandemic and now seems primed to take advantage of a shift to booking travel online. Although only about 10% of the Chinese population currently has a passport that proportion is expected to increase2. The second addition this quarter was Motilal Oswal Financial Services (India: Financials), a diversified financial-services conglomerate operating in retail and institutional broking, asset management, wealth management, investment banking, and housing finance with an ambitious-but-conservative steward at its helm. It should benefit from meeting the needs of India’s growing middle class. We also continued to build our positions in Cholamandalam Financial Holdings (India: Financials), Alibaba (China: Consumer Discretionary) and Naver (South Korea: Communication Services).

Set against that, we sold EPAM Systems (United States: Information Technology). We have become increasingly concerned about the outlook for IT services businesses, particularly those with a significant level of exposure to the US. EPAM produced a solid set of first-quarter results and its management upgraded their guidance on revenues for the rest of 20253. Despite this, we see a risk that its clients postpone or cancel investments in their IT systems due to the uncertainties currently facing the US economy. As part of our ongoing review of this sector, we also trimmed the holding in Globant (Argentina: Information Technology). We understand the argument that some companies will need IT services businesses to help them to adopt and integrate artificial intelligence (AI) tools. Equally, it may be that its clients actually replace their existing IT services with AI. Elsewhere, we sold Syngene (India: Health Care) and Dr. Lal PathLabs (India: Health Care) to finance additions to other, higher-conviction ideas.

Looking ahead, any renewed weakness in the dollar could be the trigger for capital currently domiciled in the US to begin to flow into emerging markets. We remain particularly positive on the prospects for high-quality companies in India. The central bank recently started cutting interest rates, which should support demand in rural India. Towards the end of the quarter, we attended a conference of Indian companies and were struck by how positive all of them were about the growth opportunities ahead of them over the next 10 years. In our view, this potential growth – and the size of the Indian market – continues to offer powerful support to valuations.

[1] Source: Financial Times, 30 June 2025 ‘US dollar suffers worst start to year since 1973’.

[2] Source: Straits Times, 21 December 2023 ‘China is world’s second-largest economy but its passport is ranked 63rd. Are things looking up?’.

[3] Source: EPAM ‘EPAM Reports Results for First Quarter 2025 and Raises Full Year Revenue Outlook’.

Source for company information: Stewart Investors investment team and company data. This stock information does not constitute any offer or inducement to enter into any investment activity. Portfolio data shown is from representative strategy accounts of the strategy shown above. Named new investments disclosed relate to holdings with a portfolio weight over 0.5%. It is not a recommendation or solicitation to purchase or invest in any fund. Differences between the representative account-specific constraints, currency or fees and those of a similarly managed fund or mandate would affect results.

Download a PDF copy

Select Strategy update and/or Proxy voting to produce a report. You can then download a copy of the report by clicking on the button.

You can build a bespoke report for all our strategies on the full Quarterly update report.

Strategy update: Q1 2025

Global Emerging Markets All Cap strategy update: 1 January - 31 March 2025

With the threat of US tariffs ever present, the volatility seen across emerging markets in the final quarter of 2024 carried over into 2025. Share prices in India fell sharply due to concerns about a cyclical slowdown. China, by contrast, performed well as investors anticipated a reacceleration in economic growth and began to identify value in many parts of the market. Sentiment was also supported by President Xi, who met executives from a number of private-sector companies.

We added eight new names to the portfolio and sold six. Although it is unusual to see so many names entering and exiting the portfolio, turnover as a percentage of assets under management remained low, at around 9%1. We were, in essence, simply tidying up a number of our smaller positions – the ‘tail’ of the portfolio.

In China, we sold out of Glodon (China: Information Technology) and Hangzhou Robam (China: Consumer Discretionary). These sales were informed by our view of the country’s property market, where we don’t see the issue of oversupply being resolved any time soon. Glodon provides software for construction and development companies. The majority of Hangzhou Robam’s appliances, meanwhile, are sold to housing developers. These sales also allowed us to reallocate the capital to new investment ideas such as Alibaba (China: Consumer Discretionary), S.F. Holding (China: Industrials) and Mindray (China: Health Care).

Alibaba is one of China’s leading e-commerce platforms. It is using the strength of its balance sheet to invest in building its AI capabilities. S.F. Holding has grown into one of China’s leading logistics businesses since its founding in 1992. Its founder remains involved in the day-to-day management of the company. Mindray is a leading medical company. As trade barriers are thrown up around the world, it has the potential to benefit should there be a shift in China towards buying domestically sourced products.

We also added some new names in India while trimming back some others. Share prices in India sold off as the country appeared to be entering a cyclical slowdown. In response, the central bank cut interest rates for the first time since the Covid pandemic in 2020. Valuations in some parts of the market, meanwhile, had begun to appear excessive. We sold out of Godrej Consumer Products (India: Consumer Staples) because it was too expensive for the growth it offered. We sold out of Bajaj Housing Finance (India: Financials) because of liquidity constraints and reallocated the capital into its asset-lite holding company, Bajaj Holdings & Investment (India: Financials) while also establishing a position in sister company Bajaj Auto (India: Consumer Discretionary), a leading manufacturer of motorcycles, scooters and auto rickshaws backed by a high-quality steward.

Other new names in India included Cholamandalam Financial Holdings (India: Financials) and Triveni Turbines (India: Industrials). Cholamandalam is another business associated with the Muragappa family, who we believe to be good stewards of capital. Triveni Turbines, meanwhile, is a leading maker of steam turbines.

We also added a position in Walmart de Mexico (‘Walmex’) (Mexico: Consumer Staples). With the market having taken fright from the elections of Claudia Sheinbaum (in April 2024) and then Donald Trump (in November), Walmex shares had fallen to their lowest multiple since 1996. Despite this, we believe it remains a solid, dependable long-term growth story. The final new name was BDO Unibank (Philippines: Financials) which is the largest bank in the country with a good opportunity to grow in the outlying islands and by developing its digital offering2. We sold Koh Young Technology (South Korea: Information Technology), following a number of missteps in execution and a miss on earnings. We also sold Unicharm (Japan: Consumer Staples). While it has pivoted to adult diapers in response to demographic change, it has found this shift harder than it had originally envisaged.

While we are broadly positive on the outlook for emerging markets, we recognise that there is likely to be ongoing volatility for as long as ‘top-down’ uncertainty – inspired by trade tariffs and geopolitical flux – remains at elevated levels. Valuations are certainly attractive and there remains plenty of domestically driven growth in the markets we favour. Our task is to block out the short-term noise to focus on the underlying quality, growth and stewardship of the companies we invest in.

[1] Source: FactSet as of 31 March 2025.

[2] Source : BDO Unibank – Company Profile (as of 31 December 2024).

Source for company information: Stewart Investors investment team and company data. This stock information does not constitute any offer or inducement to enter into any investment activity. Portfolio data shown is from representative strategy accounts of the strategy shown above. Named new investments disclosed relate to holdings with a portfolio weight over 0.5%. It is not a recommendation or solicitation to purchase or invest in any fund. Differences between the representative account-specific constraints, currency or fees and those of a similarly managed fund or mandate would affect results.

Strategy update: Q4 2024

Global Emerging Markets All Cap strategy update: 1 October - 31 December 2024

Emerging markets ended 2024 lagging developed markets for the second year in a row. Whilst the MSCI Emerging Markets Index returned 8.1% (USD, total return), developed markets, measured by the MSCI World Index were up 19.2%, driven by strong performance in the United States. Brazil (-29.5%) and Mexico (-26.8%) both had a tough year in 2024 but China, India and Taiwan all posted positive returns1.

Through the last quarter of 2024, markets had to contend with the re-election of Donald Trump and all the expected geopolitical noise that will come over the next four years, as well as the continuing strength of the US dollar. We remain focused on bottom-up stock picking which is at the core of our portfolio construction process and we will continue to seek out long-term growth opportunities regardless of who is the President in the White House.

We added one new position and sold out of two companies through the quarter. We have built a position in Naver (South Korea: Communication Services), the leading South Korean internet search engine with a very strong market share. It was founded inside Samsung SDS before being spun out on its own in 1999. It is still run by the founder, Lee Hae-jin who has recently brought in a new management team which is aiming to return the company to a path of steady and profitable growth. One key aim for them is to use the stickiness of their search engine client base to drive increased e-commerce down the same channels. Their e-commerce business is the second largest in South Korea2. Naver’s attractive valuation presented a good opportunity to invest in a business that should achieve double-digit earnings growth each year.

We sold out of two positions, one of which is Advanced Energy Solution (Taiwan: Industrials). The company makes battery module units for e-bikes and backup servers and after a tough few years, management announced that they could see light at the end of the tunnel with demand from artificial intelligence (AI) coming through from their server clients. We have repeatedly asked for an update call with management without success. Given this lack of communication, we find it difficult to build conviction and have therefore exited the position. We added to Samsung Electronics (South Korea: Information Technology) and AirTAC International (Taiwan: Industrials) with some of the proceeds of this sale.

We also sold Kotak Mahindra Bank (India: Financials) through the quarter. Earlier in the year the bank came under increased regulatory scrutiny because of some lapses in IT security and they were forced to pause issuing some credit cards. Since then, we have had several meetings with the company which have led us to believe that they may continue to struggle especially as competitor public sector banks continue to show marked improvements. We believe there are better opportunities elsewhere in India.

We continue to look for high-quality companies which we can buy at reasonable valuations. We believe that valuations in emerging markets are now at very attractive levels alongside long-term growth opportunities that we can back for the next decade. The team is planning many research trips for 2025 to seek out new investment opportunities and update our knowledge of existing holdings. We look forward to sharing more with you as the year progresses.

1 Source: MSCI Index Factsheets as at 31 December 2024. All data USD, total returns.

2 Source: External market research.

Source for company information: Stewart Investors investment team and company data. This stock information does not constitute any offer or inducement to enter into any investment activity. Portfolio data shown is from representative strategy accounts of the strategy shown above. Named new investments disclosed relate to holdings with a portfolio weight over 0.5%. It is not a recommendation or solicitation to purchase or invest in any fund. Differences between the representative account-specific constraints, currency or fees and those of a similarly managed fund or mandate would affect results.

Strategy update: Q3 2024

Global Emerging Markets All Cap strategy update: 1 July - 30 September 2024

Most of the quarter’s activity happened in September, as is often the case. It is in such moments, like the biggest market moves since 2009 in China and Hong Kong and rising geopolitical tensions in the Middle East, that we remain grateful for our long-term philosophy. It gives us the ability to step back in moments of such volatility and reminds us to focus on the more important, bottom-up drivers for the companies we own on your behalf.

Over the course of the quarter, we have sold out of one of our Indian banks. RBL Bank (India: Financials), which we purchased in December 2023. The new management team seemed determined to move the bank towards less risky (more secured) lending which at 1x price-to-book (P/B)1 appeared attractively priced. Unfortunately, the quarter after we purchased the company, it became clear that unsecured bank loans had been growing at over 30% and the path to a more balanced loan portfolio would be a lot longer than we had expected. Added to that, we are seeing a few banks that are struggling to grow their deposit base which impacts how they can fund their loan growth. For many years, most depositors avoided the public sector banks fearing either insolvency or potential loss of deposits. They have been cleaned up and professionalised which is great for the Indian saver and borrower but tougher for the private sector banks who benefitted from weak competition in the public sector. With prospects for RBL looking riskier and with better ideas elsewhere, we decided to exit.

We exited Yifeng Pharmacy Chain (China: Consumer Staples) which was another name where we were becoming worried about increased regulatory oversight having a negative impact on profit margins. We are confident that they will continue to roll up the pharmacy sector in China – in much the same way that RaiaDrogasil (Brazil: Consumer Staples) is doing in Brazil – but we worry that Beijing could well impose price cuts on those drugs purchased through medical insurance plans.

We also fully sold out of Clicks (South Africa: Consumer Staples), another pharmacy chain. Growth has been phenomenal at this business with new store openings continuing apace and a better mix of basket driving profitability. However, with our focus on delivering strong absolute returns, we struggled to see Clicks growing into these valuations and decided to reallocate the capital into more attractively priced ideas elsewhere. We think Clicks remains a very high-quality business, one that we would look forward to owning again at more reasonable valuations.

Finally, we sold Integrated Diagnostics (Egypt: Health Care) due to liquidity risks and to fund higher conviction ideas elsewhere.

We did not make new complete purchases in the quarter.

We continue to discuss our China holdings at length, especially in light of the recent market moves. But another area where we are doing a lot of thinking is Poland. Here we hold Allegro (Poland: Consumer Discretionary), Dino Polska (Poland: Consumer Staples) and Jerónimo Martins (Portugal: Consumer Staples), which is listed in Portugal but >50% of revenues are from its Biedronka business in Poland.2 They all experienced strong growth through 2022 and 2023 as inflation helped them increase profit margin but the opposite has now happened. Deflation in food prices and rising costs have squeezed profit margins considerably.

As always, we spend the bulk of our time continuing to better understand the quality attributes of the companies we invest in and finding similarly resilient ideas to add to the portfolio.

1 Source: Bloomberg Finance L.P.

2 Source: Jerónimo Martins Annual Report 2023

Source for company information: Stewart Investors investment team and company data. This stock information does not constitute any offer or inducement to enter into any investment activity. Portfolio data shown is from representative strategy accounts of the strategy shown above. Named new investments disclosed relate to holdings with a portfolio weight over 0.5%. It is not a recommendation or solicitation to purchase or invest in any fund. Differences between the representative account-specific constraints, currency or fees and those of a similarly managed fund or mandate would affect results.

Voting

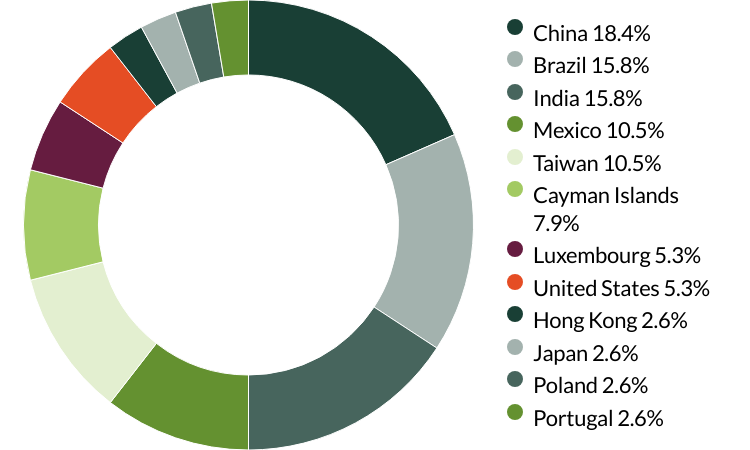

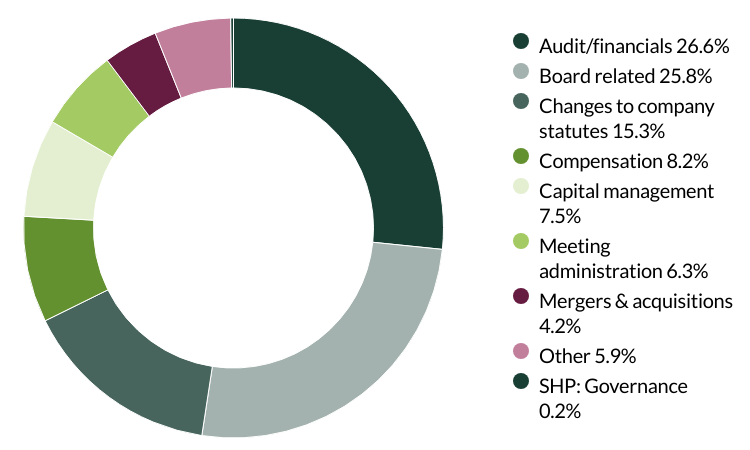

Voting: Q2 2025

Global Emerging Markets All Cap voting: 1 April - 30 June 2025

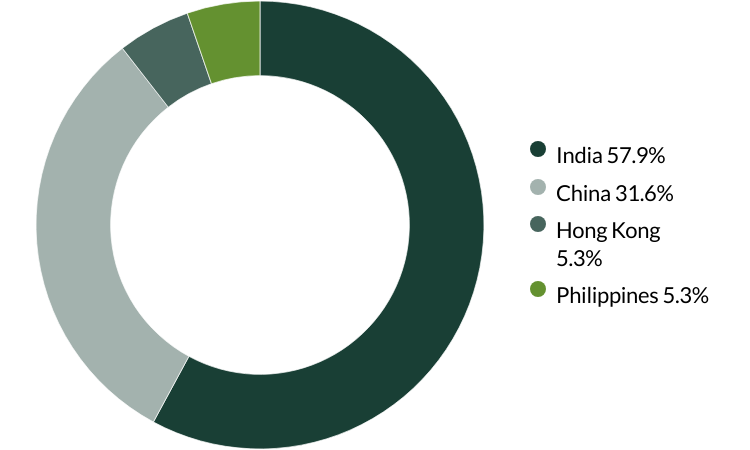

Voting by country of origin

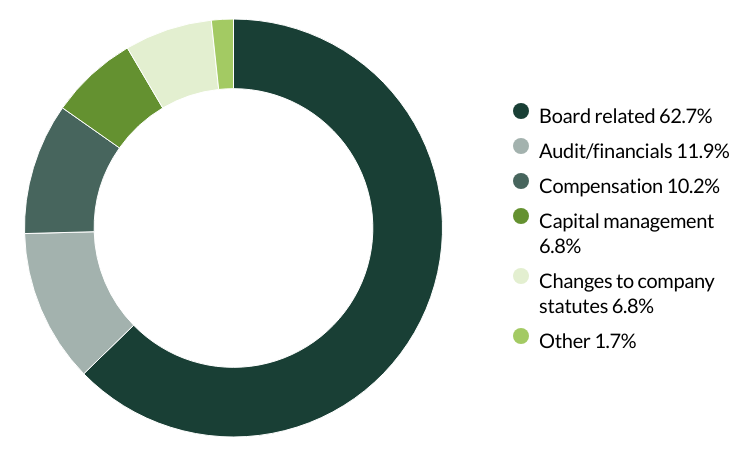

Voting by proposal category

During the quarter there were 477 proposals from 33 companies to vote on. On behalf of our clients, we voted against 11 proposals and abstained from voting on 16 proposals.

We voted against the remuneration report at Dino Polska as we believe the current policy does not encourage executives to focus on long-term goals. Implementing a long-term incentive plan could, along with enhanced disclosure and transparency on the remuneration structure, be beneficial for both the company and its shareholders. (one proposal)

We voted against changing the terms of the board at EPAM Systems as the proposed changes would require all directors to stand for election annually instead of on staggered terms. While we understand the rationale for annual elections, we believe that a staggered approach provides continuity and helps prevent excessive turnover. We also voted against changes to limit the liability of certain officers, as we believe the company has demonstrated its ability to attract and retain an admirable management team under the current structure, which encourages managers to think and act as long-term owners. Finally, we voted against the appointment of the auditor as they have been in place for over 10 years. The company has given no information on rotating its auditors, a practice we believe is important to ensure a fresh perspective is brought to its accounts. (three proposals)

We voted against a proposal at MercadoLibre to move the company’s registration from Delaware to Texas as it did not provide clear reasons for the change, and we do not believe the move aligns with shareholders’ interests. (one proposal)

We voted against the recasting of votes (the ability for voters to change their original votes on a particular matter in response to new information or changes to a proposal) for directors and the supervisory council at RaiaDrogasil. We believe the principle of recasting votes for an amended group of candidates is poor practice and would prefer the group to be resubmitted for voting. (two proposals)

We voted against the election of a director at Trip.com due to the company's lack of disclosure regarding director attendance, the number of board meetings held, and the voting results from the previous year. Our aim is to encourage greater transparency and adoption of global governance standards. (one proposal)

We voted against the recasting of votes for the supervisory council at WEG as we believe the principle of recasting votes for an amended group of candidates is poor practice and would prefer the group to be resubmitted for voting. We also abstained from voting on a request for a separate board election and the election of a supervisory council position. According to Brazilian voting practices, we are unable to vote for this proposal while simultaneouslysupporting the board in its candidate elections. (two proposals)

We voted against a request for approval to invest in wealth management products at Zhejiang Supor as we believe it carries excessive risk relative to the limited additional returns these products would provide. Making such financial investments is not central to the business and we believe surplus cash is better kept in time deposits at banks. (one proposal)

By supporting the appointment of the auditor at Jerónimo Martins, we abstained from voting on three other proposals related to auditor appointments. (three proposals)

We abstained from voting on proposals relating to the accounts and acts of the board at Regional. At the time of voting, the company had not released its annual report and/or audited financial statements, leaving us without significant information to make an informed decision. (10 proposals)

We abstained from voting on the establishment of a supervisory council at TOTVS as the company had not disclosed which candidates would be up for election to serve on the council. (two proposals)

We voted against a shareholder proposal regarding simple majority voting at EPAM Systems as this topic was already covered by the company's own proposal, which we supported. (one proposal)

Source for company information: Stewart Investors investment team and company data. This stock information does not constitute any offer or inducement to enter into any investment activity. Portfolio data shown is from representative strategy accounts of the strategy shown above. Voting chart numbers may not add to 100 due to rounding. SHP means: Shareholder Proposal.

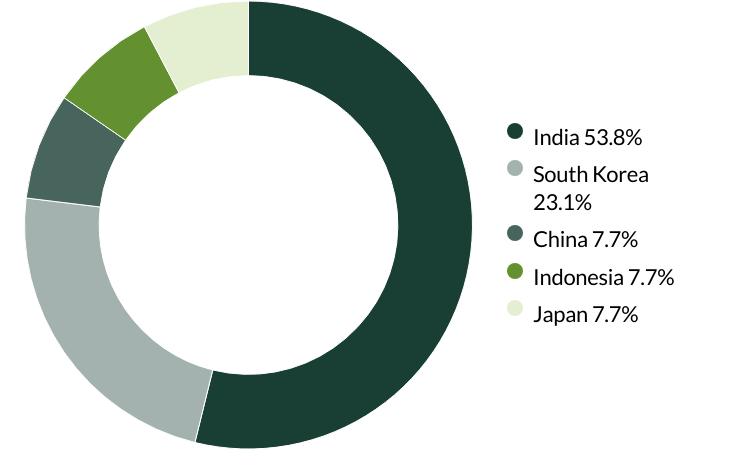

Voting: Q1 2025

Global Emerging Markets All Cap voting: 1 January - 31 March 2025

Voting by country of origin

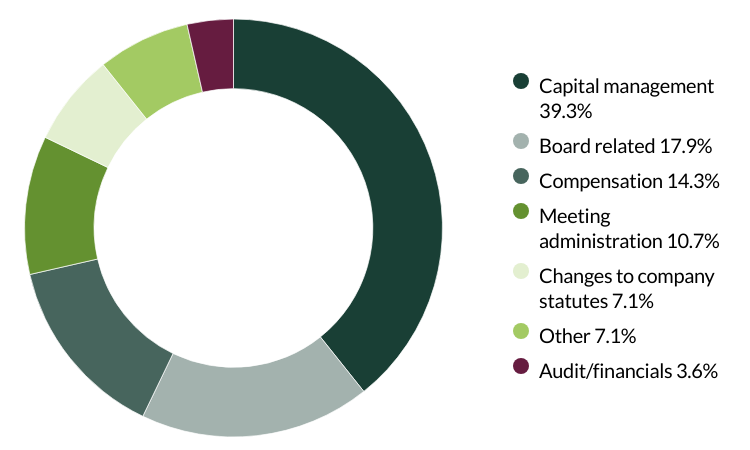

Voting by proposal category

During the quarter there were 59 resolutions from 12 companies to vote on. On behalf of clients, we voted against six resolutions.

We voted against executive remuneration at Bank Central Asia because we believed it was excessive. (one resolution)

We voted against the election of a director and their remuneration at IndiaMART as we seek to encourage greater diversity and independence on the board. (one resolution)

We voted against the election of two directors and an audit committee member at Samsung Electronics as we do not believe them to be truly independent. (three resolutions)

We voted against the election of the audit committee chair at Unicharm as we do not believe they are independent. (one resolution)

Source for company information: Stewart Investors investment team and company data. This stock information does not constitute any offer or inducement to enter into any investment activity. Portfolio data shown is from representative strategy accounts of the strategy shown above. Voting chart numbers may not add to 100 due to rounding. SHP means: Shareholder Proposal.

Voting: Q4 2024

Global Emerging Markets All Cap voting: 1 October - 31 December 2024

Voting by country of origin

Voting by proposal category

During the quarter there were 28 resolutions from eight companies to vote on. On behalf of clients, we did not vote against any resolutions.

Source for company information: Stewart Investors investment team and company data. This stock information does not constitute any offer or inducement to enter into any investment activity. Portfolio data shown is from representative strategy accounts of the strategy shown above. Voting chart numbers may not add to 100 due to rounding. SHP means: Shareholder Proposal.

Voting: Q3 2024

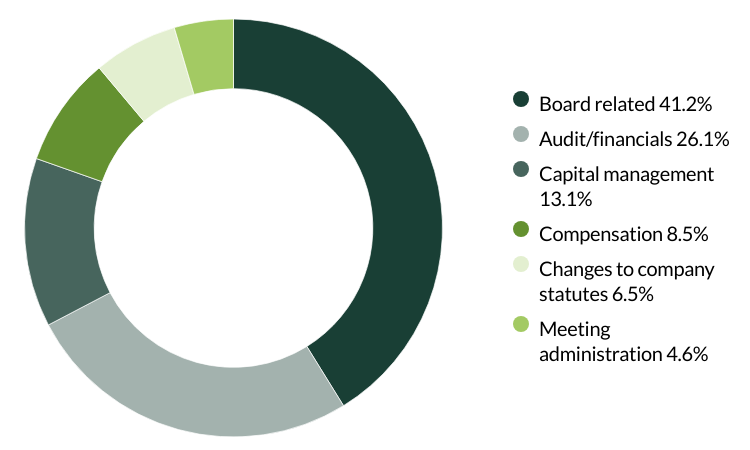

Global Emerging Markets All Cap voting: 1 July - 30 September 2024

Voting by country of origin

Voting by proposal category

During the quarter there were 153 resolutions from 17 companies to vote on. On behalf of clients, we voted against three resolutions.

We voted against the appointment of the auditor at Philippine Seven as they have been in place for over ten years. The company has given no information on intended rotation which we believe is important for ensuring a fresh perspective on the accounts. We also voted against proposals on transaction of business, as the company did not provide enough information about the proposals. We wanted to avoid giving them unrestricted decision-making power without sufficient clarity. (two resolutions)

We voted against the appointment of the auditor at Vitasoy as they have been in place for over ten years. The company has given no information on intended rotation which we believe is important for ensuring a fresh perspective on the accounts. (one resolution)

Source for company information: Stewart Investors investment team and company data. This stock information does not constitute any offer or inducement to enter into any investment activity. Portfolio data shown is from representative strategy accounts of the strategy shown above. Voting chart numbers may not add to 100 due to rounding. SHP means: Shareholder Proposal.

Portfolio Explorer

If you are unable to view the portfolio explorer, please re-open in Google Chrome, Edge, Firefox, Safari or Opera. IE11 is not supported.

For illustrative purposes only. Reference to the names of example company names mentioned in this communication is merely for explaining the investment strategy and should not be construed as investment advice or investment recommendation of those companies. Companies mentioned herein may or may not form part of the holdings of Stewart Investors. Holdings are subject to change.

Certain statements, estimates, and projections in this document may be forward-looking statements. These forward-looking statements are based upon Stewart Investors’ current assumptions and beliefs, in light of currently available information, but involve known and unknown risks and uncertainties. Actual actions or results may differ materially from those discussed. Readers are cautioned not to place undue reliance on these forward-looking statements. There is no certainty that current conditions will last, and Stewart Investors undertakes no obligation to correct, revise or update information herein, whether as a result of new information, future events or otherwise.

Source: Stewart Investors investment team and company data. Securities mentioned are all investee companies* from representative Asia Pacific All Cap Strategy, Asia Pacific & Japan All Cap Strategy, Asia Pacific Leaders Strategy, European All Cap Strategy, European (ex UK) All Cap Strategy, Global Emerging Markets (ex China) Leaders Strategy, Global Emerging Markets Leaders Strategy, Global Emerging Markets All Cap Strategy, Indian Subcontinent All Cap Strategy, Worldwide All Cap Strategy and Worldwide Leaders Strategy accounts as at 30 June 2025. *Assets that the strategies may hold which an active decision has not been made, and sustainability assessment does not apply, include cash, cash equivalents, short-term holdings for the purpose of efficient portfolio management and holdings received as a result of mandatory corporate actions. Holdings of such assets will not appear on Portfolio Explorer. Not all strategies are available in all jurisdictions or to all audience types.

The Stewart Investors supports the Sustainable Development Goals (SDGs). The full list of SDGs can be found on the United Nations website.

Source for Climate Solutions and impact figures: © 2014–2025 Project Drawdown (drawdown.org). Source for Human Development Pillars: Stewart Investors investment team.

Source for climate solutions and human development analysis and mapping: Stewart Investors investment team. Contributions are defined by the team as demonstrable contributions to any solution, either direct (directly attributable to products, services or practices provided by that company), or enabling (supported or made possible by products or technologies provided by that company).

Investment terms

View our list of investment terms to help you understand the terminology within this website.

Fund data and information

Fund prices and details

Click on the links below to access key facts, literature, performance and portfolio information for the funds and share classes available in this jurisdiction:

Stewart Investors Global Emerging Markets All Cap Fund

Share prices are calculated on a forward pricing basis which means that the price at which you buy or sell will be calculated at the next valuation point after the transaction is placed. Where a fund price is marked XD, this means that the fund is currently Ex-Dividend. Past performance is not necessarily a guide to future performance. The value of shares and income from them may go down as well as up and is not guaranteed. Please note that the yield quoted above is not the historic yield. It is considered that the yield quoted represents the current position of investments, income and expenses in the fund and that this is a more accurate figure. Investors may be subject to tax on their distribution. The yield is not guaranteed or representative of future yields. You should be aware that any currency movements could affect the value of your investment. The Funds within the First Sentier Investors Global Umbrella Fund plc (Irish VCC) are denominated in USD or EUR.

Following the UK departure from the European Union, the First Sentier Investors ICVC, an open ended investment company registered in England and Wales ("OEIC") has ceased to qualify as a UCITS scheme and is instead an Alternative Investment Fund ("AIF") for European Union purposes under the terms of the Alternative Investment Fund Managers Directive (2011/61/EU). Accordingly, no marketing activities relating to the OEIC are being carried out by Stewart Investors in the European Union (or the additional EEA states) and the OEIC is not available for distribution in those jurisdictions. We have made documents available for existing EU investors in the ICVC which can be accessed here.

Strategy and fund name changes

As of end of 2024, please note that Stewart Investors strategies and the Funds within the UK First Sentier Investors ICVC, First Sentier Investors Global Umbrella Fund plc (Irish VCC) and First Sentier Investors Global Growth Funds (Singapore Unit Trust) have been renamed. Please refer to our note via the link below for further information.