Get the right experience for you. Please select your location and investor type.

IMPORTANT NEWS: Transition of investment management responsibilities (excluding the Worldwide strategies)

First Sentier Group, the global asset management organisation, has announced a strategic transition of Stewart Investors' investment management responsibilities to its affiliate investment team, FSSA Investment Managers, effective Friday, 14 November close of business EST.

Global Emerging Markets All Cap

The strategy was launched in 2009. It invests in the shares of between 30-75 companies in emerging markets.

You can see all of the companies that this strategy invests in by filtering on our Portfolio Explorer tool.

- We define investment risk as losing clients’ money – this means we focus on looking after your money as well as growing it

- Companies must contribute to sustainable development and make a positive impact towards a more sustainable future. Portfolio Explorer >

- We invest in high-quality companies with exceptional cultures, strong franchises and resilient financials. How we pick companies >

- We avoid companies linked to harmful activities and engage and vote for positive change. Our position on harmful products >

Quarterly updates

Strategy update: Q1 2026

Global Emerging Markets All Cap strategy update: 1 January - 31 March 2026

Market review

Two developments in particular shaped the global emerging markets landscape in the first quarter. First, continued data-centre investment benefited artificial intelligence and technology supply-chain companies, even as sectors such as software and online travel platforms were hit by fears of AI disruption. Second, the US-Israeli military campaign against Iran, launched at the end of February, destabilised the Middle East and drove energy prices sharply higher.

The MSCI Emerging Markets Index fell by 0.2% over the quarter in US dollar terms. However, that headline figure concealed a tale of two halves – strong performance and inflows in the first two months, followed by a sharp reversal in March amid the rise in geopolitical risk.

Returns were concentrated. Korea and Taiwan led for much of the quarter, driven by AI-related momentum in semiconductors and technology supply chains, before partially unwinding in March. Latin America emerged as a relative safe haven, with Brazil and Colombia among the index’s top performers as oil-exporting economies benefited from the energy shock. China held up reasonably well, supported by high energy inventories. India, Indonesia and several other Asian markets were harder hit, hurt by energy dependence, currency weakness and capital outflows.

Overall, it is fair to say the market environment is uncertain. As the economist Frank Knight observed, uncertainty – unlike risk – cannot be quantified or predicted. The timing and impact of the quarter’s events would have been difficult to anticipate, which is a reminder that the task for long-term equity investors is not to forecast specific outcomes, but to build portfolios capable of staying resilient across different scenarios.

Performance review

The largest contributor to performance over the period was Samsung Electronics, a leading manufacturer of memory and semiconductor chips. The company posted record profits thanks to soaring artificial intelligence (AI)-related demand and tight supply for its high-bandwidth memory (HBM) chips. Samsung started shipping its next-generation HBM4 chip in February – having reportedly agreed higher prices compared with the previous model – positioning the company to capture a larger share of fast‑growing AI server demand. On the other hand, high legacy memory (DRAM and NAND) prices look less sustainable in the medium-term as it is already causing demand destruction in consumer electronics products.

The second largest contributor was Taiwan Semiconductor Manufacturing (TSMC), the leading foundry of advanced chips. Its recent earnings results were stronger than expected: with AI demand driving higher profits and strong guidance for the year ahead, it announced new capital expenditure plans to try and narrow the gap between its supply of advanced chips and customer demand. Over the longer term, TSMC’s unrivalled position at the most advanced process nodes, combined with its deep and longstanding customer relationships, gives it clear structural advantages. We see it as a natural beneficiary of “productisation” – the diffusion of AI into end-devices and industrial applications – which we believe will accelerate over the coming years, even if near-term data-centre spending normalises.

The third largest contributor was WEG, a Brazilian industrial group and global leader in electric motors, generators and automation solutions. Its performance was driven by strong investor enthusiasm for the company's exposure to several structural growth themes. Demand for power transformers surged as electricity grids came under pressure from data-centre construction and the broader energy transition, while interest in battery energy storage added further momentum.

On the negative side, India’s HDFC Bank was the largest detractor from performance. Its improvement in net interest margin has been slower than expected, as it continued to face a challenging operating environment. The resignation of the chairman has also led to concerns. However, we have spoken with the management and joined a call with the new interim chairman Keki Mistry, who we respect. We feel comfortable about the bank’s governance and the quality of its franchise – in particular, its deposit franchise and underwriting culture/capability remain solid and a standout amongst banks. Valuations have declined to levels not seen before, even during the Global Financial Crisis or the Covid-19 pandemic, and we find this to be very attractive, given HDFC’s leading deposit franchise and pristine balance sheet. We believe returns can improve and book value can compound at mid-teens or higher, which is attractive in absolute terms.

Trip.com was the second largest detractor. China's dominant online travel platform, with around 70% market share, the company fell sharply in January following news of an anti-monopoly investigation by Chinese regulators (the company is cooperating fully with the investigation). This was compounded by investor fears that large language models (LLMs) could disrupt its business. However, we are confident Trip.com will be resilient to AI disintermediation. The company’s proven track record in handling the real-world complexities of payments, cancellations and customer service, not to mention relationships with hundreds of thousands of hotels and other travel providers, give it key competitive advantages. Recent earnings results have been positive, and we expect Trip.com to benefit from continued travel demand in China.

The third largest detractor was Sea Ltd, the largest e-commerce, fintech and gaming platform in Southeast Asia, with growing businesses in Taiwan and Brazil. Its shares declined after it reported tighter margins due to the ongoing investment into its e-commerce business. On the other hand, revenue growth was strong, and its credit business expanded at a brisk clip. With a model focused on low costs and being competitive on prices, Sea can serve a layer of customers that no one else can touch, and profitably too. We believe the management and the culture are worth backing, and execution continues to be strong across all three businesses.

New purchases over the quarter

Full Truck Alliance (FTA) is a leading digital freight platform in China with a strong competitive moat and a long growth runway. FTA should continue to strengthen with scale, as shippers move more of their business on to the platform, driven by cheaper prices, which then drives more truckers to the platform, and so on. The business is still in the early stages of monetisation (which implies room to grow), margins are expanding, and it is cash flow generative. Meanwhile, new growth opportunities, such as cargo pooling, could also open up once it reaches a minimum viable scale.

PDD is a leading e-commerce company in China. Founded by Colin Huang – widely respected and recognised as a capable leader – the company is an innovator within China’s e-commerce industry, having disrupted the seemingly mature market by bringing customers directly to farmers and manufacturers. Positioned as a “value-for-money” platform, it is a highly profitable and cash flow generative business, while being less capital intensive vs. peers. We believe it has good growth potential, with a franchise that continues to strengthen.

Kotak Mahindra Bank is one of India’s leading financial services companies – it has consistently improved the strength of its deposit franchise and maintained better asset quality than peers through the business cycle. The new CEO, Ashok Vaswani, has aspirations to grow the business, with greater focus on consumer banking and digitisation. We expect to see a growing trend of formalised financial savings, benefiting Kotak’s insurance, mutual funds and asset management businesses

Complete sales over the quarter

We sold out of several positions where we had lower conviction, in order to consolidate the portfolio among a smaller number of companies with better long-term prospects. These divestments included:

Tube Investments, a diversified Indian industrial conglomerate with businesses spanning precision steel tubes, automotive components, bicycles and financial services.

Advantech, a Taiwan-based technology company specialising in industrial computing, embedded systems and solutions for automation and smart manufacturing applications.

Ayala Corp, one of the Philippines' oldest and largest conglomerates, with interests spanning real estate, banking, telecoms, water, healthcare and renewable energy.

Looking forward

The situation in the Middle East is clearly clouding the near-term outlook. Around 20% of global seaborne oil and liquefied natural gas (LNG) flows through the Strait of Hormuz, so any disruption has immediate implications for energy prices, freight costs and inflation.

Our base case is that there are political constraints – particularly for the US – that should limit the duration of the conflict and lead to some degree of de-escalation in coming weeks. That said, history shows these situations can evolve in unintended ways. If the conflict persists or escalates, the implications would extend well beyond the region and into the global economy.

In terms of portfolio impact, the first-order effects are largely regional, where we have no exposure. The second-order effects are more relevant: energy flows through the Strait and the resulting price impact. Asia is particularly exposed given its reliance on imported energy from the Middle East. South Asia – especially India – is more vulnerable, as energy is both a large import item and a meaningful component of CPI, which is likely to weigh on consumption. North Asia will also be affected, though the impact should be more muted given higher income levels and greater resilience.

Against this backdrop, we remain confident in the strategy’s ability to navigate the environment. The companies we own benefit from strong competitive positions – whether through network effects, brands, distribution, cost leadership or high switching costs for essential products and services. Historically, this has translated into pricing power and the ability to protect margins even in more inflationary or volatile conditions.

Latest insights from the FSSA team

We have written short articles on companies, investment trends and market themes across our various strategies, which are available to read on the FSSA website.

Our latest piece “Against the current” discusses the reasons why high-quality companies are being overlooked amid the artificial intelligence boom and resurgence in cyclical stocks. FOMO is beating fundamentals; but these trends are creating opportunities for quality-focused investors in Asia and emerging markets to accumulate attractive businesses at lower valuations.

Source for company information: First Sentier Group and company data. This stock information does not constitute any offer or inducement to enter into any investment activity. Portfolio data shown is from representative strategy accounts of the strategy shown above. Named new investments disclosed relate to holdings with a portfolio weight over 0.5%. It is not a recommendation or solicitation to purchase or invest in any fund. Differences between the representative account-specific constraints, currency or fees and those of a similarly managed fund or mandate would affect results.

Strategy update: Q4 2025

Global Emerging Markets All Cap strategy update: 1 October - 31 December 2025

In November 2025, First Sentier Group (FSG) announced a strategic transition of Stewart Investors’ (SI) investment management responsibilities to its affiliate investment team, FSSA Investment Managers (FSSA). This was decided to be in the best interests of our clients, given the significant overlap in SI’s and FSSA’s investment capabilities and our shared history and heritage.

Introducing FSSA Investment Managers

FSSA has been investing in Asia Pacific and Global Emerging Market equities since 1988 as part of the former Stewart Ivory & Company, which subsequently became First State Stewart. After years of organic growth, the First State Stewart team split in two in 2015, leading to the formation of FSSA Investment Managers and Stewart Investors.

Like SI, we are long-term and quality-focused investors. We pay little attention to the index or short-term performance, preferring to focus on generating absolute returns for our clients in the long run. From our research, we aim to construct relatively concentrated portfolios made up of the best ideas that we can find across Asia and emerging markets. As responsible, long-term shareholders, we have integrated sustainability analysis into our investment process and engage extensively with companies on environmental, labour and governance issues.

Following the transition of SI’s portfolios to FSSA, the Stewart Investors Global Emerging Markets All Cap portfolio is now being managed by Rasmus Nemmoe and Rizi Mohanty.

Rasmus Nemmoe is a Portfolio Manager at FSSA Investment Managers. He joined the team in 2016 and is the lead manager of the FSSA Global Emerging Markets Focus strategies. Rasmus has more than 20 years of investment experience and is based in Hong Kong.

Rizi Mohanty is a Portfolio Manager at FSSA Investment Managers. He joined the team in 2016 and focuses on the Southeast Asian markets as well as Asia ex-Japan equities more broadly. He is the lead manager of the FSSA ASEAN All Cap and FSSA Asian Growth strategies. Rizi has more than 14 years of investment experience and is also based in Hong Kong.

Rasmus and Rizi are supported by a broader team of investment analysts, with an average of 14 years of investment experience and 8 years tenure with the team. All 15 members of the FSSA investment team are analysts first and foremost, including the portfolio managers, and we spend the majority of our time meeting companies, writing research and seeking quality companies to invest in.

How we invest

FSSA’s investment philosophy, which shares its genesis with SI, has remained broadly unchanged since the First State Stewart team was established in 1988. We focus on identifying quality companies, buying them at a sensible price and holding them for the long term. Most importantly, we invest our clients’ capital as if it were our own. As long-term investors and owners of businesses on behalf of our clients, we look for founders and management teams that act with integrity and risk awareness, and dominant franchises that have the ability to deliver sustainable and predictable returns over the long term.

As a team, we conduct over 1,000 direct company meetings each year across Asia and other emerging markets. The most significant source of investment ideas comes from these company visits and country research trips. We find that our reputation as patient, long-term investors has given us unparalleled access to management, which allows us to gain valuable insights and a thorough understanding of the businesses we want to invest in.

As a result of our long-term time horizon and conservative investment approach, our portfolios – and our performance – can look very different to the index. We shy away from “flavour of the month” themes (such as the current AI-driven boom), and instead look for high-quality companies that can deliver attractive returns for much longer than the market expects – and extend our investment time horizon to capture that advantage. When you own quality businesses, time isn’t a risk – it’s an asset.

Our performance may lag in very buoyant or momentum-driven markets, but we usually compensate very quickly once such bubbles burst. Based on historical data, our long-term track record shows that our portfolios tend to perform better in “normal” markets (-15% to +15% returns over one year) and bear markets (more than 15% decline), than in steeply rising markets (defined as over 15% returns over one year).

A smooth transition

Given the significant overlap in SI’s and FSSA’s investment philosophy and portfolios, we know all the holdings well. As part of the transition, we made a few changes to tilt the portfolio towards companies with stronger cash generation, higher returns and better long-term growth prospects. In general, we are adding to holdings in China, where we have found leading businesses like Tencent, with strong competitive advantages and attractive growth at reasonable valuations. We are reducing exposure to India, mainly in cyclical businesses like Tube Investments of India and Motilal Oswal, where valuations are expensive and the growth outlook has deteriorated.

Below, we highlight a few of the key additions and disposals over the fourth quarter of 2025.

New purchases:

Tencent Holdings is the largest social media network and online gaming company in China, with growing businesses in online advertising, cloud services, e-payments/e-commerce and overseas gaming. Tencent has created an ecosystem of businesses which are unrivalled and should continue growing over the medium term. It has continued to develop new functions within WeChat (such as Video Accounts and Mini Shops), which should slowly improve monetisation and enhance the quality of the franchise. At FSSA, we have been shareholders of Tencent since 2005 and have consistently found the management to be effective long-term stewards of the business. In recent times, we have been impressed by Tencent’s AI strategy and its disciplined approach to technology investments, which aligns with our conservative view on AI capex spending.

Sea is the largest e-commerce, fintech and gaming platform in Southeast Asia, with growing businesses in Taiwan and Brazil. The e-commerce business (75% of sales) is complex, but its model is focused on the lowest cost structure and being competitive on prices, which allows Sea to serve a layer of customers that no one else can touch, and profitably too. The margins are admittedly thin for now, but it seems like the hard work is done. From here, it should be easier to grow the business and unlock operating leverage. The management and the culture are worth backing, and execution has been consistently strong across all three businesses.

Nu Holdings is a digital-only bank in Brazil with over 100 million customers. Founded in 2013, it has disrupted large incumbent banks thanks to its superior customer service and lower costs. There is strong alignment with the leadership team and a prudent lending culture. The company has achieved decent profitability while the growth outlook is robust, driven by increasing credit penetration and additional service offerings (such as secured loans and digital payments).

Complete sales:

Milkyway Intelligent Supply Chain is a chemical materials logistics company in China. We sold out of the position on concerns about leverage and poor cash generation.

Motilal Oswal Financial Services is a non-bank financial company (NBFC) in India. We sold out of a lower conviction holding to raise cash for better ideas elsewhere.

Voltronic Power is a Taiwanese company specialising in uninterruptable power supply (UPS). We sold out of a lower conviction holding to raise cash for better ideas elsewhere.

Performance and outlook

With our long-term investment time horizon, we tend not to pay much attention to short-term market fluctuations. We invest on at least a three-to-five-year view, though we often hold on to companies for much longer. In an industry rife with short-termism, we believe our long-term approach stands out from the crowd.

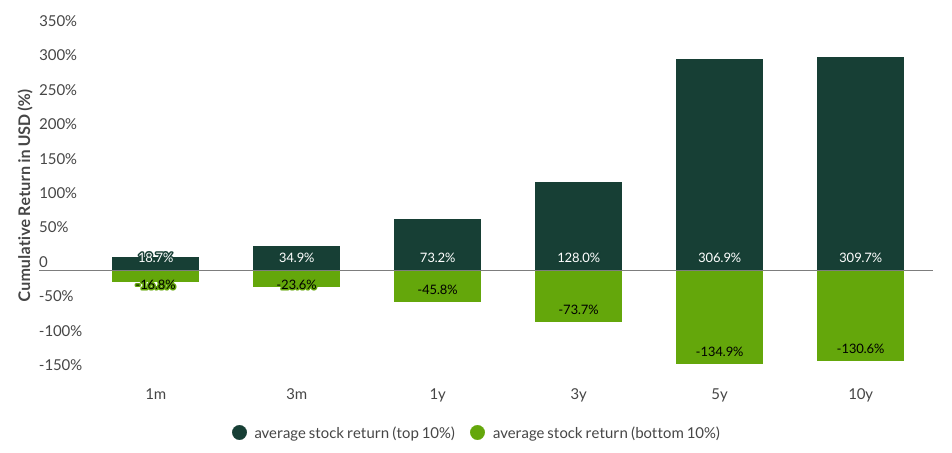

What we have seen, over the past few decades, is that average holding periods for stocks have fallen from over eight years in the 1960s to less than six months today. Yet this shift has come at a cost: it reduces investors’ ability to generate outsized returns that are materially different from the broader market. The reason is simple — as investment horizons shrink, so does the return dispersion between the best- and worst-performing companies. With less time in the market, investors end up tracking the index, not beating it.

Emerging Markets: time horizons matter

MSCI EM Index -dispersion around mean return for top 10% top / bottom stock performers

Source: MSCI Emerging Markets Index, as at 31 May 2025

In a world where markets rise consistently, that might seem like an acceptable outcome. But markets don’t move in straight lines; and in addition to the higher costs and transaction fees that come with frantic trading activity, the bigger issue is that investors miss out on what is far more important – the future value creation that the best companies tend to generate. This is often poorly understood by the market, with many investors simply focusing on the next quarter or year ahead. Yet the real drivers of returns lie in the cash flows that come well beyond that timeframe.

With that context in mind, we highlight the key contributors and detractors from performance over the fourth quarter of 2025.

The largest contributor to performance over the period was Samsung Electronics, a leading manufacturer of memory and semiconductor chips. In recent years, Samsung’s foundry business has been a major point of investor concern, which culminated in significant losses in the first half of 2025. These losses were exacerbated by one-time charges related to US export controls to China. The company has since undertaken a strategic shift from a “capacity-first” to a “customer-first” model, which appears to be bearing fruit. The shares rose during the quarter, as Samsung continued to benefit from surging AI-related demand for its high-bandwidth memory chips as well as tightness in traditional DRAM demand-supply. Strong results from US chipmaker Micron reinforced expectations of a sustained memory upcycle into 2026. With the turnaround in its foundry business and a strong legacy memory business, we believe the risk-reward looks favourable.

Taiwan Semiconductor Manufacturing (TSMC) was the second largest contributor to performance, as it continued to see solid revenue growth and strong demand from cloud AI for its leading-edge chips. Given the lead time and supply shortages, this provides visibility into 2026 earnings and possibly even beyond into 2027. TSMC is expected to invest in capacity expansion, with top line growth to follow.

The third largest contributor to performance was WEG, a Brazilian multinational electrical-equipment company. A leader in transformers and industrial electric motors, WEG continued to deliver solid profits in 2025, despite facing challenges due to US tariffs on imports from Brazil. Over the longer term, AI-driven power demand and the ongoing electrification of grids in Brazil and other key markets where WEG has a presence – including Mexico and South Africa – is expected to drive stronger revenue growth in the company’s core transformer business.

On the negative side, Tube Investments of India was the biggest detractor from performance, as it reported sluggish business performance and rising competition in the electric vehicle (EV) space. Despite its early mover advantage, Tube has struggled to maintain market share. It plans to arrest these challenges by increasing the number of dealership partners and entering new sub-segments in EV battery packs. On a positive note, the core business is stable with robust returns on capital employed, and it generates healthy free cash flow which is being invested in new businesses with high returns potential. In this endeavour, we are backing the management, particularly Vellayan Subbiah (executive chairman), who has an exceptional track record and has created tremendous value for shareholders.

Alibaba was the second biggest detractor. The shares weakened over the last few months of 2025 on concerns about its e-commerce business and the resulting pressure on earnings. Losses from its Taobao Instant Commerce business (food delivery and on-demand retail) weighed on the share price. On the other hand, Alibaba has had a strong run-up over 2025, driven by its investments into AI and growing demand for cloud computing. Alicloud revenue has accelerated in recent quarters and is expected to continue at pace in the coming quarters.

Milkyway Intelligent Supply Chain, a leading Chinese chemical materials logistics firm, was the third biggest detractor, declining due to underwhelming earnings results. The company’s revenue and profit growth lagged analyst expectations due to weak demand across China’s chemicals sector. While the company is taking steps to improve the efficiency of its operations, we nevertheless decided to sell our stake in order to raise cash for better opportunities.

Looking forward

Despite the geopolitical uncertainty triggered by the US administration’s reciprocal tariff policy, emerging-market equities delivered robust performance in 2025. This reflects longer-term developments. The global economy is increasingly being led by emerging markets, a trend we expect to accelerate in the future. As concerns grow over the health of the US economy, investors are considering alternatives, as indicated by the strong demand for emerging-market equities over the last year.

Amid the market rise, it is important to keep a close eye on valuations. The growth in AI-related spending has led to a particularly sharp increase in the shares of chipmakers and other technology firms. While some of the Fund’s key holdings are benefiting from this trend, it is important not to get carried away by the hype around generative AI. In the tech sector as elsewhere, the Fund focuses on businesses with proven management teams and competitive advantages that allow them to capitalise on long-term shifts across emerging markets.

Whether it is the development of Chinese cities as hubs for innovation in medical devices, the formalisation of the Indian economy, the continued financialisation of the South African population, or the growing enterprise resource planning (ERP) adoption by small-to-medium sized enterprises in Brazil, there are plenty of investment opportunities in emerging markets. Yet these kinds of businesses are not widely included in major market benchmarks, which is why the Fund focuses on high-quality companies rather than following the crowd.

SFDR Article 9 and FSSA’s approach to sustainability

All SI portfolios will continue to be managed true to label, with due consideration given to SI’s SFDR Article 9 sustainability requirements. Importantly, both FSSA and SI had operated as one team for 27 years (1988-2015) before the decision was made in 2015 to split into two teams. This is heavily reflected in our investment philosophies and processes and our respective approaches to sustainability.

At FSSA, we believe it is everyone’s responsibility to think about sustainability as part of his or her investment decision-making. We don’t use external consultants or environmental, social and governance (ESG) ratings, nor do we outsource the sustainability work to a separate team. In our research, we focus on evaluating the long-term merits of a given investment opportunity. Given that sustainability issues are effectively investment issues, we believe that these challenges and opportunities – and management’s response to them – can have a significant impact on a company’s returns. As such, we look for evidence that the management operates the business effectively and in the interests of all stakeholders – both now and for the longer term.

While issues relating to climate change, or people and communities, are often the ones that get the most attention, most of our company engagements relate to management quality and corporate governance systems, as we believe that good governance is the foundation on which great companies are built. We often engage with management teams on capital allocation and strategy, remuneration structures and succession planning, board diversity and tenure, and ensuring high levels of transparency and company disclosure – to highlight just a few.

For more information on FSSA, or if you have any questions about the transition, please do not hesitate to contact us.

NB Both Stewart Investors and FSSA have been supported by the same centralised Responsible Investment team within the First Sentier Group, who will continue to support FSSA after the transition of SI funds.

Source for company information: First Sentier Group and company data. This stock information does not constitute any offer or inducement to enter into any investment activity. Portfolio data shown is from representative strategy accounts of the strategy shown above. Named new investments disclosed relate to holdings with a portfolio weight over 0.5%. It is not a recommendation or solicitation to purchase or invest in any fund. Differences between the representative account-specific constraints, currency or fees and those of a similarly managed fund or mandate would affect results.

Strategy update: Q3 2025

Global Emerging Markets All Cap strategy update: 1 July - 30 September 2025

Emerging markets enjoyed another strong quarter due, in part, to sharp gains for those Chinese stocks that are seen as beneficiaries of the artificial intelligence (AI) boom. Although some of our Chinese holdings, such as Alibaba, performed well, not all of our holdings there are aligned with the surge of investment in AI. As a consequence, returns from our strategy lagged behind emerging-market indices. While these types of market conditions can be challenging for our approach, we know that our philosophy and process have been proven to deliver over the long term.

The long-term outlook for Indian companies remains bright

The quarter saw a continuation of an unhelpful dynamic: the significant outperformance of the Chinese market relative to India. We have more invested in India, where we are enthusiastic about the long-term prospects for a range of high-quality companies, than we do in China. So far, this year has seen a reduction in income taxes and a simplification of the Goods and Service Tax (‘GST’) system in India, which is similar to the value added tax (VAT) levied in the UK. India’s central bank, meanwhile, has been cutting interest rates. Both should boost demand.

There is, of course, more to emerging markets than China and India. Having visited South Korea in September, we are increasingly confident in the changes to corporate governance standards that are unfolding in that country. These echo similar reforms seen in Japan and could have positive effects on shareholder returns in Korea and perhaps across the region more widely – a similar mood of reform now seems to be infecting other countries across Asia.

Continuity and change

It would be remiss not to mention the significant changes that have taken place at Stewart Investors over the last quarter. After acting as careful stewards of our clients’ capital over many years, three of our colleagues stepped back from their portfolio-management responsibilities in August and left the business. While our team looks different now than it did when the quarter began, on a deeper level, nothing has changed: the philosophy and approach that has defined Stewart Investors since 1988 is deeply engrained and continues to define what we do. Our structure is flat. Every member of the investment team is first and foremost an analyst and our collective focus is on identifying high-quality companies, with resilient financials, guided by ambitious stewards.

This strategy’s new lead manager is Jack Nelson, who was formerly its co-manager. He joined Stewart Investors in 2011 and is the lead manager of our Global Emerging Markets Leaders strategy. He continues to apply the same principles to managing this strategy that have guided it since its launch, working as part of the same tight-knit group of investment analysts and drawing on the same common pool of investment ideas.

Activity

We added one new holding to the portfolio during the quarter. Ayala (Philippines: Industrials) is owned by the seventh generation of Zóbel de Ayala family and its interests span property, banking, car dealerships, renewable energy, and retail. Like us, the Zóbel de Ayala family focus on finding long-term growth opportunities. The Philippines appears to be rich in those opportunities. For example, while around half of Filipinos don’t have a bank account, lenders such as Bank of the Philippine Islands (BPI, in which Ayala is a major shareholder) are opening new branches, acquiring new customers, and promoting financial inclusion.1

We sold several holdings where we had lost some confidence in our investment thesis. Vitasoy (Hong Kong: Consumer Staples) has struggled with supply-chain issues. This year, however, its shares have rallied in response to rumours of a takeover bid. This provided a good opportunity for us to sell the holding and reinvest the proceeds in companies where we have great of confidence.

We also sold home appliance manufacturer Zhejiang Supor (China: Consumer Discretionary). A subsidy programme introduced by the government earlier this year offers Chinese consumers financial incentives to trade in and upgrade their home appliances. This has helped to foster positive sentiment towards Zhejiang Supor. Looking longer term, however, the outlook for its future growth appears to be muted, so this appears to be a good opportunity to sell.

Elsewhere, we sold out of Hoya (Japan: Health Care) which, despite being listed in Japan, sells the majority of its products into emerging markets. We also sold Tata Communications (India: Communication Services) and Jerónimo Martins (Portugal: Consumer Staples). In all three cases, these companies’ shares appeared somewhat expensive given the growth on offer. We believe new ideas such as Ayala – as well as our other existing holdings – now represent better homes for our clients’ capital.

1 Source: World Bank Global Findex database https://databank.worldbank.org/source/global-findex-database. 2024 data for metric: account (% age 15+) which measures the percentage of respondents having an account at a bank or similar financial institution or using a mobile money service.

Source for company information: First Sentier Group and company data. This stock information does not constitute any offer or inducement to enter into any investment activity. Portfolio data shown is from representative strategy accounts of the strategy shown above. Named new investments disclosed relate to holdings with a portfolio weight over 0.5%. It is not a recommendation or solicitation to purchase or invest in any fund. Differences between the representative account-specific constraints, currency or fees and those of a similarly managed fund or mandate would affect results.

Strategy update: Q2 2025

Global Emerging Markets All Cap strategy update: 1 April - 30 June 2025

The announcement of President Trump’s ‘Liberation Day’ tariffs on 2 April and the short, sharp trade war with China that followed drove share prices sharply lower.

Nerves were soon calmed, however, by the announcement of a 90-day pause on the tariffs’ introduction. That calm endured even when Israel took direct military action against Iran, with the oil price spiking higher only briefly. Perhaps the most interesting development from our perspective, however, was that the US dollar had its weakest start to the year since 19731. We think the pressure on the dollar could persist and may, in time, encourage asset owners to reduce the proportion of their wealth held in US and look to emerging markets instead.

We added two new holdings over the quarter: one in China, one in India. Trip.com (China: Consumer Discretionary) is the country’s largest online travel-booking platform. It survived the dead stop in tourism prompted by the covid pandemic and now seems primed to take advantage of a shift to booking travel online. Although only about 10% of the Chinese population currently has a passport, that proportion is expected to increase2. The second addition this quarter was Motilal Oswal Financial Services (India: Financials), a financial-services group active in stockbroking, asset management, wealth management, investment banking, and housing finance with an ambitious-but-conservative steward at its helm. It should benefit from meeting the needs of India’s growing middle class. We also continued to build our positions in Cholamandalam Financial Holdings (India: Financials), Alibaba (China: Consumer Discretionary) and Naver (South Korea: Communication Services).

Set against that, we sold EPAM Systems (United States: Information Technology). We have become increasingly concerned about the outlook for IT services businesses, seeing a risk that their clients postpone or cancel investments in IT systems due to the uncertainties currently facing the US economy. As part of our ongoing review of this sector, we also trimmed the holding in Globant (Argentina: Information Technology). We understand the argument that some companies will need IT services businesses to help them to adopt and integrate artificial intelligence (AI) tools. Equally, it may be that its clients actually replace their existing IT services with AI. Elsewhere, we sold Syngene (India: Health Care) and Dr. Lal PathLabs (India: Health Care) to finance additions elsewhere.

Looking ahead, we remain particularly positive on the prospects for high-quality companies in India. The central bank recently started cutting interest rates, which should support demand in rural India. Towards the end of the quarter, we attended a conference of Indian companies and were struck by how positive all of them were about the growth opportunities ahead of them over the next 10 years. In our view, this potential growth – and the size of the Indian market – should continue to offer powerful support to share prices.

[1] Source: Financial Times, 30 June 2025 ‘US dollar suffers worst start to year since 1973’.

[2] Source: Straits Times, 21 December 2023 ‘China is world’s second-largest economy but its passport is ranked 63rd. Are things looking up?’.

Source for company information: First Sentier Group and company data. This stock information does not constitute any offer or inducement to enter into any investment activity. Portfolio data shown is from representative strategy accounts of the strategy shown above. Named new investments disclosed relate to holdings with a portfolio weight over 0.5%. It is not a recommendation or solicitation to purchase or invest in any fund. Differences between the representative account-specific constraints, currency or fees and those of a similarly managed fund or mandate would affect results.

Portfolio Explorer

Portfolio Explorer tells the stories of the companies we invest in. The company profiles have been written by our own team so that you can see why they believe that the companies they invest in are making the world a better place.

Fund data and information

Key documents and links

- Factsheet and KIIDS

- Prospectuses

- Application forms

- Download Annual Review 2024 - ICVC

- Download Annual Review 2024 - VCC

- Strategy Climate Report 2021

- The race to zero: Climate Report 2021

- UK Task Force on Climate-related Financial Disclosures (“TCFD”) Public Product report

- SDR Client Facing Disclosure

Fund prices and details

Click on the links below to access key facts, literature, performance and portfolio information for the funds and share classes available in this jurisdiction:

Stewart Investors Global Emerging Markets All Cap (UK OEIC)

| Fund name | Fund type | Currency | Price | Daily change | Price date | Factsheet |

|---|---|---|---|---|---|---|

| Stewart Investors Global Emerging Markets All Cap Class A (Acc) | OEIC | GBP | 405.68 | 0.19 | 24 Jun 2026 | |

| Stewart Investors Global Emerging Markets All Cap Class B (Acc) | OEIC | GBP | 458.49 | 0.19 | 24 Jun 2026 | |

| Stewart Investors Global Emerging Markets All Cap Class A (Acc) | OEIC | EUR | 453.28 | 0.24 | 24 Jun 2026 |

Stewart Investors Global Emerging Markets All Cap (Irish VCC/Offshore)

| Fund name | Fund type | Currency | Price | Daily change | Price date | Factsheet |

|---|---|---|---|---|---|---|

| Stewart Investors Global Emerging Markets All Cap Class I (Acc) | Irish UCITs | EUR | 9.80 | 0.28 | 24 Jun 2026 | |

| Stewart Investors Global Emerging Markets All Cap Class I (Acc) | Irish UCITs | USD | 11.77 | -0.30 | 24 Jun 2026 | |

| Stewart Investors Global Emerging Markets All Cap Class VI (Acc) | Irish UCITs | EUR | 2.56 | 0.28 | 24 Jun 2026 | |

| Stewart Investors Global Emerging Markets All Cap Class VI (H Dist) | Irish UCITs | EUR | 12.05 | 0.28 | 24 Jun 2026 | |

| Stewart Investors Global Emerging Markets All Cap Class VI (Acc) | Irish UCITs | GBP | 10.25 | 0.12 | 24 Jun 2026 | |

| Stewart Investors Global Emerging Markets All Cap Class VI (Acc) | Irish UCITs | USD | 13.23 | -0.30 | 24 Jun 2026 |

Share prices are calculated on a forward pricing basis which means that the price at which you buy or sell will be calculated at the next valuation point after the transaction is placed. Where a fund price is marked XD, this means that the fund is currently Ex-Dividend. Past performance is not necessarily a guide to future performance. The value of shares and income from them may go down as well as up and is not guaranteed. Please note that the yield quoted above is not the historic yield. It is considered that the yield quoted represents the current position of investments, income and expenses in the fund and that this is a more accurate figure. Investors may be subject to tax on their distribution. The yield is not guaranteed or representative of future yields. You should be aware that any currency movements could affect the value of your investment. The Funds within the First Sentier Investors Global Umbrella Fund plc (Irish VCC) are denominated in USD or EUR.

Strategy and fund name changes

As of end of 2024, please note that Stewart Investors strategies and the Funds within the UK First Sentier Investors ICVC, First Sentier Investors Global Umbrella Fund plc (Irish VCC) and First Sentier Investors Global Growth Funds (Singapore Unit Trust) have been renamed. Please refer to our note via the link below for further information.

An affiliate of First Sentier Group

Copyright © 2026 Stewart Investors.