Get the right experience for you. Please select your location and investor type.

Indian Subcontinent All Cap

Launched in 2006, the strategy invests in companies based in or having significant operations in India, Pakistan, Sri Lanka or Bangladesh.

Strategy overviewLaunched in 2006, the Stewart Investors Indian All Cap Strategy is a long-term, equity-only strategy that aims to invest in shares of high-quality companies positioned to contribute to, and benefit from, the sustainable development of the region. Given the size of the economy and the investment universe, the majority of the strategy’s 30-60 investments are in Indian-listed companies.

Strategy highlights: a focus on quality and sustainability

- Companies must contribute to sustainable development. Portfolio Explorer >

- We invest in high-quality companies with exceptional cultures, strong franchises and resilient financials. How we pick companies >

- We avoid companies linked to harmful activities and engage and vote for positive change. Our position on harmful products >

- Our approach is long-term, bottom-up, high conviction and benchmark agnostic

- We focus on capital preservation as well as capital growth – we define risk as the permanent loss of client capital

Latest insights

Quarterly updates

Strategy update: Q2 2025

Indian Subcontinent All Cap strategy update: 1 April - 30 June 2025

It was another quarter in which our clients were keen to discuss both the short - and long-term prospects for investing in India. The questions we were asked covered a range of topics, including:

- Whether India’s growth is sustainable given global headwinds.

- The risks arising from the country’s dependency on imported energy.

- Whether valuations remain too high.

- The extent to which India’s economic development is inclusive.

All of these subjects are worthy of debate. As always, however, we prefer to think about the investment opportunities from the bottom-up – by looking for and talking to high-quality companies that are both driving and benefiting from long-term human development trends. We believe there are plenty of these businesses in India and we tend to share the excitement expressed by the chief executive of one of our holdings, Mahindra & Mahindra (India: Consumer Discretionary):

Sentiments like these are not uncommon among India’s high-quality companies. They remind us there is still lots of work to be done to build capacity and meet demand. We believe this dynamic should underpin the long-term growth of those companies that can contribute to India’s development in a sustainable way.

We initiated seven new positions over the quarter. Dalmia Bharat (India: Materials) is a well-managed, family-owned supplier of cement and related products. PB Fintech (India: Financials) is the holding company of Policybazaar (an insurance intermediary) and Paisabazaar (a loans intermediary). It is growing nicely and has strong market shares in both areas. Jyothy Labs (India: Consumer Staples) is a family-owned supplier of cleaning and personal care products with a strengthening and diversifying franchise. It has no debt on its balance sheet. Motilal Oswal Financial Services (India: Financials) is a diversified financial conglomerate operating in retail and institutional broking, asset management, wealth management, investment banking, and housing finance with an ambitious-but-conservative steward at its helm. It should benefit from meeting the savings and investment needs of India’s growing middle class. CarTrade Tech (India: Consumer Discretionary) is a platform that helps to match buyers and sellers of new and second-hand cars. Its acquisition of classified-ad portal OLX India has given it the opportunity to expand and diversify away from cars.

Blue Star (India: Industrials) makes, installs and services air conditioners, refrigerators, deep freezers, watercoolers, and cold rooms. Its products are found in a third of India’s commercial buildings2. With family owners and an ambitious, competent, and long-tenured management team, it is well stewarded. The final addition, MakeMyTrip (India: Consumer Discretionary), is India’s leading online travel agency. Its platforms – MakeMyTrip, Goibibo and redBus – facilitate travel and tourism, supporting job creation and economic growth.

To fund these purchases, we sold Syngene (India: Health Care), Cyient (India: Information Technology), Dr. Lal PathLabs (India: Health Care), Bajaj Housing Finance (India: Financials), Tata Chemicals (India: Materials) and Tata Consumer Products (India: Consumer Staples). These sales were prompted either by valuations becoming too stretched or because we felt the opportunity cost of holding these positions was too high given the strength of our conviction in other stocks.

Focusing on what individual companies are saying and doing is especially important as macro news – on the global economy, trade and geopolitics – continues to build. Rather than trying to second-guess politicians, we prefer to spend our time focusing on companies with high-quality management, robust franchises and strong financials with compelling valuations. Although we understand that these companies do not exist in a vacuum, we try to focus on what we can control rather than fretting over those things we can’t. As such, we are striving to analyse the long-term opportunities and idiosyncratic risks facing the companies we invest in.

[1] Mahindra & Mahindra Annual Report 2024 https://www.mahindra.com/annual-report-FY2024/index.html pp. 7/519.

[2] Source: Blue Star Annual Report 2023-24.

Source for company information: Stewart Investors investment team and company data. This stock information does not constitute any offer or inducement to enter into any investment activity. Portfolio data shown is from representative strategy accounts of the strategy shown above. Named new investments disclosed relate to holdings with a portfolio weight over 0.5%. It is not a recommendation or solicitation to purchase or invest in any fund. Differences between the representative account-specific constraints, currency or fees and those of a similarly managed fund or mandate would affect results.

Download a PDF copy

Select Strategy update and/or Proxy voting to produce a report. You can then download a copy of the report by clicking on the button.

You can build a bespoke report for all our strategies on the full Quarterly update report.

Strategy update: Q1 2025

Indian Subcontinent All Cap strategy update: 1 January - 31 March 2025

Due to the recent softness in the Indian market, we have received lots of questions from investors and plenty of interest in the strategy. Recent market declines have given us an opportunity to add to some of our existing high-quality holdings at more attractive valuations as well as to add a number of new names.

Over the quarter, we initiated a new position in Bajaj Auto (India: Consumer Discretionary), a leading manufacturer of automobiles. This is another company in the Bajaj stable that we believe represents a strong franchise with a high-quality steward behind it. It joins our existing position in Bajaj Holdings & Investment (India: Financials), which is the holding company of siblings Rajiv and Sanjiv Bajaj, who have an exemplary track record of delivering shareholder returns.

Elsewhere, we continued to build a position in Sundaram Finance (India: Financials), a high-quality and conservative financial services institution stewarded by the Sundaram Group. Meanwhile, to benefit from lower valuations, we added to our existing holdings in Tube Investments (India: Consumer Discretionary), Blue Dart Express (India: Industrials), SKF India (India: Industrials), Elgi Equipments (India: Industrials) and Cholamandalam Financial Holdings (India: Financials).

To fund these additions, we sold our positions in Havells (India: Industrials), Carborundum Universal (India: Materials) and Bosch India (India: Consumer Discretionary). Although we continue to believe in these businesses’ long-term growth potential, we believe there are better returns to be achieved elsewhere given their relative valuations.

The strategy’s performance over the past quarter (and over the past year) has been disappointing. We would have hoped that it would have exhibited greater resilience relative to the market. At the same time, however, we would caution that a single quarter is too short a timeframe over which to measure equity returns. When considering the future of the underlying businesses that we invest in, we look several years – and sometimes decades – into the future. On reflection, we could perhaps have trimmed position sizes more aggressively in our strongest performing industrial names. At the same time, however, we still see good value when considering their long-term potential.

The softness in the Indian market in recent months must be seen in the context of the strong returns that it has generated in recent years. Furthermore, equities are long-duration assets, so we continue to focus on the long-term growth potential of the companies we own. We have made three visits to India over the past four months and, in common with the corporate stewards backing our companies, we remain excited by the opportunity to generate compelling investment returns.

Source for company information: Stewart Investors investment team and company data. This stock information does not constitute any offer or inducement to enter into any investment activity. Portfolio data shown is from representative strategy accounts of the strategy shown above. Named new investments disclosed relate to holdings with a portfolio weight over 0.5%. It is not a recommendation or solicitation to purchase or invest in any fund. Differences between the representative account-specific constraints, currency or fees and those of a similarly managed fund or mandate would affect results.

Strategy update: Q4 2024

Indian Subcontinent All Cap strategy update: 1 October - 31 December 2024

One question we increasingly encounter when speaking to clients is: “isn’t India expensive now”? We can understand why clients are asking this, after all the MSCI India index has risen over 85% in the five years to end December 2024 and has increased by over 12% over the past 12 months alone.1

Two answers spring to mind here: firstly, that we are not investing in the index, we are trying to find the highest-quality companies we can and secondly, we keep a keen eye on valuations and position sizes to try and ensure our investments deliver good, long-term returns whilst also protecting capital. To that end we still see lots of reasons to be positive about the outlook for our India holdings.

We have found a few new ideas at acceptable valuations and during the period we purchased Narayana Health (India: Health Care) which is supplying affordable, private healthcare in India. We also increased our holding in insurer ICICI Lombard (India: Financials).

We sold Mahindra Finance (India: Financials) as we struggled to build conviction in the business trajectory.

As far as monitoring valuations, we slightly trimmed our holdings in Mahindra & Mahindra (India: Consumer Discretionary) and Dr. Lal PathLabs (India: Health Care). Our belief in their long-term success remains robust.

More generally, we continue to assess all our investments from a bottom-up perspective, trying to gauge the quality of the people and businesses that we are backing with your money. We are doing our best not to overpay for these investments and to hold them for the long term. We continue to believe that this is the bedrock of long-term capital preservation and growth.

[1] Source: FactSet. USD total returns.

Source for company information: Stewart Investors investment team and company data. This stock information does not constitute any offer or inducement to enter into any investment activity. Portfolio data shown is from representative strategy accounts of the strategy shown above. Named new investments disclosed relate to holdings with a portfolio weight over 0.5%. It is not a recommendation or solicitation to purchase or invest in any fund. Differences between the representative account-specific constraints, currency or fees and those of a similarly managed fund or mandate would affect results.

Strategy update: Q3 2024

Indian Subcontinent All Cap strategy update: 1 July - 30 September 2024

“Red-hot Indian market”,1 “India overtakes China in world’s biggest investable stock benchmark”,2 “Five undervalued qualities of the Indian economy”3 and so on and so on; one is hard pushed to find negative news on India’s economy or financial markets in mainstream financial media these days.

For us, India remains the same exciting investment destination that it has long been and for the same reasons too: a multitude of fantastic companies providing necessary goods and services to a rapidly developing population which leaves long-term and quality-focused investors spoilt for choice.

In terms of new positions, we bought ICICI Lombard (India: Financials), one of India’s largest private sector general insurance companies. ICICI Lombard is addressing the underinsurance gap in India by expanding access to insurance products to help individuals, businesses and families better manage risks. The company is well-managed and our conviction has grown enough to purchase for the strategy.

In the quarter, we increased our positions in Cholamandalam Financial Holdings (India: Financials), Aavas Financiers (India: Financials), Blue Dart Express (India: Industrials), Tata Communications (India: Communication Services) and SKF India (India: Industrials) as we believe they are all reasonably valued for good, long-term returns. We partially funded these by reducing our positions in CG Power (India: Industrials), as valuations continued to creep up, and HDFC Bank (India: Financials). We sold RBL Bank (India: Financials) and Kotak Mahindra Bank (India: Financials) as we felt there are currently better opportunities, at the margin, elsewhere.

Positive news flow notwithstanding, we continue to assess all our investments from a bottom-up perspective; trying to gauge the quality of the people and businesses that we are backing with your money, and doing our best not to overpay for these investments and to hold them for the long term. We continue to believe that this is the bedrock of long-term capital preservation and growth.

Source for company information: Stewart Investors investment team and company data. This stock information does not constitute any offer or inducement to enter into any investment activity. Portfolio data shown is from representative strategy accounts of the strategy shown above. Named new investments disclosed relate to holdings with a portfolio weight over 0.5%. It is not a recommendation or solicitation to purchase or invest in any fund. Differences between the representative account-specific constraints, currency or fees and those of a similarly managed fund or mandate would affect results.

Voting

Voting: Q2 2025

Indian Subcontinent All Cap voting: 1 April - 30 June 2025

Voting by country of origin

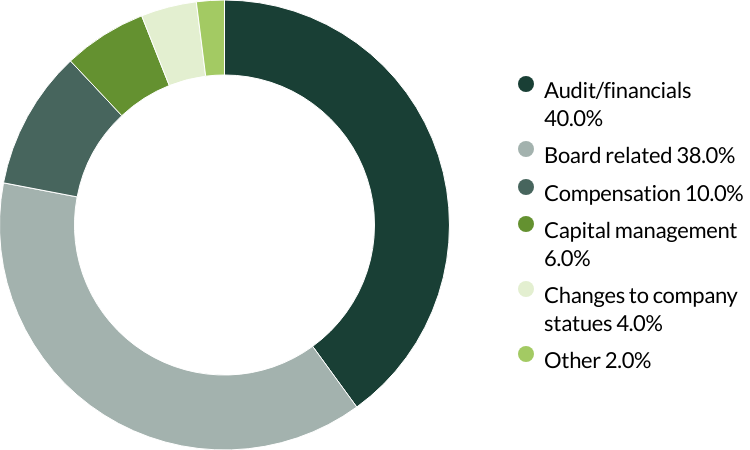

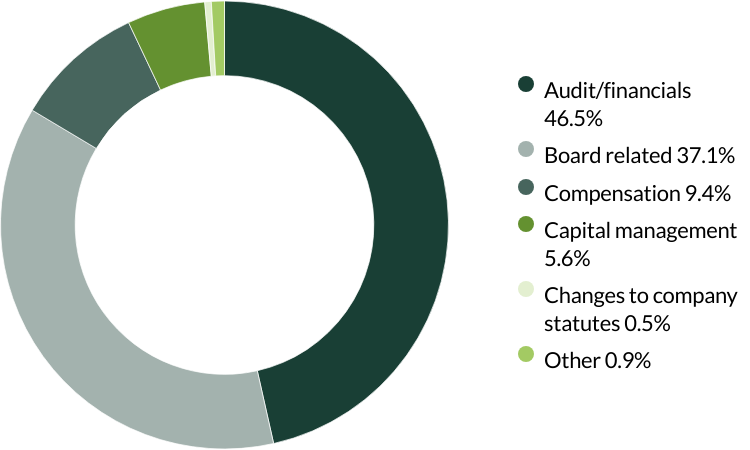

Voting by proposal category

During the quarter there were 50 proposals from 11 companies to vote on. On behalf of our clients, we did not vote against any proposals.

Source for company information: Stewart Investors investment team and company data. This stock information does not constitute any offer or inducement to enter into any investment activity. Portfolio data shown is from representative strategy accounts of the strategy shown above. Voting chart numbers may not add to 100 due to rounding. SHP means: Shareholder Proposal.

Voting: Q1 2025

Indian Subcontinent All Cap voting: 1 January - 31 March 2025

Voting by country of origin

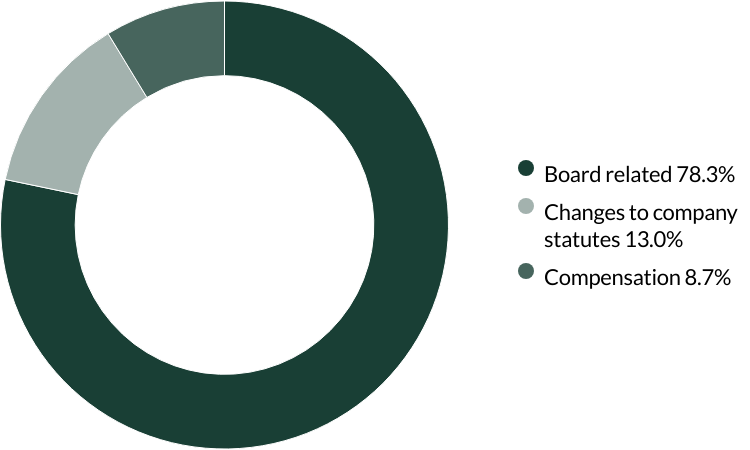

Voting by proposal category

During the quarter there were 23 resolutions from 11 companies to vote on. On behalf of clients, we voted against one resolution.

We voted against the election of a director and their remuneration at IndiaMART as we seek to encourage greater diversity and independence on the board. (one resolution)

Source for company information: Stewart Investors investment team and company data. This stock information does not constitute any offer or inducement to enter into any investment activity. Portfolio data shown is from representative strategy accounts of the strategy shown above. Voting chart numbers may not add to 100 due to rounding. SHP means: Shareholder Proposal.

Voting: Q4 2024

Indian Subcontinent All Cap voting: 1 October - 31 December 2024

Voting by country of origin

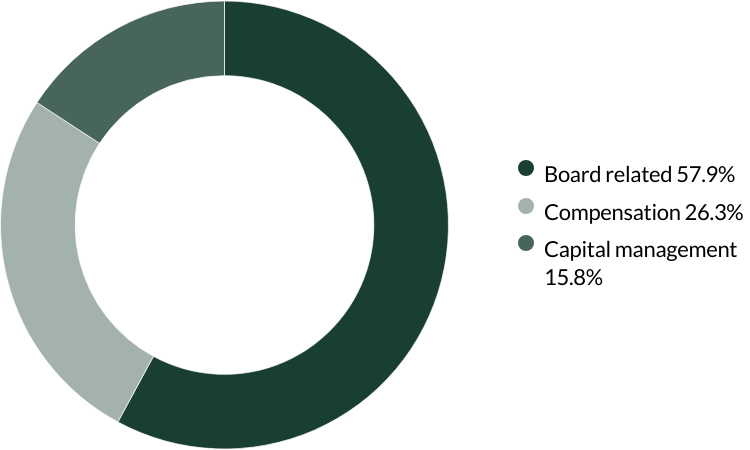

Voting by proposal category

During the quarter there were 19 resolutions from seven companies to vote on. On behalf of clients, we did not vote against any resolutions.

Source for company information: Stewart Investors investment team and company data. This stock information does not constitute any offer or inducement to enter into any investment activity. Portfolio data shown is from representative strategy accounts of the strategy shown above. Voting chart numbers may not add to 100 due to rounding. SHP means: Shareholder Proposal.

Voting: Q3 2024

Indian Subcontinent All Cap voting: 1 July - 30 September 2024

Voting by country of origin

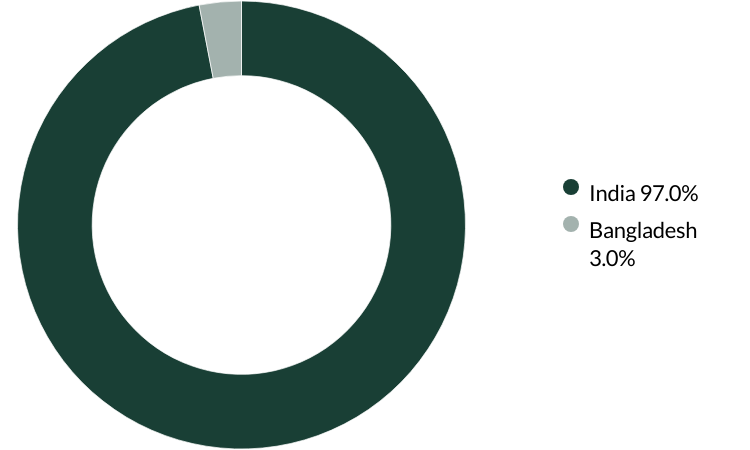

Voting by proposal category

During the quarter there were 213 resolutions from 29 companies to vote on. On behalf of clients, we did not vote against any resolutions.

Source for company information: Stewart Investors investment team and company data. This stock information does not constitute any offer or inducement to enter into any investment activity. Portfolio data shown is from representative strategy accounts of the strategy shown above. Voting chart numbers may not add to 100 due to rounding. SHP means: Shareholder Proposal.

Portfolio Explorer

If you are unable to view the portfolio explorer, please re-open in Google Chrome, Edge, Firefox, Safari or Opera. IE11 is not supported.

For illustrative purposes only. Reference to the names of example company names mentioned in this communication is merely for explaining the investment strategy and should not be construed as investment advice or investment recommendation of those companies. Companies mentioned herein may or may not form part of the holdings of Stewart Investors. Holdings are subject to change.

Certain statements, estimates, and projections in this document may be forward-looking statements. These forward-looking statements are based upon Stewart Investors’ current assumptions and beliefs, in light of currently available information, but involve known and unknown risks and uncertainties. Actual actions or results may differ materially from those discussed. Readers are cautioned not to place undue reliance on these forward-looking statements. There is no certainty that current conditions will last, and Stewart Investors undertakes no obligation to correct, revise or update information herein, whether as a result of new information, future events or otherwise.

Source: Stewart Investors investment team and company data. Securities mentioned are all investee companies* from representative Asia Pacific All Cap Strategy, Asia Pacific & Japan All Cap Strategy, Asia Pacific Leaders Strategy, European All Cap Strategy, European (ex UK) All Cap Strategy, Global Emerging Markets (ex China) Leaders Strategy, Global Emerging Markets Leaders Strategy, Global Emerging Markets All Cap Strategy, Indian Subcontinent All Cap Strategy, Worldwide All Cap Strategy and Worldwide Leaders Strategy accounts as at 30 June 2025. *Assets that the strategies may hold which an active decision has not been made, and sustainability assessment does not apply, include cash, cash equivalents, short-term holdings for the purpose of efficient portfolio management and holdings received as a result of mandatory corporate actions. Holdings of such assets will not appear on Portfolio Explorer. Not all strategies are available in all jurisdictions or to all audience types.

The Stewart Investors supports the Sustainable Development Goals (SDGs). The full list of SDGs can be found on the United Nations website.

Source for Climate Solutions and impact figures: © 2014–2025 Project Drawdown (drawdown.org). Source for Human Development Pillars: Stewart Investors investment team.

Source for climate solutions and human development analysis and mapping: Stewart Investors investment team. Contributions are defined by the team as demonstrable contributions to any solution, either direct (directly attributable to products, services or practices provided by that company), or enabling (supported or made possible by products or technologies provided by that company).

Investment terms

View our list of investment terms to help you understand the terminology within this website.

Fund data and information

Fund prices and details

Click on the links below to access key facts, literature, performance and portfolio information for the funds and share classes available in this jurisdiction:

Stewart Investors Indian Subcontinent All Cap Fund

Share prices are calculated on a forward pricing basis which means that the price at which you buy or sell will be calculated at the next valuation point after the transaction is placed. Where a fund price is marked XD, this means that the fund is currently Ex-Dividend. Past performance is not necessarily a guide to future performance. The value of shares and income from them may go down as well as up and is not guaranteed. Please note that the yield quoted above is not the historic yield. It is considered that the yield quoted represents the current position of investments, income and expenses in the fund and that this is a more accurate figure. Investors may be subject to tax on their distribution. The yield is not guaranteed or representative of future yields. You should be aware that any currency movements could affect the value of your investment. The Funds within the First Sentier Investors Global Umbrella Fund plc (Irish VCC) are denominated in USD or EUR.

Following the UK departure from the European Union, the First Sentier Investors ICVC, an open ended investment company registered in England and Wales ("OEIC") has ceased to qualify as a UCITS scheme and is instead an Alternative Investment Fund ("AIF") for European Union purposes under the terms of the Alternative Investment Fund Managers Directive (2011/61/EU). Accordingly, no marketing activities relating to the OEIC are being carried out by Stewart Investors in the European Union (or the additional EEA states) and the OEIC is not available for distribution in those jurisdictions. We have made documents available for existing EU investors in the ICVC which can be accessed here.

Strategy and fund name changes

As of end of 2024, please note that Stewart Investors strategies and the Funds within the UK First Sentier Investors ICVC, First Sentier Investors Global Umbrella Fund plc (Irish VCC) and First Sentier Investors Global Growth Funds (Singapore Unit Trust) have been renamed. Please refer to our note via the link below for further information.