Get the right experience for you. Please select your location and investor type.

Asia Pacific All Cap

This strategy aims to deliver long-term capital growth by investing in companies in the Asia Pacific region, including Australia and New Zealand but excluding Japan.

Download overviewOriginally launched in December 2005, this equity-only strategy aims to deliver long-term capital growth by investing in between 30-60 companies in the Asia Pacific region, including Australia and New Zealand but excluding Japan. As with all of our strategies, we are looking for businesses that are well positioned to contribute to, and benefit from, sustainable development.

Strategy highlights: a focus on quality and sustainability

- Companies must contribute to sustainable development. Portfolio Explorer >

- We invest in high-quality companies with exceptional cultures, strong franchises and resilient financials. How we pick companies >

- We avoid companies linked to harmful activities and engage and vote for positive change. Our position on harmful products >

- Our approach is long-term, bottom-up, high conviction and benchmark agnostic

- We focus on capital preservation as well as capital growth – we define risk as the permanent loss of client capital

Latest insights

Quarterly update

Strategy update: Q2 2025

Asia Pacific All Cap strategy update: 1 April - 30 June 2025

Shortly after the quarter began, President Trump announced his ‘Liberation Day’ tariffs. With China responding in kind, the prospect of a sharp contraction in global trade saw markets worldwide – including Asia – falling sharply.

Within a matter of days, however, a fall in the US dollar and the threat of a rout in the US government bond market encouraged the president to impose a 90-day moratorium on introducing many of his tariffs. As the world pulled back from an outright trade war, Asian markets rallied, with the gains being led by markets in the export-dominated economies of South Korea and Taiwan. Given our enthusiasm for a number of India’s high-quality, entrepreneurial companies, we were pleased to see share prices in that country starting to rally off the lows seen earlier in the year. The rally was aided by a cut in interest rates but also, we would argue, by valuations that appear attractive in view of those companies’ long-term growth potential.

Although share prices in some parts of Asia have recovered from the sell-off seen at the start of the quarter, the on/off discussions on tariffs have undoubtedly created lingering uncertainty. Some of the companies we have met are looking ahead to a potential resumption of talks on trade through the summer. Although we won’t try to predict their outcome, we would note that business leaders are often preparing for the worst while hoping for the best. While the market waits for greater clarity on trade, we continue as usual: seeking companies led by high-quality stewards, with strong franchises and resilient financials. We have found this combination provides resilience during periods of uncertainty.

During the quarter, we added five new investments. The first, Trip.com (China: Consumer Discretionary), is China’s largest online travel-booking platform. Its founders remain involved in the business and have seen it grow organically as well as through mergers and acquisitions. It survived the dead stop in tourism in the covid pandemic and now seems primed to take advantage of a shift to booking travel online. While only about 10% of the Chinese population currently has a passport that proportion is expected to increase1. Sea (Singapore: Communication Services) benefits from the growth of e-commerce, entertainment and digital financial services in demographically advantaged markets across Southeast Asia and Latin America. At this stage, we believe that its proven franchises would be almost impossible for would-be challengers to replicate.

Motilal Oswal Financial Services (India: Financials) is a financial conglomerate operating in retail and institutional broking, asset management, wealth management, investment banking, and housing finance. It is led by an ambitious-but-conservative steward and should benefit from meeting the savings and investment needs of India’s growing middle class. ICICI Lombard (India: Financials) is a private-sector general insurance provider. General insurance is one of the lowest penetrated services in India but Prime Minister Modi is committed to a programme of delivering ‘insurance for all’ by 2047; we believe it will benefit from this drive. Lastly, we added SM Investments (Philippines, Industrials), a conglomerate stewarded by the Sy family. It has investments in property, banking, and retail while also venturing into new areas such as logistics and geothermal energy.

To fund these purchases, we sold Hangzhou Robam (China: Consumer Discretionary), Bajaj Housing Finance (India: Financials) and Dr. Lal PathLabs (India: Health Care). We also sold Unicharm (Japan: Consumer Staples) due to concerns over its growth prospects.

We estimate that, of the holdings in our Asian portfolios, roughly three-quarters are primarily focused on selling to their domestic markets, offering them a useful buffer amid ongoing concerns about potential disruptions to international trade. With valuations across Asia currently standing at what we regard as extremely attractive levels, we remain confident in the prospects for returns from our carefully selected high-quality companies.

1 Source: Straits Times, 21 December 2023 ‘China is world’s second-largest economy but its passport is ranked 63rd. Are things looking up?’.

Source for company information: Stewart Investors investment team and company data. This stock information does not constitute any offer or inducement to enter into any investment activity. Portfolio data shown is from representative strategy accounts of the strategy shown above. Named new investments disclosed relate to holdings with a portfolio weight over 0.5%. It is not a recommendation or solicitation to purchase or invest in any fund. Differences between the representative account-specific constraints, currency or fees and those of a similarly managed fund or mandate would affect results.

Download a PDF copy

Select Strategy update and/or Proxy voting to produce a report. You can then download a copy of the report by clicking on the button.

You can build a bespoke report for all our strategies on the full Quarterly update report.

Strategy update: Q1 2025

Asia Pacific All Cap strategy update: 1 January - 31 March 2025

While broad Asia Pacific market indices edged slightly higher in both US dollar and Australian dollar terms, they moved slightly lower in euro and sterling terms. Perhaps of greater significance was that political turbulence resulted in a wide divergence of returns on a country level. Market indices in China, South Korea and Singapore moved higher but fell across the rest of the region, with some markets suffering double-digit falls.

Most notable was the extent of the divergence in returns between markets in India (down) and China (up). Investors’ enthusiasm for Chinese equities was, in part, a response to DeepSeek’s impressive demonstration of the progress the country is making in AI. Market-friendly rhetoric from the government in Beijing and hopes that the United States’ trade tariffs might not prove too onerous also helped to underpin the gains. In contrast, while there was relatively little news from India, share prices fell back from elevated levels, as they did in many other parts of the world; returns from the Indian market over the quarter were broadly in-line with those from markets in the United States.

During the quarter, we added new positions in S.F. Holding (China: Industrials), Mindray (China: Health Care) and Alibaba (China: Consumer Discretionary). We believe each of these companies has the potential to benefit from China’s new emphasis on national self-reliance. Over the last five years, the stewards of Chinese companies have, often for the first time, been tested by genuine economic and political adversity. They have applied the lessons learned during this period of adversity, strengthening their franchises and balance sheets. This, in combination with valuations that appear modest by global standards, means we have been identifying a greater number of new investment ideas in China.

We have also been finding quality companies at attractive valuations in the Philippines and India. As a result, the competition for a place in our portfolio has rarely been more intense and we were more active than normal over the quarter. As part of this, and in addition to the Chinese companies mentioned already, we added Bank of the Philippine Islands (Philippines: Financials) and BDO Unibank (Philippines: Financials). Both are family owned, professionally managed and attractively valued. They complement our existing investment in Ayala (Philippines: Industrials), to which we also added over the quarter.

In India, we added new holdings in Triveni Turbines (India: Industrials), a leading manufacturer of steam turbines and Bajaj Auto (India: Consumer Discretionary), a leading manufacturer of motorcycles, scooters and auto rickshaws backed by a high-quality steward. These are high-quality franchises whose share prices had been weak.

We sold out of ResMed (Australia: Health Care) partly for valuation reasons and partly due to its potential susceptibility to changes in US tariff policy. Similarly, we sold out of Syngene (India: Health Care), Dr. Reddy’s Laboratories (India: Health Care) and Cyient (India: Information Technology) because of their vulnerability to policy changes from the White House. We sold the holding in Tata Consumer Products (India: Consumer Staples) on valuation grounds. Finally, we sold ICICI Lombard (India Financials), IndiaMART (India: Industrials) and Koh Young Technology (South Korea: Information Technology). These were small positions and we had better ideas elsewhere.

To help finance the additions mentioned above, we trimmed our holdings in companies whose cashflows we believe are at greatest risk from the imposition of new tariffs by the Trump administration, such as CSL (Australia: Health Care), Fisher & Paykel Healthcare (New Zealand: Health Care) and Tech Mahindra (India: Information Technology). We continued to reduce the holding in TSMC (Taiwan: Information Technology) as evidence continued to mount that it is losing its discipline around capital expenditure.

As the long period of US exceptionalism draws to an end, we hope investors will begin to pay attention to the abundance of attractively valued companies to be found in the Asia Pacific region. Clearly, if the US economy falters and global demand falls, then economies across Asia will be impacted, albeit to differing degrees. We are also conscious that political risks appear to be rising in many Asian countries. Those risks, however, are far from uniform. The region’s technology complex, centred around Taiwan, South Korea and China, would appear to be particularly vulnerable to a global slowdown. India, by contrast, remains a domestically driven growth story and, as such, is somewhat isolated from the tumult in the global economy. The Philippines, meanwhile, could receive a significant economic boost if a global slowdown results in a meaningful fall in oil prices.

Predicting how any of today’s economic and geopolitical challenges will play out lies beyond our remit and our skillset. Fortunately, the Asian companies we invest in tend to have long memories; they still have the scar tissue formed during previous crises. These businesses have been forced to learn, to adapt and to become resilient. As a result, we believe they are set up not only to perform when conditions are fair but to navigate through whatever political and economic turbulence lies ahead.

Source for company information: Stewart Investors investment team and company data. This stock information does not constitute any offer or inducement to enter into any investment activity. Portfolio data shown is from representative strategy accounts of the strategy shown above. Named new investments disclosed relate to holdings with a portfolio weight over 0.5%. It is not a recommendation or solicitation to purchase or invest in any fund. Differences between the representative account-specific constraints, currency or fees and those of a similarly managed fund or mandate would affect results.

Strategy update: Q4 2024

Asia Pacific All Cap strategy update: 1 October - 31 December 2024

Over most three-month periods, there should be relatively little change in the portfolio. We aim to build resilient portfolios of high-quality companies with diversified streams of cash flows that have the ability to grow in value over the long term.

Chinese equities gave back some gains from the dramatic autumn stimulus which challenged comparative performance in the third quarter of 2024. The performance of the Indian market index struggled after some of the largest companies in India faced governance issues that became subject to enquiry by the regulator in the United States. The re-election of Mr Trump also seemed to distract global investors from Asian equities. At Stewart Investors we continue to concentrate on bottom-up stock selection rather than overly focus on unpredictable macro news flow.

The portfolio purchased DFI Retail Group (Hong Kong: Consumer Staples), a pan-Asian retailer stewarded by the Keswick family. We also purchased MANI (Japan: Health Care), a Japanese medical device company, Wesfarmers (Australia: Consumer Discretionary), an Australian conglomerate managing an evolving portfolio of retail and healthcare assets and Naver (South Korea: Communication Services), South Korea’s dominant internet search engine which has significantly improved its capital allocation in recent years.

During the quarter we took advantage of attractive valuations to add to our positions in AirTAC International (Taiwan: Industrials) and Yiheda Automation (China: Industrials).

Due to waning conviction, high valuations, or finding better ideas elsewhere, we sold Pentamaster (Malaysia: Information Technology), Advanced Energy Solution (Taiwan: Industrials) and Samsung C&T (South Korea: Industrials).

To control position sizes, we trimmed Mahindra & Mahindra (India: Consumer Discretionary), CG Power (India: Industrials), Marico (India: Consumer Staples), TSMC (Taiwan: Information Technology), Unicharm (Japan: Consumer Staples), Chroma ATE (Taiwan: Information Technology), CSL (Australia: Health Care) and Dr. Lal PathLabs (India: Health Care).

Views on investment opportunities in Asia have not changed; the strategy continues to look to invest in high-quality companies that are aligned with sustainable development. We look for stewards who are low profile, competent, long-term decision makers, franchises free from political agendas and financials that are resilient, not frail. Our focus is on quality, and we remain indifferent to many of the large, well-known companies, regardless of lower valuations.

Source for company information: Stewart Investors investment team and company data. This stock information does not constitute any offer or inducement to enter into any investment activity. Portfolio data shown is from representative strategy accounts of the strategy shown above. Named new investments disclosed relate to holdings with a portfolio weight over 0.5%. It is not a recommendation or solicitation to purchase or invest in any fund. Differences between the representative account-specific constraints, currency or fees and those of a similarly managed fund or mandate would affect results.

Strategy update: Q3 2024

Asia Pacific All Cap strategy update: 1 July - 30 September 2024

Over most three-month periods, there should be relatively little change in the portfolio. We aim to build resilient portfolios of high-quality companies with diversified streams of cash flows that have the ability to grow in value over the long term.

During the last few days of the quarter the Chinese central bank and government announced monetary and fiscal stimulus measures for the economy, causing Chinese stocks to rally significantly. Whilst it is heartening to see the Chinese authorities attempting to address the issues within the economy it remains unclear whether this stimulus will adequately address structural issues like the lack of consumer demand.

The portfolio purchased ICICI Lombard (India: Financials), a conservatively run insurer set to potentially benefit from rising insurance penetration in India. We purchased Ayala (Philippines: Industrials), a 190-year-old Filipino conglomerate stewarded by the Ayala family who in recent years have appointed the first ever non-family CEO. We also initiated a position in Yiheda Automation (China: Industrials), China’s leading supplier of factory automation components that we believe has the opportunity to consolidate a largely informal market whilst benefiting from the automation of Chinese factories.

During the quarter we continued to add to Techtronic Industries (Hong Kong: Industrials) and increased our position in Tata Communications (India: Communication Services).

We controlled the position size of our large holding in Mahindra & Mahindra (India: Consumer Discretionary), and also trimmed Cochlear (Australia: Health Care), Chroma ATE (Taiwan: Information Technology), Syngene (India: Health Care), Fisher & Paykel Healthcare (New Zealand: Health Care), and Unicharm (Japan: Consumer Staples).

We sold RBL Bank (India: Financials) and Unilever Indonesia (Indonesia: Consumer Staples), both of which were smaller positions that we struggled to build conviction in. We also sold Kotak Mahindra Bank (India: Financials) to fund better ideas elsewhere.

Views on investment opportunities in Asia have not changed; the strategy continues to look to invest in high-quality companies that are aligned with sustainable development. We look for stewards who are low profile, competent, long-term decision makers, franchises free from political agendas and financials that are resilient, not frail. Our focus is on quality, and we remain indifferent to many of the large, well-known companies, regardless of lower valuations.

Source for company information: Stewart Investors investment team and company data. This stock information does not constitute any offer or inducement to enter into any investment activity. Portfolio data shown is from representative strategy accounts of the strategy shown above. Named new investments disclosed relate to holdings with a portfolio weight over 0.5%. It is not a recommendation or solicitation to purchase or invest in any fund. Differences between the representative account-specific constraints, currency or fees and those of a similarly managed fund or mandate would affect results.

Voting

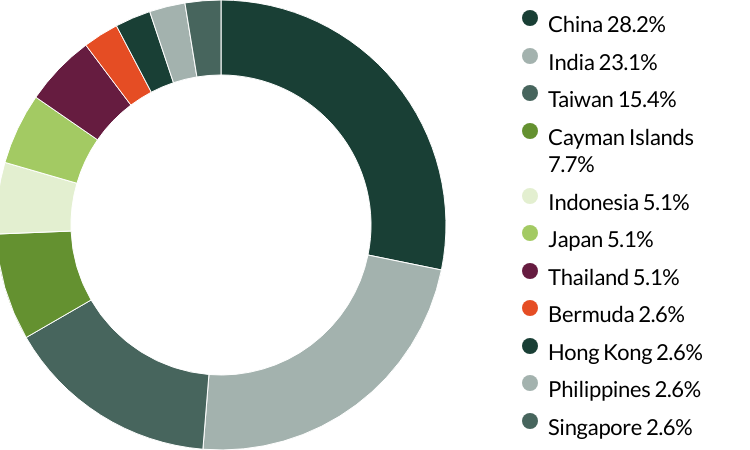

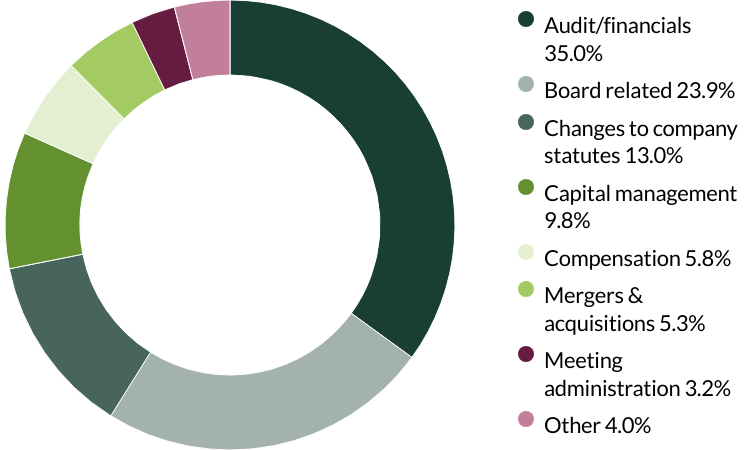

Voting: Q2 2025

Asia Pacific All Cap voting: 1 April - 30 June 2025

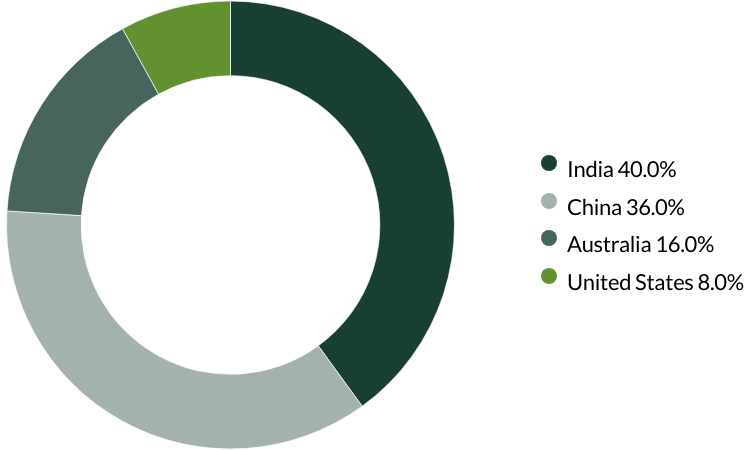

Voting by country of origin

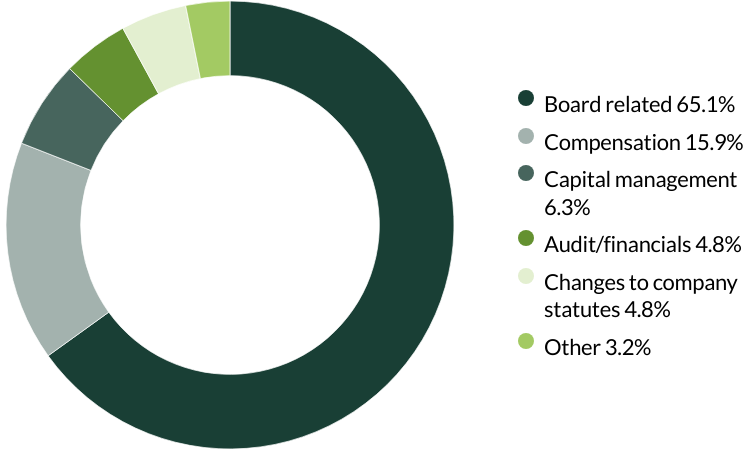

Voting by proposal category

During the quarter there were 377 proposals from 35 companies to vote on. On behalf of our clients, we voted against six proposals.

We voted against proposals on transaction of business at Ayala and Kasikornbank, as they did not provide enough information about the proposals. We wanted to avoid giving unrestricted decision-making power without sufficient clarity. (three proposals)

We voted against the appointment of the auditor at Glodon as they have been in place for over 10 years. The company has given no information on rotating its auditors, a practice we believe is important to ensure a fresh perspective is brought to its accounts. (one proposal)

We voted against the election of a director at Trip.com due to the company's lack of disclosure regarding director attendance, the number of board meetings held, and the voting results from the previous year. Our aim is to encourage greater transparency and the adoption of global governance standards. (one proposal)

We voted against a request for approval to invest in wealth management products at Zhejiang Supor as we believe it carries excessive risk relative to the limited additional returns these products would provide. Making such financial investments is not central to the business and we believe surplus cash is better kept in time deposits at banks. (one proposal)

Source for company information: Stewart Investors investment team and company data. This stock information does not constitute any offer or inducement to enter into any investment activity. Portfolio data shown is from representative strategy accounts of the strategy shown above. Voting chart numbers may not add to 100 due to rounding. SHP means: Shareholder Proposal.

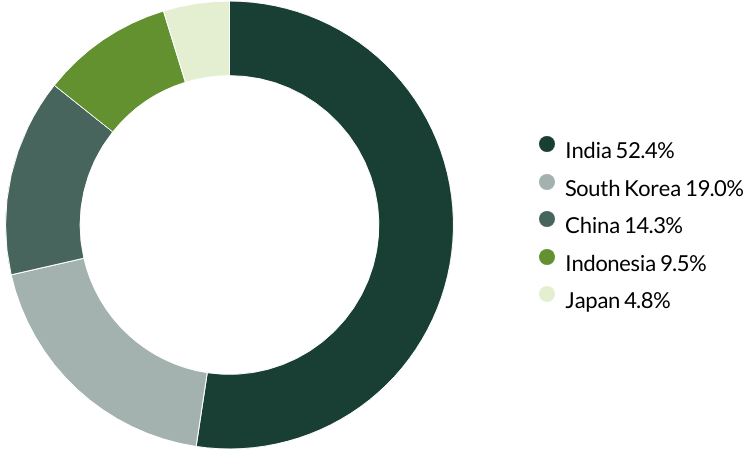

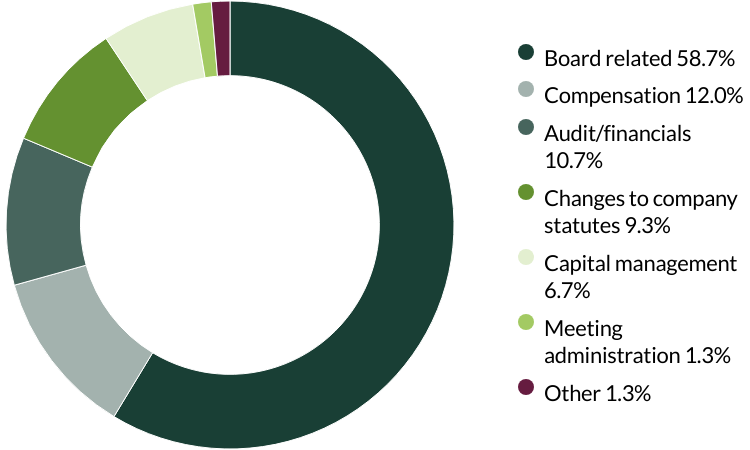

Voting: Q1 2025

Asia Pacific All Cap voting: 1 January - 31 March 2025

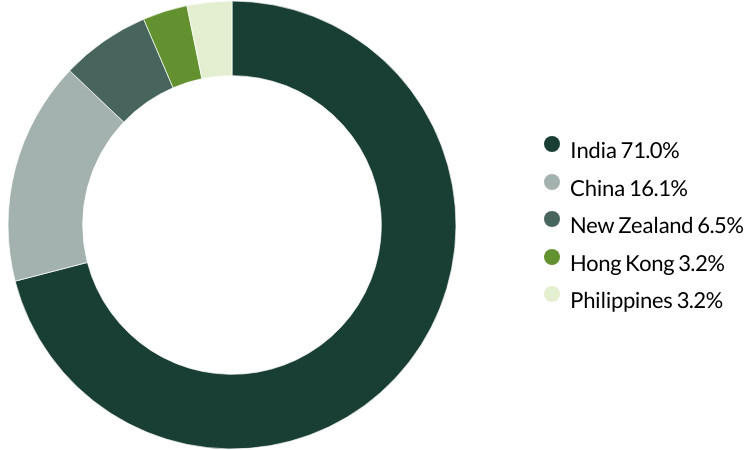

Voting by country of origin

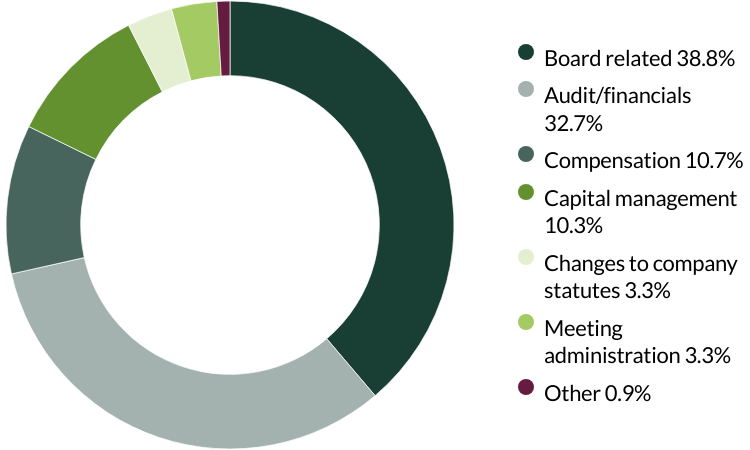

Voting by proposal category

During the quarter there were 75 resolutions from 20 companies to vote on. On behalf of clients, we voted against six resolutions.

We voted against executive remuneration at Bank Central Asia because we believed it was excessive. (one resolution)

We voted against the election of a director and their remuneration at IndiaMART as we seek to encourage greater diversity and independence on the board. (one resolution)

We voted against the election of two directors and an audit committee member at Samsung Electronics as we do not believe them to be truly independent. (three resolutions)

We voted against the election of the audit committee chair at Unicharm as we do not believe they are independent. (one resolution)

Source for company information: Stewart Investors investment team and company data. This stock information does not constitute any offer or inducement to enter into any investment activity. Portfolio data shown is from representative strategy accounts of the strategy shown above. Voting chart numbers may not add to 100 due to rounding. SHP means: Shareholder Proposal.

Voting: Q4 2024

Asia Pacific All Cap voting: 1 October - 31 December 2024

Voting by country of origin

Voting by proposal category

During the quarter there were 63 resolutions from 12 companies to vote on. On behalf of clients, we voted against eight resolutions.

At ResMed, we voted against the Board re-election of Peter C. Farrell who retired from the company over 10 years ago and believe should step down from the Board. We also voted against the re-election of Richard Sulpizio as Chair of the nominating and governance committee, due to the decreasing gender diversity on the Board. We voted against the company’s executive remuneration and payment terms, as we have concerns around the complexity and use of many adjusted metrics. We also voted against the re-appointment of the auditor as they have been in place for over 10 years and the company has given no information on intended rotation which we believe is important for ensuring a fresh perspective on the financial accounts. (eight resolutions)

Source for company information: Stewart Investors investment team and company data. This stock information does not constitute any offer or inducement to enter into any investment activity. Portfolio data shown is from representative strategy accounts of the strategy shown above. Voting chart numbers may not add to 100 due to rounding. SHP means: Shareholder Proposal.

Voting: Q3 2024

Asia Pacific All Cap voting: 1 July - 30 September 2024

Voting by country of origin

Voting by proposal category

During the quarter there were 214 resolutions from 27 companies to vote on. On behalf of clients, we voted against three resolutions.

We voted against the appointment of the auditor at Philippine Seven as they have been in place for over ten years. The company has given no information on intended rotation which we believe is important for ensuring a fresh perspective on the accounts. We also voted against proposals on transaction of business, as the company did not provide enough information about the proposals. We wanted to avoid giving them unrestricted decision-making power without sufficient clarity. (two resolutions)

We voted against the appointment of the auditor at Vitasoy as they have been in place for over ten years. The company has given no information on intended rotation which we believe is important for ensuring a fresh perspective on the accounts. (one resolution)

Source for company information: Stewart Investors investment team and company data. This stock information does not constitute any offer or inducement to enter into any investment activity. Portfolio data shown is from representative strategy accounts of the strategy shown above. Voting chart numbers may not add to 100 due to rounding. SHP means: Shareholder Proposal.

Portfolio Explorer

If you are unable to view the portfolio explorer, please re-open in Google Chrome, Edge, Firefox, Safari or Opera. IE11 is not supported.

For illustrative purposes only. Reference to the names of example company names mentioned in this communication is merely for explaining the investment strategy and should not be construed as investment advice or investment recommendation of those companies. Companies mentioned herein may or may not form part of the holdings of Stewart Investors. Holdings are subject to change.

Certain statements, estimates, and projections in this document may be forward-looking statements. These forward-looking statements are based upon Stewart Investors’ current assumptions and beliefs, in light of currently available information, but involve known and unknown risks and uncertainties. Actual actions or results may differ materially from those discussed. Readers are cautioned not to place undue reliance on these forward-looking statements. There is no certainty that current conditions will last, and Stewart Investors undertakes no obligation to correct, revise or update information herein, whether as a result of new information, future events or otherwise.

Source: Stewart Investors investment team and company data. Securities mentioned are all investee companies* from representative Asia Pacific All Cap Strategy, Asia Pacific & Japan All Cap Strategy, Asia Pacific Leaders Strategy, European All Cap Strategy, European (ex UK) All Cap Strategy, Global Emerging Markets (ex China) Leaders Strategy, Global Emerging Markets Leaders Strategy, Global Emerging Markets All Cap Strategy, Indian Subcontinent All Cap Strategy, Worldwide All Cap Strategy and Worldwide Leaders Strategy accounts as at 30 June 2025. *Assets that the strategies may hold which an active decision has not been made, and sustainability assessment does not apply, include cash, cash equivalents, short-term holdings for the purpose of efficient portfolio management and holdings received as a result of mandatory corporate actions. Holdings of such assets will not appear on Portfolio Explorer. Not all strategies are available in all jurisdictions or to all audience types.

The Stewart Investors supports the Sustainable Development Goals (SDGs). The full list of SDGs can be found on the United Nations website.

Source for Climate Solutions and impact figures: © 2014–2025 Project Drawdown (drawdown.org). Source for Human Development Pillars: Stewart Investors investment team.

Source for climate solutions and human development analysis and mapping: Stewart Investors investment team. Contributions are defined by the team as demonstrable contributions to any solution, either direct (directly attributable to products, services or practices provided by that company), or enabling (supported or made possible by products or technologies provided by that company).

Investment terms

View our list of investment terms to help you understand the terminology within this website.

Fund data and information

Fund prices and details

Click on the links below to access key facts, literature, performance and portfolio information for the funds and share classes available in this jurisdiction:

Stewart Investors Asia Pacific All Cap Fund

| Fund name | Fund type | Currency | Price | Daily change | Price date | Factsheet |

|---|---|---|---|---|---|---|

| Stewart Investors Asia Pacific All Cap Class I (Acc) | Irish UCITs | EUR | 11.88 | 0.30 | 22 Aug 2025 | |

| Stewart Investors Asia Pacific All Cap Class I (Acc) | Irish UCITs | SGD | 9.88 | -0.01 | 22 Aug 2025 | |

| Stewart Investors Asia Pacific All Cap Class I (Acc) | Irish UCITs | USD | 10.99 | -0.20 | 22 Aug 2025 | |

| Stewart Investors Asia Pacific All Cap Class VI (Acc) | Irish UCITs | EUR | 3.62 | 0.30 | 22 Aug 2025 | |

| Stewart Investors Asia Pacific All Cap Class VI (Dist) | Irish UCITs | GBP | 9.94 | 0.27 | 22 Aug 2025 | |

| Stewart Investors Asia Pacific All Cap Class VI (Acc) | Irish UCITs | USD | 14.70 | -0.20 | 22 Aug 2025 |

Share prices are calculated on a forward pricing basis which means that the price at which you buy or sell will be calculated at the next valuation point after the transaction is placed. Where a fund price is marked XD, this means that the fund is currently Ex-Dividend. Past performance is not necessarily a guide to future performance. The value of shares and income from them may go down as well as up and is not guaranteed. Please note that the yield quoted above is not the historic yield. It is considered that the yield quoted represents the current position of investments, income and expenses in the fund and that this is a more accurate figure. Investors may be subject to tax on their distribution. The yield is not guaranteed or representative of future yields. You should be aware that any currency movements could affect the value of your investment. The Funds within the First Sentier Investors Global Umbrella Fund plc (Irish VCC) are denominated in USD or EUR.

Following the UK departure from the European Union, the First Sentier Investors ICVC, an open ended investment company registered in England and Wales ("OEIC") has ceased to qualify as a UCITS scheme and is instead an Alternative Investment Fund ("AIF") for European Union purposes under the terms of the Alternative Investment Fund Managers Directive (2011/61/EU). Accordingly, no marketing activities relating to the OEIC are being carried out by Stewart Investors in the European Union (or the additional EEA states) and the OEIC is not available for distribution in those jurisdictions. We have made documents available for existing EU investors in the ICVC which can be accessed here.

Strategy and fund name changes

As of end of 2024, please note that Stewart Investors strategies and the Funds within the UK First Sentier Investors ICVC, First Sentier Investors Global Umbrella Fund plc (Irish VCC) and First Sentier Investors Global Growth Funds (Singapore Unit Trust) have been renamed. Please refer to our note via the link below for further information.