Get the right experience for you. Please select your location and investor type.

European Sustainability

The strategy was launched in June 2021 and invests in 30-45 companies that we consider to be the very best sustainability companies in Europe (including the UK).

Our European Sustainability strategy invests in companies that we consider to be the very best sustainability companies in Europe. These businesses have strong and competitive franchises, exceptional people and distinctive cultures, and resilient financials. Individually and collectively they are solving difficult problems, meeting critical needs, and helping bring about a more sustainable future.

By focusing on the highest quality and best sustainability companies in Europe, we believe we can offer an exciting portfolio that stands out from the crowd.

Why invest in European companies?

World-leading sustainability companies

- Europe has a large listed universe, including world-leading health care, clean energy, manufacturing and IT companies

- Many of these companies have large and growing end-markets, including in many emerging economies, and a strong presence globally and locally

Exceptional people and cultures

- Many companies are run by outstanding management teams and are often controlled by long-term stewards – foundations, families and entrepreneurs

- Europe has a high concentration of companies with strong cultures, great franchises, and healthy balance sheets and financial characteristics

Sustainability tailwinds

- Social norms, policies and regulations are often favourable for companies advancing sustainable technologies and solutions

- European companies are known and respected for setting high standards

Strategy highlights: a focus on quality and sustainability

- Companies must contribute to sustainable development. Portfolio Explorer >

- We invest in high-quality companies with exceptional cultures, strong franchises and resilient financials. How we pick companies >

- We avoid companies linked to harmful activities and engage and vote for positive change. Our position on harmful products >

- Our approach is long-term, bottom-up, high conviction and benchmark agnostic

- We focus on capital preservation as well as capital growth – we define risk as the permanent loss of client capital

Latest insights

Quarterly updates

Strategy update: Q1 2024

European Sustainability strategy update: 1 January - 31 March 2024

Following a stronger performance profile in the last quarter of 2023, the first quarter of 2024 has been relatively flat. The strategy portfolio performance was behind the MSCI AC Europe Index which was boosted in part by easing monetary policy and hopes for a soft economic landing.

During the quarter we took the opportunity to build up some of the newer positions we added in 2023, including Teqnion (Sweden: Industrials), the founder owned, serial acquirer of diverse businesses; Nexans (France: Industrials), the maker of electrical cabling used in renewable energy, and DiscoverIE (United Kingdom: Industrials), a manufacturer of niche electronics and manufacturing businesses. We also took the opportunity to add to our holding in Endava (United Kingdom: Information Technology) which suffered a sharp sell-off over market concerns about weaker discretionary spend from customers. While the company may face short-term uncertainty due to macro conditions, we feel confident backing its culture, stewardship and long-term growth potential.

Judges Scientific (United Kingdom: Industrials), the largest position in the strategy, continues to demonstrate resilient growth, and we remain excited about its potential, given it is still early on in its growth journey.

Valuation concerns and a need to manage position sizes led us to trim positions in Ringkjøbing Landbobank (Denmark: Financials), Nemetschek (Germany: Information Technology) and Adyen (Netherlands: Financials). Adyen had a particularly strong quarter, rising more than 145%1 since a period of weakness last year.

Over the course of the quarter, we exited Komerční banka (Czech Republic: Financials) to make room for two faster growing eastern European companies: Dino Polska (Poland: Consumer Staples), a vertically integrated, low-cost grocery retailer, and Allegro (Poland: Consumer Staples), Poland’s number one e-commerce platform that is expanding into Eastern Europe.

As ever, we continue to focus on long-term capital preservation as the bedrock of capital appreciation, and on ensuring the portfolio can weather most macro environments. Looking forward, we are excited by the quality, and diverse nature of the companies we hold, and their ability to contribute to, and benefit from, sustainable development.

1 Source: Factset

Source for company information: Stewart Investors investment team and company data. This stock information does not constitute any offer or inducement to enter into any investment activity. Portfolio data shown is from representative strategy accounts of the strategy shown above. Named new investments disclosed relate to holdings with a portfolio weight over 0.5%. It is not a recommendation or solicitation to purchase or invest in any fund. Differences between the representative account-specific constraints, currency or fees and those of a similarly managed fund or mandate would affect results.

Download a PDF copy

Select Strategy update and/or Proxy voting to produce a report. You can then download a copy of the report by clicking on the button.

You can build a bespoke report for all our strategies on the full Quarterly update report.

Strategy update: Q4 2023

European Sustainability strategy update: 1 October - 31 December 2023

Strong performance in Q4 propelled overall performance for the year convincingly into positive territory. Nonetheless 2023 will be remembered for market turbulence and fluctuations in the performance of the strategy.

The period from August through to October was especially difficult. Many macroeconomic worries that had weighed on equity markets at different times earlier in the year came to a head: monetary and fiscal policy tightness across European economies, the threat of recession and stagnation, falling real wages, declining household savings and spending, vulnerable housing markets, and slowing demand from China.

However, sentiment improved markedly in the final quarter as a consensus emerged that interest rates have peaked. Yields plummeted and valuations rose as markets celebrated a more benign inflation outlook and the possibility that the monetary policy tightening cycle is over, the industrial cycle turning, and demand recovering.

All but six of the 43 portfolio holdings rose over the quarter. Valuation concerns and a need to manage position sizes led us to trim positions in Admiral (United Kingdom: Financials), bioMérieux (France: Health Care), Atlas Copco (Sweden: Industrials), DHL Group (Germany: Industrials), and Infineon Technologies (Germany: Information Technology). We also sold the small remaining position in Rational (Germany: Industrials). The company has a limited range of products which we are concerned could face growing competitive and pricing pressures.

We made no new purchases, but took advantage of attractive valuation opportunities to increase shareholdings in EPAM Systems (United States: Information Technology), Jerónimo Martins (Portugal: Consumer Staples), Alfen (Netherlands: Industrials), Elisa (Finland: Communication Services), and Judges Scientific (United Kingdom: Industrials).

Over the course of the year our main concerns were to: 1) maintain and improve portfolio diversification and defensiveness; 2) maintain valuation discipline; and 3) take advantage of compelling valuation opportunities. In total we sold out of five holdings and introduced seven new names into the portfolio.

We replaced a handful of industrial companies because they became too expensive and/or their competitive positioning less convincing to us. They included Beijer Ref (Sweden: Industrials), Nibe Industrier (Sweden: Industrials), Tomra (Norway: Industrials), and Rational (mentioned previously). We also sold Diploma (United Kingdom: Industrials) to make room in the portfolio for DiscoverIE (United Kingdom: Industrials), a somewhat similar company to Diploma, although earlier in its evolution, and less expensive.

The four industrial companies we brought into the portfolio were Nexans (France: Industrials), Teqnion (Sweden: Industrials), Assa Abloy (Sweden: Industrials), and Addtech (Sweden: Industrials). All apart from Nexans have contributed positively to performance. The other two new positions were in EPAM Systems (mentioned previously) and Endava (United States: Information Technology). Both looked beaten up when we bought them, and both have strengthened since.

The most disappointing aspect of performance in 2023 was the damage done by the health care holdings, many of which were among the larger portfolio positions, precisely because we expect them to be resilient and steady compounders over the long term.

Three of the five largest detractors from performance were DiaSorin (Italy: Health Care), Roche (Switzerland: Health Care), and Carl Zeiss Meditec (Germany: Health Care). The other two big detractors were Alfen (Netherlands: Industrials) and Tecan (Switzerland: Health Care). We could have been less eager and slower adding to all five holdings as they fell.

The top five performance contributions in 2023 came from holdings in Inficon (Switzerland: Information Technology), Atlas Copco, DHL Group, Teqnion (all mentioned previously), and Spectris (United Kingdom: Information Technology); we reduced shareholdings in all except Teqnion and Spectris.

We have no ability to forecast markets, though it wouldn’t surprise us if 2024 presents a complex market environment with contradictory forces and signals. Optimism about equities may be running higher than it has for a couple of years, but markets have been swift to price in lower interest rates and some company valuations are already starting to look stretched. Easier financial conditions may be on the horizon, but money and credit remain tight in many economies. We may not yet have seen the full impacts of the tightening cycle we have been through. If economic activity fails to pick up, or contracts, company earnings could come under renewed pressure, and balance sheet strength and liquidity could be tested.

We enter 2024 with a portfolio of what we believe to be adaptable, high-quality, great sustainability companies, with consistent cash flow capabilities, and strong competitive positions in different market segments. The leaders of these companies understand the value of staying close to their customers. They steward their balance sheets carefully. They ensure their companies are as well placed to deal with emergent risks as they are to capitalise on long-term opportunities.

We will stay focused on the long-term, fundamental prospects of the companies we hold and those we are watching closely. Although we like the composition and shape of the portfolio, we will keep searching for companies that might improve overall portfolio risk-return characteristics. We will be vigilant about trimming holdings that become expensive and adding to those that present compelling valuations opportunities.

Source for company information: Stewart Investors investment team and company data. This stock information does not constitute any offer or inducement to enter into any investment activity. Portfolio data shown is from representative strategy accounts of the strategy shown above. Named new investments disclosed relate to holdings with a portfolio weight over 0.5%. It is not a recommendation or solicitation to purchase or invest in any fund. Differences between the representative account-specific constraints, currency or fees and those of a similarly managed fund or mandate would affect results.

Strategy update: Q3 2023

European Sustainability strategy update: 1 July - 30 September 2023

In what was a turbulent quarter for many financial markets, European equities felt the chilling effects of fears about recession and economic stagnation in the eurozone, rising yields, persistent monetary and fiscal policy tightness, resurgent energy prices, falling real wages, a depletion of household savings built up during the pandemic, lacklustre retail spending, fragile housing markets, and slowing demand from China.

The strategy registered a painful decline, more than erasing the gains of the first half of the year. The share prices of all but a quarter of portfolio holdings fell, and a handful experienced double-digit declines. The largest negative contribution came from Adyen (Netherlands: Financials), a facilitator of e-commerce, mobile, and point-of-sale payments. The share price fell sharply after the company reported weaker US revenue growth and margin pressure arising from increased hiring.

Alfen (Netherlands: Industrials) a provider of smart grids, electric vehicle (EV) charging stations and energy storage solutions, also fell as sales in their EV charging station segment weakened due to customer destocking. And DiscoverIE (UK: Industrials), a serial acquirer of niche electronics design and manufacturing businesses, de-rated against an uncertain macro backdrop and concern that higher interest rates will curtail the growth contribution of acquisitions.

Positive contributions came from Admiral Group (UK: Financials), a UK auto and home insurance provider; Bechtle (Germany: Information Technology), a pan-European provider of IT infrastructure and services; and EPAM Systems (US: Information Technology), the Eastern European IT consulting and digital transformation services company which was added to the portfolio in Q2.

Two new companies were brought into the portfolio last quarter. Addtech (Sweden: Industrials) is a family-stewarded acquirer and long-term owner of more than 150 electrification, clean energy, automation, and process technology businesses. These tend to be relatively small private businesses with leading market positions, led by exceptional management teams. The business model is highly decentralised and the acquisition philosophy fosters entrepreneurship, collaboration and accountability. We took advantage of a compelling opportunity after the company de-rated.

Endava (US: Information Technology) was also added to the portfolio as its valuation became attractive. It is a founder-controlled provider of digital transformation consultancy services, mainly to customers active in payments, financial services and the technology, media and telecommunications sector. An entrepreneurial, flexible, team-focused culture has enabled successful expansion and scaling of the business. Around three-quarters of the workforce are in the greater-European region, but Endava’s revenue base and delivery footprint are expanding in the Americas and Asia.

In an effort to further improve portfolio diversification and resilience, we increased positions in Beiersdorf (Germany: Consumer Staples) and Unilever (UK: Consumer Staples). We also added to several holdings as they became more attractively valued, including Adyen (previously mentioned), Indutrade (Sweden: Industrials), an industrial holding company with over 200 subsidiaries; Assa Abloy (Sweden: Industrials), a leader in locks, doors and intelligent security systems; and Roche (Switzerland: Health Care), a developer of biologic drugs for rare diseases and in-vitro diagnostics.

Caution about valuations, position sizes and risk-return prospects led us to trim positions in Vitec Software (Sweden: Information Technology), a serial acquirer of leading niche software businesses; Sartorius (Germany: Health Care), a provider of laboratory and drug development technologies; ALK-Abelló (Denmark: Health Care), the global leader in allergen immunotherapy treatments; and Bechtle and Admiral (among the positive contributors mentioned previously).

Economic risks and headwinds are intensifying and multiplying. We ask ourselves repeatedly if the portfolio is as resilient as it can be. We have conviction in the quality of the companies we hold, and we like the composition and shape of the portfolio. However, we never stop searching for companies that might improve overall portfolio risk-return characteristics.

Patience and a long-term focus are especially important at a time like this. We challenge ourselves to look through short-term noise and take advantage of attractive valuation opportunities. And we remain just as vigilant about trimming positions in companies whose valuations become stretched.

Source for company information: Stewart Investors investment team and company data. This stock information does not constitute any offer or inducement to enter into any investment activity. Portfolio data shown is from representative strategy accounts of the strategy shown above. Named new investments disclosed relate to holdings with a portfolio weight over 0.5%. It is not a recommendation or solicitation to purchase or invest in any fund. Differences between the representative account-specific constraints, currency or fees and those of a similarly managed fund or mandate would affect results.

Strategy update: Q2 2023

European Sustainability strategy update: 1 April - 30 June 2023

In order to gauge a company’s performance prospects, we must try to grasp the context in which it operates. Seen through the abstract lens of news, the world usually seems profoundly chaotic, hostile, erratic and unfathomable. The world may be all these things, but all these things are not the singular context in which companies operate. We need a different, better frame of reference.

The more uncertain the political economy context and market conditions get, the harder and closer we look at what we can best make sense of: companies, and how well they deal with the particular contextual challenges they face and foresee. Companies are of course impacted by developments in the political economy and financial markets, but company leaders deal with the manifestations of these things in amongst the practical realities of employees, customers, supply chains, production facilities, distribution channels, and regulatory environments.

Performance over the quarter was mixed. Encouraging results and positive outlooks boosted the share prices of Jerónimo Martins (Portugal: Consumer staples), the leading supermarket operator in Poland; Judges Scientific (UK: Industrials), a serial acquirer of specialised scientific instruments businesses; and Atlas Copco (Sweden: Industrials), a maker of compressors, vacuums, and industrial assembly technologies.

Companies that dragged most on performance included Carl Zeiss Meditec (Germany: Health Care) – a maker of ophthalmic devices and microsurgery visualisation technologies – which fell after the company confirmed slower growth in China due to covid infection waves and lockdowns earlier in the year; Sartorius (Germany: Health Care) – a provider of laboratory and drug development technologies – which issued a profit warning due to falling sales as biopharma customers run off inventories built up during the pandemic; and ALK-Abelló (Denmark: Health Care) – the global leader in allergen immunotherapy treatments – which fell when first quarter data showed softer European tablet sales growth.

Two new companies were brought into the portfolio. Assa Abloy (Sweden: Industrials) is a global leader in locks, doors and intelligent security systems. It operates in fragmented end-markets where success depends on winning and maintaining trust. Its electromechanical, digital and automated access systems are helping save energy and regulate airflow and temperature in buildings. Although sales are linked to the property cycle, significant revenues from after-market upgrades and other services help smooth the overall revenue and margin profile.

EPAM Systems (US: Information Technology) is a founder-controlled, Eastern European IT services company that is helping accelerate digital transformation and productivity gains for its clients. EPAM is known in its field as the developers’ developer. The exceptional platform engineering and software development skills of its workforce, most of whom are based in Eastern Europe, and a full consult-design-engineer-operate model, have enabled it to establish long-term relationships with leading companies in over 35 countries worldwide.

We continued building positions in companies bought during the first quarter, including DiscoverIE (UK: Industrials) a serial acquirer of electronics design and manufacturing businesses; and Teqnion (Sweden: Industrials), a serial acquirer of a wide range of specialised industrial and technology businesses. We also added to several holdings as they became more attractively valued, including Alfen (Netherlands: Industrials), a provider of electric vehicle charging stations as well as smart grid and energy storage solutions; and Infineon Technologies (Germany: Information Technology), a provider of semiconductors for the auto, industrial and power management sectors.

We sold out of Tomra Systems (Norway: Industrials), which makes automated recycling, sorting and reverse vending technologies. These technologies could slide down lists of spending priorities if economies slip into recession. At current valuations we believe Tomra may struggle to generate an adequate return over the next decade. It seems wise to deploy capital to other portfolio companies.

Valuation concerns were the main reason for trimming positions in Tecan (Switzerland: Health Care), a maker of laboratory automation devices; Elisa (Finland: Communication Services), the market leader in telecommunications and digital services in Finland; and Inficon (Switzerland: Information Technology), a maker of niche gas detection equipment and sensors.

We seek out exceptional leaders of companies with adaptable franchises and solid balance sheets – companies that can thrive in good times as well as bad. We strive to hold companies which, in combination, can help make the portfolio resilient across a range of fast-fluctuating market environments. The goal of consistently good performance in all circumstances can never be attained, but we aim for consistency in as many different market environments as possible. We believe this is the best way to deliver good overall performance over the long term.

Source for company information: Stewart Investors investment team and company data. This stock information does not constitute any offer or inducement to enter into any investment activity. Portfolio data shown is from representative strategy accounts of the strategy shown above. Named new investments disclosed relate to holdings with a portfolio weight over 0.5%. It is not a recommendation or solicitation to purchase or invest in any fund. Differences between the representative account-specific constraints, currency or fees and those of a similarly managed fund or mandate would affect results.

Proxy voting

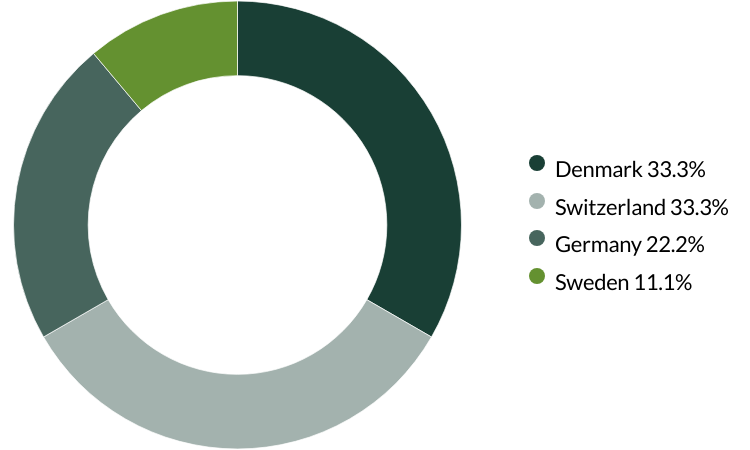

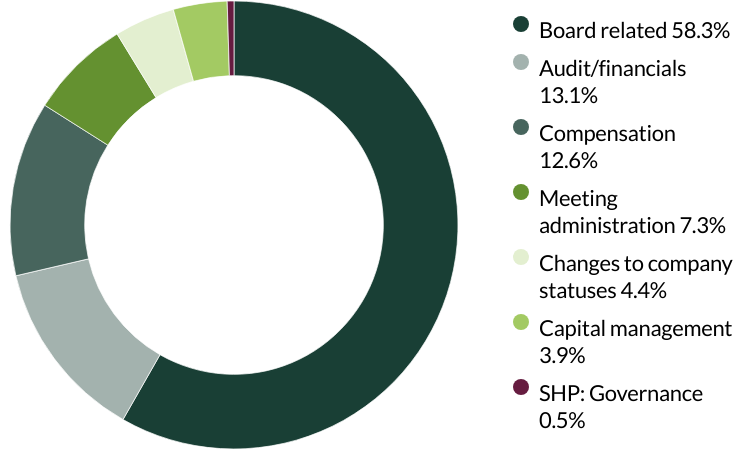

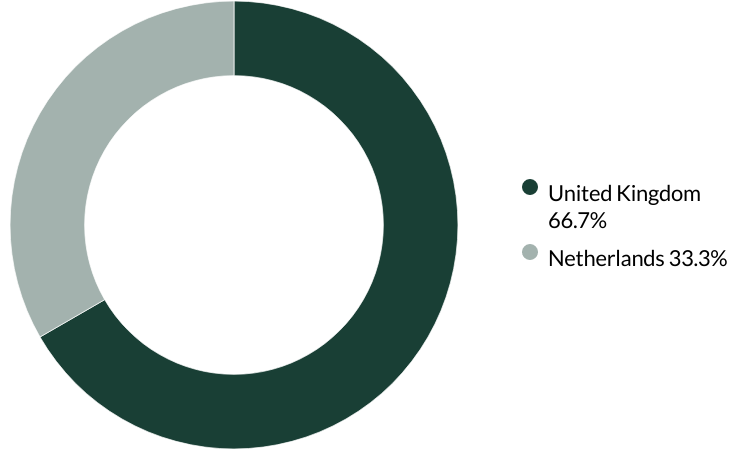

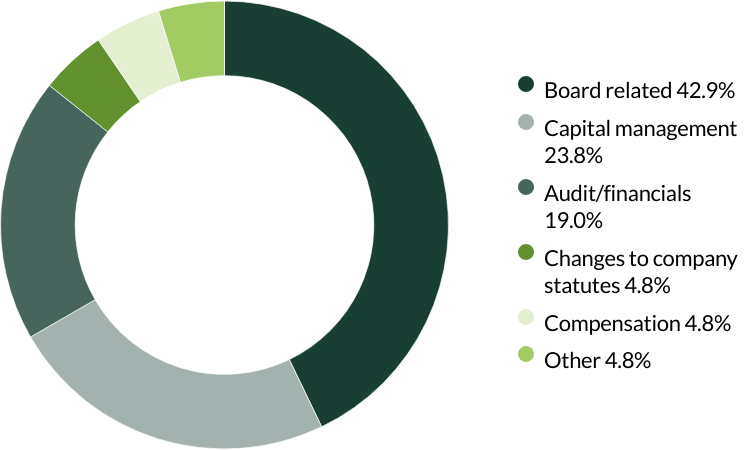

Proxy voting: Q1 2024

European Sustainability proxy voting: 1 January - 31 March 2024

Proxy voting by country of origin

Proxy voting by proposal category

During the quarter there were 206 resolutions from 9 companies to vote on. On behalf of clients, we voted against 10 resolutions.

We voted against an amendment to company articles at Belimo as we do not believe the registered office should be the sole place of jurisdiction for corporate disputes. We also voted against a transaction of other business which would grant unfettered discretion at Belimo and Sika. (three resolutions)

We voted against the appointment of the auditor at Roche as they have been in place for over 10 years. We believe rotating an auditor on a relatively frequent basis (e.g. every 5-10 years) helps to ensure a fresh pair of eyes are examining the accounts and follows best practice. We also voted against excessive executive renumeration. (six resolutions)

We voted against a shareholder proposal concerning a change of payment software at Handelsbanken as we believe the day-to-day operation of the business is best left up to the board and management. (one resolution)

Source for company information: Stewart Investors investment team and company data. This stock information does not constitute any offer or inducement to enter into any investment activity. Portfolio data shown is from representative strategy accounts of the strategy shown above. Proxy voting chart numbers may not add to 100 due to rounding. SHP means: Shareholder Proposal.

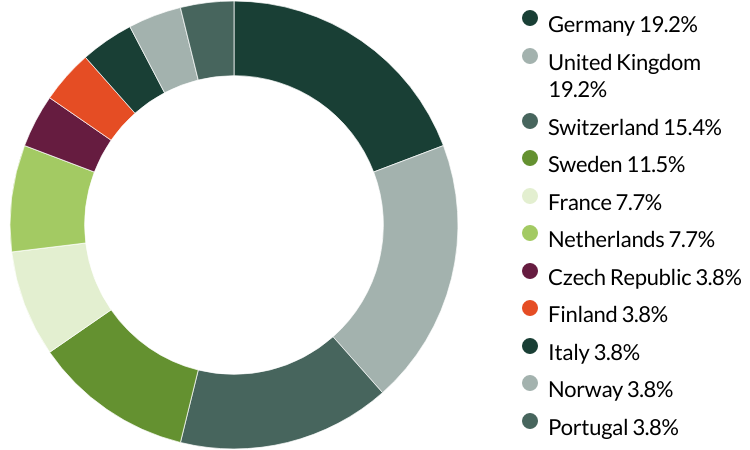

Proxy voting: Q4 2023

European Sustainability proxy voting: 1 October - 31 December 2023

Proxy voting by country of origin

Proxy voting by proposal category

During the quarter there were 28 resolutions from two companies to vote on. On behalf of clients, we didn't vote against any resolutions.

Source for company information: Stewart Investors investment team and company data. This stock information does not constitute any offer or inducement to enter into any investment activity. Portfolio data shown is from representative strategy accounts of the strategy shown above. Proxy voting chart numbers may not add to 100 due to rounding. SHP means: Shareholder Proposal.

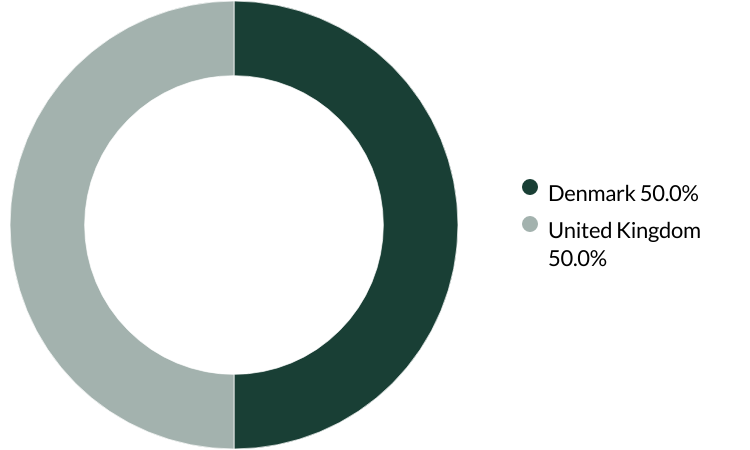

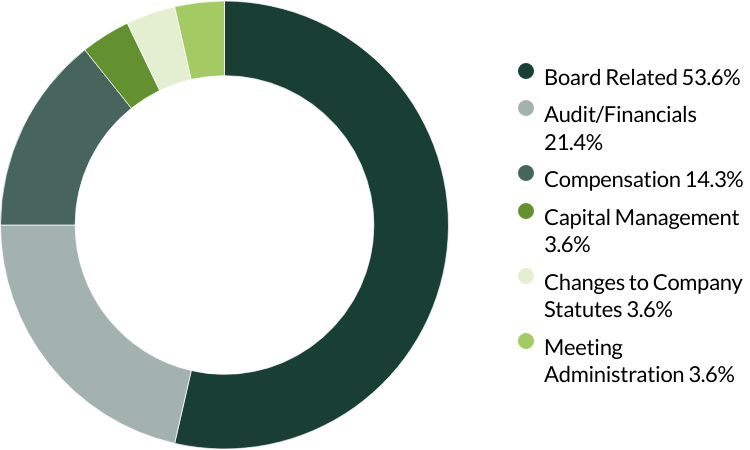

Proxy voting: Q3 2023

European Sustainability proxy voting: 1 July - 30 September 2023

Proxy voting by country of origin

Proxy voting by proposal category

During the quarter there were 42 resolutions from three companies to vote on. On behalf of clients, we voted against one resolution. We voted against DiscoverIE’s request to distribute dividends to shareholders as we would prefer for the cash flows to be reinvested in the company. (one resolution)

Source for company information: Stewart Investors investment team and company data. This stock information does not constitute any offer or inducement to enter into any investment activity. Portfolio data shown is from representative strategy accounts of the strategy shown above. Proxy voting chart numbers may not add to 100 due to rounding. SHP means: Shareholder Proposal.

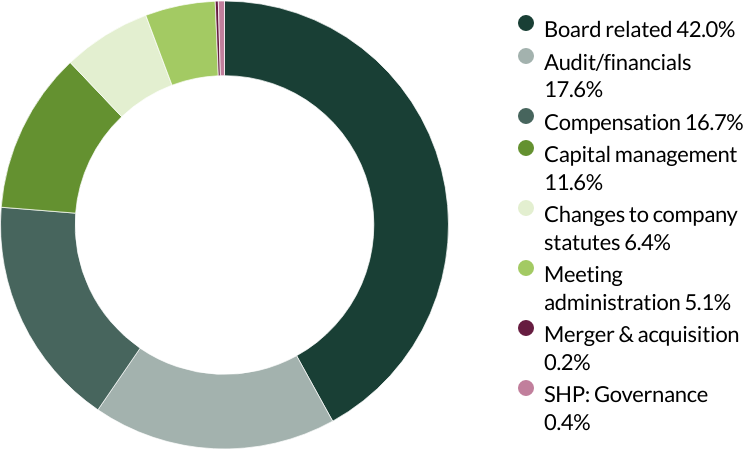

Proxy voting: Q2 2023

European Sustainability proxy voting: 1 April - 30 June 2023

Proxy voting by country of origin

Proxy voting by proposal category

During the quarter there were 455 resolutions from 26 companies to vote on. On behalf of clients, we voted against eight resolutions.

We voted against Alcon’s remuneration report as well as the Board and Executive remuneration, as we believe it is excessive and the company has signalled that they want to keep ratcheting. (three resolutions)

We voted against the appointment of the auditor at Beiersdorf, bioMérieux, Elisa and SFS Group as they have been in place for over 10 years and the companies have given no information on intended rotation. We believe rotating an auditor on a relatively frequent basis (e.g. every 5-10 years) helps to ensure a fresh pair of eyes are examining the accounts, and follows best practice. (four resolutions)

We voted against Unilever’s remuneration report as we have concerns about the magnitude of the increase in the base salary being offered to the new CEO and the lower performance hurdles being set. (one resolution)

Source for company information: Stewart Investors investment team and company data. This stock information does not constitute any offer or inducement to enter into any investment activity. Portfolio data shown is from representative strategy accounts of the strategy shown above. Proxy voting chart numbers may not add to 100 due to rounding. SHP means: Shareholder Proposal.

Portfolio Explorer

If you are unable to view the portfolio explorer, please re-open in Google Chrome, Edge, Firefox, Safari or Opera. IE11 is not supported.

For illustrative purposes only. Reference to the names of example company names mentioned in this communication is merely for explaining the investment strategy and should not be construed as investment advice or investment recommendation of those companies. Companies mentioned herein may or may not form part of the holdings of Stewart Investors. Holdings are subject to change.

Certain statements, estimates, and projections in this document may be forward-looking statements. These forward-looking statements are based upon Stewart Investors’ current assumptions and beliefs, in light of currently available information, but involve known and unknown risks and uncertainties. Actual actions or results may differ materially from those discussed. Readers are cautioned not to place undue reliance on these forward-looking statements. There is no certainty that current conditions will last, and Stewart Investors undertakes no obligation to correct, revise or update information herein, whether as a result of new information, future events or otherwise.

Source: Stewart Investors investment team and company data. Securities mentioned are all investee companies* from representative Asia Pacific Sustainability Strategy, Asia Pacific & Japan Sustainability Strategy, Asia Pacific Leaders Sustainability Strategy, European Sustainability Strategy, European (ex UK) Sustainability Strategy, Global Emerging Markets Leaders Sustainability Strategy, Global Emerging Markets Sustainability Strategy, Indian Subcontinent Sustainability Strategy, Worldwide Sustainability Strategy and Worldwide Leaders Sustainability Strategy accounts as at 30 June 2024. *Assets that the strategies may hold which an active decision has not been made, and sustainability assessment does not apply, include cash, cash equivalents, short-term holdings for the purpose of efficient portfolio management and holdings received as a result of mandatory corporate actions. Holdings of such assets will not appear on Portfolio Explorer.

The Stewart Investors supports the Sustainable Development Goals (SDGs). The full list of SDGs can be found on the United Nations website.

Source for Climate Solutions and impact figures: © 2014–2024 Project Drawdown (drawdown.org). Source for Human Development Pillars: Stewart Investors investment team.

Source for climate solutions and human development analysis and mapping: Stewart Investors investment team. Contributions are defined by the team as demonstrable contributions to any solution, either direct (directly attributable to products, services or practices provided by that company), or enabling (supported or made possible by products or technologies provided by that company).

Investment terms

View our list of investment terms to help you understand the terminology within this document.

Copyright © 2024 Stewart Investors.

Material on this website is intended to provide general information only. Such material does not into account your objectives, financial situation or needs. You should consider these matters before acting on the information and consider the relevant Product Disclosure Statement for any product named on this website before making an investment decision. Any opinions expressed in videos are the opinions of the individual participant and are subject to change without notice. Such opinions are not a recommendation to hold, purchase or sell a particular financial product and may not include all of the information required to make such a decision. Before making any such decision you should consult a financial adviser.