Get the right experience for you. Please select your location and investor type.

Global Emerging Markets All Cap

The Global Emerging Markets All Cap strategy invests in between 30-75 high-quality companies that are contributing to a more sustainable future.

Our Global Emerging Markets All Cap strategy was launched in 2009 and invests in between 30 to 75 high-quality companies that are contributing to a more sustainable future. The strategy’s bottom-up approach allows us to find only the very best businesses from an investable universe of some 65,000 companies. We are looking for companies well positioned to contribute to long-term sustainable development; businesses with high quality management teams, franchises, and financials.

Strategy highlights: a focus on quality and sustainability

- Companies must contribute to sustainable development. Portfolio Explorer >

- We invest in high-quality companies with exceptional cultures, strong franchises and resilient financials. How we pick companies >

- We avoid companies linked to harmful activities and engage and vote for positive change. Our position on harmful products >

- Our approach is long-term, bottom-up, high conviction and benchmark agnostic

- We focus on capital preservation as well as capital growth – we define risk as the permanent loss of client capital

Latest insights

Quarterly updates

Global Emerging Markets All Cap strategy update: 1 January - 31 March 2025

With the threat of US tariffs ever present, the volatility seen across emerging markets in the final quarter of 2024 carried over into 2025. Share prices in India fell sharply due to concerns about a cyclical slowdown. China, by contrast, performed well as investors anticipated a reacceleration in economic growth and began to identify value in many parts of the market. Sentiment was also supported by President Xi, who met executives from a number of private-sector companies.

We added eight new names to the portfolio and sold six. Although it is unusual to see so many names entering and exiting the portfolio, turnover as a percentage of assets under management remained low, at around 9%1. We were, in essence, simply tidying up a number of our smaller positions – the ‘tail’ of the portfolio.

In China, we sold out of Glodon (China: Information Technology) and Hangzhou Robam (China: Consumer Discretionary). These sales were informed by our view of the country’s property market, where we don’t see the issue of oversupply being resolved any time soon. Glodon provides software for construction and development companies. The majority of Hangzhou Robam’s appliances, meanwhile, are sold to housing developers. These sales also allowed us to reallocate the capital to new investment ideas such as Alibaba (China: Consumer Discretionary), S.F. Holding (China: Industrials) and Mindray (China: Health Care).

Alibaba is one of China’s leading e-commerce platforms. It is using the strength of its balance sheet to invest in building its AI capabilities. S.F. Holding has grown into one of China’s leading logistics businesses since its founding in 1992. Its founder remains involved in the day-to-day management of the company. Mindray is a leading medical company. As trade barriers are thrown up around the world, it has the potential to benefit should there be a shift in China towards buying domestically sourced products.

We also added some new names in India while trimming back some others. Share prices in India sold off as the country appeared to be entering a cyclical slowdown. In response, the central bank cut interest rates for the first time since the Covid pandemic in 2020. Valuations in some parts of the market, meanwhile, had begun to appear excessive. We sold out of Godrej Consumer Products (India: Consumer Staples) because it was too expensive for the growth it offered. We sold out of Bajaj Housing Finance (India: Financials) because of liquidity constraints and reallocated the capital into its asset-lite holding company, Bajaj Holdings & Investment (India: Financials) while also establishing a position in sister company Bajaj Auto (India: Consumer Discretionary), a leading manufacturer of motorcycles, scooters and auto rickshaws backed by a high-quality steward.

Other new names in India included Cholamandalam Financial Holdings (India: Financials) and Triveni Turbines (India: Industrials). Cholamandalam is another business associated with the Muragappa family, who we believe to be good stewards of capital. Triveni Turbines, meanwhile, is a leading maker of steam turbines.

We also added a position in Walmart de Mexico (‘Walmex’) (Mexico: Consumer Staples). With the market having taken fright from the elections of Claudia Sheinbaum (in April 2024) and then Donald Trump (in November), Walmex shares had fallen to their lowest multiple since 1996. Despite this, we believe it remains a solid, dependable long-term growth story. The final new name was BDO Unibank (Philippines: Financials) which is the largest bank in the country with a good opportunity to grow in the outlying islands and by developing its digital offering2. We sold Koh Young Technology (South Korea: Information Technology), following a number of missteps in execution and a miss on earnings. We also sold Unicharm (Japan: Consumer Staples). While it has pivoted to adult diapers in response to demographic change, it has found this shift harder than it had originally envisaged.

While we are broadly positive on the outlook for emerging markets, we recognise that there is likely to be ongoing volatility for as long as ‘top-down’ uncertainty – inspired by trade tariffs and geopolitical flux – remains at elevated levels. Valuations are certainly attractive and there remains plenty of domestically driven growth in the markets we favour. Our task is to block out the short-term noise to focus on the underlying quality, growth and stewardship of the companies we invest in.

[1] Source: FactSet as of 31 March 2025.

[2] Source : BDO Unibank – Company Profile (as of 31 December 2024).

Source for company information: Stewart Investors investment team and company data. This stock information does not constitute any offer or inducement to enter into any investment activity. Portfolio data shown is from representative strategy accounts of the strategy shown above. Named new investments disclosed relate to holdings with a portfolio weight over 0.5%. It is not a recommendation or solicitation to purchase or invest in any fund. Differences between the representative account-specific constraints, currency or fees and those of a similarly managed fund or mandate would affect results.

Download a PDF copy

Select Strategy update and/or Proxy voting to produce a report. You can then download a copy of the report by clicking on the button.

You can build a bespoke report for all our strategies on the full Quarterly update report.

Global Emerging Markets All Cap strategy update: 1 October - 31 December 2024

Emerging markets ended 2024 lagging developed markets for the second year in a row. Whilst the MSCI Emerging Markets Index returned 8.1% (USD, total return), developed markets, measured by the MSCI World Index were up 19.2%, driven by strong performance in the United States. Brazil (-29.5%) and Mexico (-26.8%) both had a tough year in 2024 but China, India and Taiwan all posted positive returns1.

Through the last quarter of 2024, markets had to contend with the re-election of Donald Trump and all the expected geopolitical noise that will come over the next four years, as well as the continuing strength of the US dollar. We remain focused on bottom-up stock picking which is at the core of our portfolio construction process and we will continue to seek out long-term growth opportunities regardless of who is the President in the White House.

We added one new position and sold out of two companies through the quarter. We have built a position in Naver (South Korea: Communication Services), the leading South Korean internet search engine with a very strong market share. It was founded inside Samsung SDS before being spun out on its own in 1999. It is still run by the founder, Lee Hae-jin who has recently brought in a new management team which is aiming to return the company to a path of steady and profitable growth. One key aim for them is to use the stickiness of their search engine client base to drive increased e-commerce down the same channels. Their e-commerce business is the second largest in South Korea2. Naver’s attractive valuation presented a good opportunity to invest in a business that should achieve double-digit earnings growth each year.

We sold out of two positions, one of which is Advanced Energy Solution (Taiwan: Industrials). The company makes battery module units for e-bikes and backup servers and after a tough few years, management announced that they could see light at the end of the tunnel with demand from artificial intelligence (AI) coming through from their server clients. We have repeatedly asked for an update call with management without success. Given this lack of communication, we find it difficult to build conviction and have therefore exited the position. We added to Samsung Electronics (South Korea: Information Technology) and AirTAC International (Taiwan: Industrials) with some of the proceeds of this sale.

We also sold Kotak Mahindra Bank (India: Financials) through the quarter. Earlier in the year the bank came under increased regulatory scrutiny because of some lapses in IT security and they were forced to pause issuing some credit cards. Since then, we have had several meetings with the company which have led us to believe that they may continue to struggle especially as competitor public sector banks continue to show marked improvements. We believe there are better opportunities elsewhere in India.

We continue to look for high-quality companies which we can buy at reasonable valuations. We believe that valuations in emerging markets are now at very attractive levels alongside long-term growth opportunities that we can back for the next decade. The team is planning many research trips for 2025 to seek out new investment opportunities and update our knowledge of existing holdings. We look forward to sharing more with you as the year progresses.

1 Source: MSCI Index Factsheets as at 31 December 2024. All data USD, total returns.

2 Source: External market research.

Source for company information: Stewart Investors investment team and company data. This stock information does not constitute any offer or inducement to enter into any investment activity. Portfolio data shown is from representative strategy accounts of the strategy shown above. Named new investments disclosed relate to holdings with a portfolio weight over 0.5%. It is not a recommendation or solicitation to purchase or invest in any fund. Differences between the representative account-specific constraints, currency or fees and those of a similarly managed fund or mandate would affect results.

Global Emerging Markets All Cap strategy update: 1 July - 30 September 2024

Most of the quarter’s activity happened in September, as is often the case. It is in such moments, like the biggest market moves since 2009 in China and Hong Kong and rising geopolitical tensions in the Middle East, that we remain grateful for our long-term philosophy. It gives us the ability to step back in moments of such volatility and reminds us to focus on the more important, bottom-up drivers for the companies we own on your behalf.

Over the course of the quarter, we have sold out of one of our Indian banks. RBL Bank (India: Financials), which we purchased in December 2023. The new management team seemed determined to move the bank towards less risky (more secured) lending which at 1x price-to-book (P/B)1 appeared attractively priced. Unfortunately, the quarter after we purchased the company, it became clear that unsecured bank loans had been growing at over 30% and the path to a more balanced loan portfolio would be a lot longer than we had expected. Added to that, we are seeing a few banks that are struggling to grow their deposit base which impacts how they can fund their loan growth. For many years, most depositors avoided the public sector banks fearing either insolvency or potential loss of deposits. They have been cleaned up and professionalised which is great for the Indian saver and borrower but tougher for the private sector banks who benefitted from weak competition in the public sector. With prospects for RBL looking riskier and with better ideas elsewhere, we decided to exit.

We exited Yifeng Pharmacy Chain (China: Consumer Staples) which was another name where we were becoming worried about increased regulatory oversight having a negative impact on profit margins. We are confident that they will continue to roll up the pharmacy sector in China – in much the same way that RaiaDrogasil (Brazil: Consumer Staples) is doing in Brazil – but we worry that Beijing could well impose price cuts on those drugs purchased through medical insurance plans.

We also fully sold out of Clicks (South Africa: Consumer Staples), another pharmacy chain. Growth has been phenomenal at this business with new store openings continuing apace and a better mix of basket driving profitability. However, with our focus on delivering strong absolute returns, we struggled to see Clicks growing into these valuations and decided to reallocate the capital into more attractively priced ideas elsewhere. We think Clicks remains a very high-quality business, one that we would look forward to owning again at more reasonable valuations.

Finally, we sold Integrated Diagnostics (Egypt: Health Care) due to liquidity risks and to fund higher conviction ideas elsewhere.

We did not make new complete purchases in the quarter.

We continue to discuss our China holdings at length, especially in light of the recent market moves. But another area where we are doing a lot of thinking is Poland. Here we hold Allegro (Poland: Consumer Discretionary), Dino Polska (Poland: Consumer Staples) and Jerónimo Martins (Portugal: Consumer Staples), which is listed in Portugal but >50% of revenues are from its Biedronka business in Poland.2 They all experienced strong growth through 2022 and 2023 as inflation helped them increase profit margin but the opposite has now happened. Deflation in food prices and rising costs have squeezed profit margins considerably.

As always, we spend the bulk of our time continuing to better understand the quality attributes of the companies we invest in and finding similarly resilient ideas to add to the portfolio.

1 Source: Bloomberg Finance L.P.

2 Source: Jerónimo Martins Annual Report 2023

Source for company information: Stewart Investors investment team and company data. This stock information does not constitute any offer or inducement to enter into any investment activity. Portfolio data shown is from representative strategy accounts of the strategy shown above. Named new investments disclosed relate to holdings with a portfolio weight over 0.5%. It is not a recommendation or solicitation to purchase or invest in any fund. Differences between the representative account-specific constraints, currency or fees and those of a similarly managed fund or mandate would affect results.

Global Emerging Markets All Cap strategy update: 1 April - 30 June 2024

We have seen a continuation of geopolitical surprises throughout the quarter which have impacted investor sentiment causing near-term volatility.

Claudia Sheinbaum was elected the first female President of Mexico with such a resounding victory that her party now holds a two-thirds majority in both congressional houses, which means it could make constitutional changes such as the proposal that Supreme Court judges would be directly elected by popular vote. India completed the largest democratic election in the world with a surprise vote removing Narendra Modi and the Bharatiya Janata Party’s absolute majority in the Lok Sabha (also known as the House of the People and the lower house in the Indian Parliament). The Nifty 50 (top 50 stocks by market capitalisation listed on the National Stock Exchange of India) rose the day before the election on the expectation that Modi would get over 400 seats. It then fell 7% when the news broke that he had lost his absolute majority before rising again in the days afterwards as the market decided Modi staying in power with a reduced majority was a positive for Indian democracy1. It is at times like this that we are thankful for our philosophy and bottom-up stock picking process with a focus on quality and a 10-year time horizon on growth, allowing us to take advantage of irrational price movements.

We sold out of seven companies and only added one through the second quarter which is higher turnover than previous quarters. We sold Amoy Diagnostics (China: Health Care) after a period of better performance. Whilst we still like the way the business is managed, the high operating margins (c.27%) generated in the healthcare sector means we have become worried about the regulatory environment potentially aiming to reduce those margins. We sold Kingmed Diagnostics (China: Health Care) for the same reason and both Amoy and Kingmed are good examples of where top-down or macro views on a country and sector can break an investment case.

We also sold Tech Mahindra (India: Information Technology) and Dabur (India: Consumer Staples) having bought into both in 2009. Tech Mahindra (known then as Satyam) and Dabur have delivered mid-teen annual performance since first bought. Whilst we still believe that they are good companies, valuations are becoming problematic. Tech Mahindra has been a great investment over the last ten years but we believe we have a better option for the next ten years in Tata Consultancy Services (India: Information Technology). Tech Mahindra has seen margins reduce and it is also expensive. Dabur is a soaps and detergents producer in India which has delivered high earnings but we expect growth to be lower in the future. Valuations in India remain one of our biggest concerns and we have been trimming back our positions there including Marico (India: Consumer Staples) and Mahindra & Mahindra (India: Consumer Discretionary) due to valuations. We also sold Pigeon (Japan: Consumer Staples) as we lost conviction in the speed and extent of the evolution of the franchise which is facing rising headwinds such as declining birth rates.

Finally we sold out of Banco Bradesco (Brazil: Financials) and Infineon Technologies (Germany: Information Technology). Infineon is a semiconductor designer and manufacturer mainly serving the automotive sector (c.45% of revenues2) and it is moving into software solutions, but we feel there are better ideas elsewhere. Banco Bradesco was a mistake which we are rectifying by exiting the position. We underestimated the impact of Nubank (a financial technology bank, known as a neobank) on the country’s banking sector and Banco Bradesco is clearly late in providing fintech and more advanced digital banking services. To compete, the company is going to have to undertake a massive amount of organisational and cultural change at a time when Brazil’s economy is looking precarious with inflation potentially beginning to reappear.

The only new company we have purchased is MediaTek (Taiwan: Information Technology), a leading fabless (outsources production) design house in Asia. It has followed TSMC in its relentless focus on quality though it has arguably been more focused on the affordability of technology, helping to provide innovative solutions to many global development challenges and democratising technology. Barriers to entry are getting higher with faster product cycles and longer lead times in terms of design but they have access to great designers in Taiwan. The company has sound financials and good management and we aim to hold this company for the long term.

We have been selectively adding to some positions in technology companies where we took advantage of price movements to continue building a long-term position. We added to Samsung Electronics (South Korea: Information Technology) as we believe it is in the early stages of a memory cycle recovery. We also added to Globant (Argentina: Information Technology) which suffered as IT capital expenditure (capex) was postponed by several customers, but growth has held up better than we expected and we don’t see it as too expensive.

1 Source: Bloomberg

2 Source: Stewart Investors investment team and company data

Source for company information: Stewart Investors investment team and company data. This stock information does not constitute any offer or inducement to enter into any investment activity. Portfolio data shown is from representative strategy accounts of the strategy shown above. Named new investments disclosed relate to holdings with a portfolio weight over 0.5%. It is not a recommendation or solicitation to purchase or invest in any fund. Differences between the representative account-specific constraints, currency or fees and those of a similarly managed fund or mandate would affect results.

Proxy voting

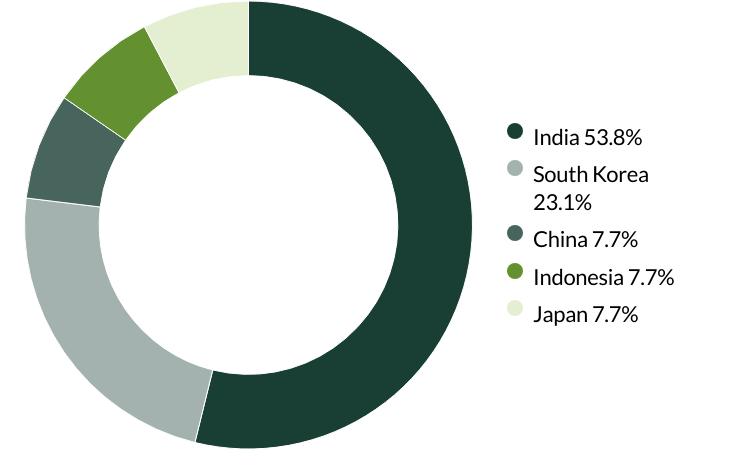

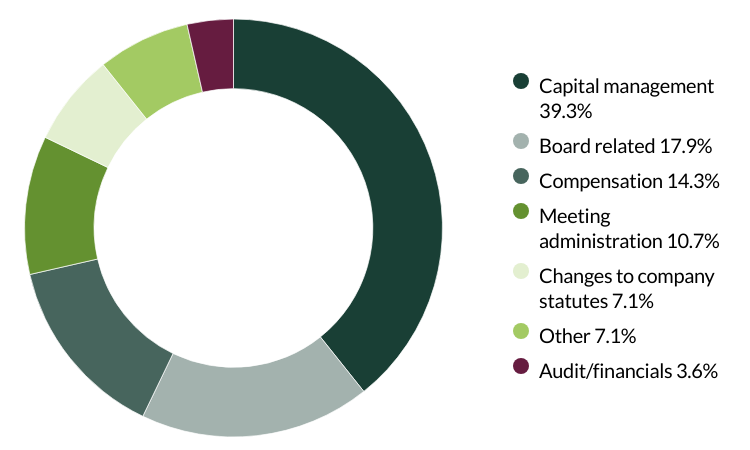

Global Emerging Markets All Cap proxy voting: 1 January - 31 March 2025

Proxy voting by country of origin

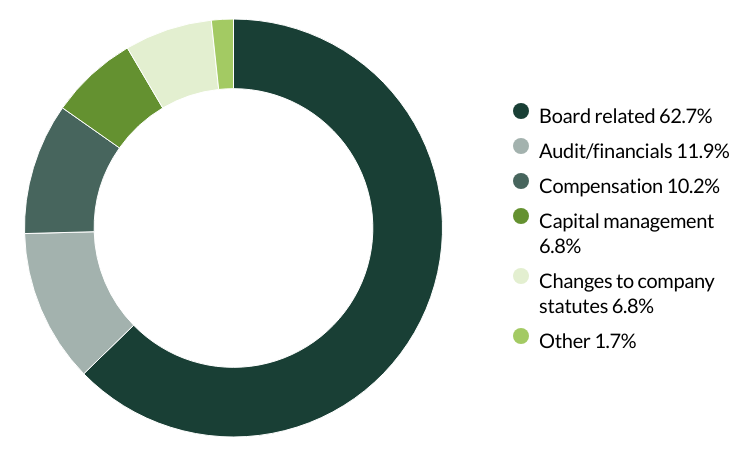

Proxy voting by proposal category

During the quarter there were 59 resolutions from 12 companies to vote on. On behalf of clients, we voted against six resolutions.

We voted against executive remuneration at Bank Central Asia because we believed it was excessive. (one resolution)

We voted against the election of a director and their remuneration at IndiaMART as we seek to encourage greater diversity and independence on the board. (one resolution)

We voted against the election of two directors and an audit committee member at Samsung Electronics as we do not believe them to be truly independent. (three resolutions)

We voted against the election of the audit committee chair at Unicharm as we do not believe they are independent. (one resolution)

Source for company information: Stewart Investors investment team and company data. This stock information does not constitute any offer or inducement to enter into any investment activity. Portfolio data shown is from representative strategy accounts of the strategy shown above. Proxy voting chart numbers may not add to 100 due to rounding. SHP means: Shareholder Proposal.

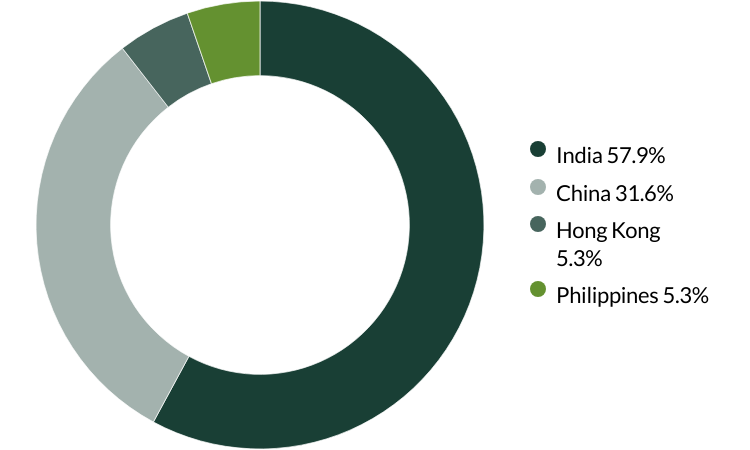

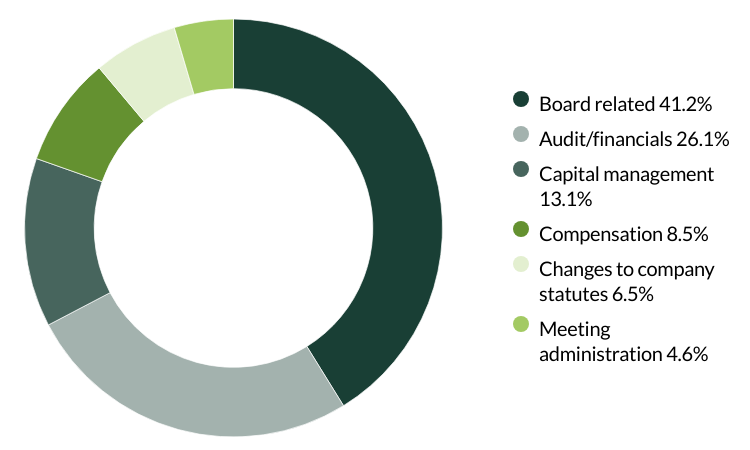

Global Emerging Markets All Cap proxy voting: 1 October - 31 December 2024

Proxy voting by country of origin

Proxy voting by proposal category

During the quarter there were 28 resolutions from eight companies to vote on. On behalf of clients, we did not vote against any resolutions.

Source for company information: Stewart Investors investment team and company data. This stock information does not constitute any offer or inducement to enter into any investment activity. Portfolio data shown is from representative strategy accounts of the strategy shown above. Proxy voting chart numbers may not add to 100 due to rounding. SHP means: Shareholder Proposal.

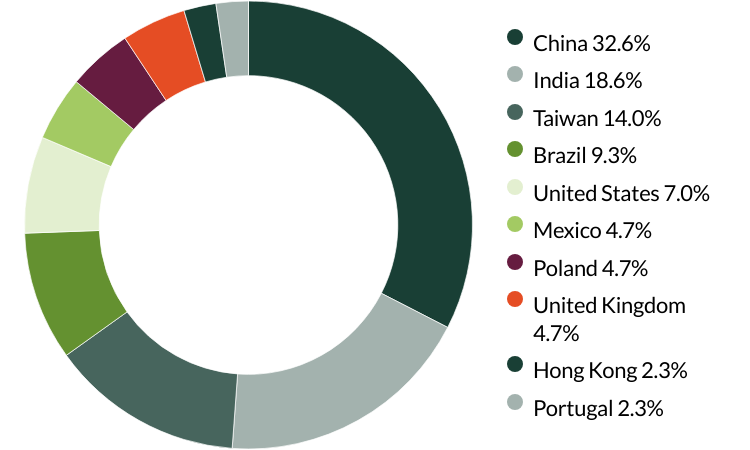

Global Emerging Markets All Cap proxy voting: 1 July - 30 September 2024

Proxy voting by country of origin

Proxy voting by proposal category

During the quarter there were 153 resolutions from 17 companies to vote on. On behalf of clients, we voted against three resolutions.

We voted against the appointment of the auditor at Philippine Seven as they have been in place for over ten years. The company has given no information on intended rotation which we believe is important for ensuring a fresh perspective on the accounts. We also voted against proposals on transaction of business, as the company did not provide enough information about the proposals. We wanted to avoid giving them unrestricted decision-making power without sufficient clarity. (two resolutions)

We voted against the appointment of the auditor at Vitasoy as they have been in place for over ten years. The company has given no information on intended rotation which we believe is important for ensuring a fresh perspective on the accounts. (one resolution)

Source for company information: Stewart Investors investment team and company data. This stock information does not constitute any offer or inducement to enter into any investment activity. Portfolio data shown is from representative strategy accounts of the strategy shown above. Proxy voting chart numbers may not add to 100 due to rounding. SHP means: Shareholder Proposal.

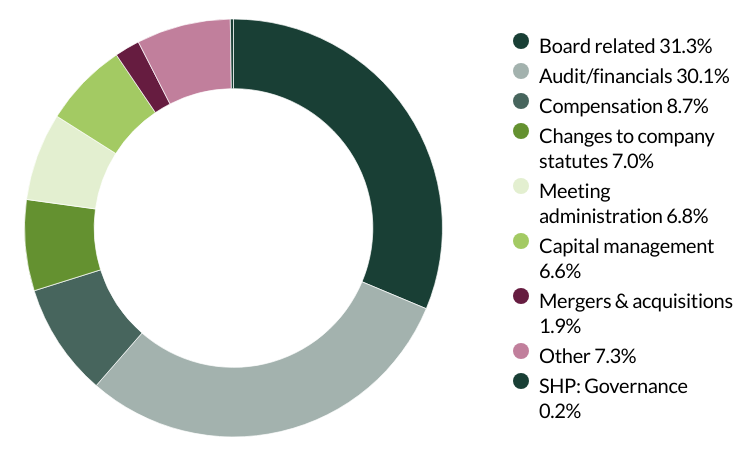

Global Emerging Markets All Cap proxy voting: 1 April - 30 June 2024

Proxy voting by country of origin

Proxy voting by proposal category

During the quarter there were 412 resolutions from 38 companies to vote on. On behalf of clients, we voted against 14 resolutions.

We abstained from voting on amendments to work systems for independent directors and board meeting procedures at Amoy Diagnostics as the company did not provide sufficient data on the proposed amendments. (two resolutions)

We voted against the appointment of the auditor at EPAM Systems, Glodon, Yifeng Pharmacy Chain and Zhejiang Supor as they have been in place for over 10 years and the companies’ have given no information on intended rotation. We believe rotating an auditor on a relatively frequent basis (e.g. every 5-10 years) helps to ensure a fresh pair of eyes are examining the accounts, and follows best practice. (four resolutions)

We voted against the proposed employee stock ownership plan at Midea as we believe non-executive director involvement could lead to conflict of interest and would not be in shareholders' interest. (three resolutions)

We abstained from voting on amendments to articles at Quálitas as the company did not provide sufficient information on the amendments. (one resolution)

We voted against the recasting of votes for the supervisory council at RaiaDrogasil as we believe the principle of recasting votes for an amended slate is poor practice and would prefer the slate to be resubmitted for voting. (one resolution)

We abstained from voting on a series of proposals regarding capital and shares allocation and board elections and reports at Regional as the company provided insufficient information. (12 resolutions)

We voted against the establishment of a supervisory council and cumulative voting at TOTVS as no detail on the candidates was provided. (two resolutions)

We voted against recasting and cumulative voting at WEG as this would allow the board to make changes without shareholder assessment or knowledge of candidates. (three resolutions)

We abstained from voting on requests for a separate board election and the election of a Supervisory Council position at WEG due to insufficient information and our preference for the current family stewards to remain in place. (two resolutions)

We voted against a shareholder proposal regarding board declassification at EPAM Systems as we do not deem it necessary for all directors to stand for election annually and believe this could destabilise the board by allowing excessive turnover. (one resolution)

Source for company information: Stewart Investors investment team and company data. This stock information does not constitute any offer or inducement to enter into any investment activity. Portfolio data shown is from representative strategy accounts of the strategy shown above. Proxy voting chart numbers may not add to 100 due to rounding. SHP means: Shareholder Proposal.

Portfolio Explorer

If you are unable to view the portfolio explorer, please re-open in Google Chrome, Edge, Firefox, Safari or Opera. IE11 is not supported.

For illustrative purposes only. Reference to the names of example company names mentioned in this communication is merely for explaining the investment strategy and should not be construed as investment advice or investment recommendation of those companies. Companies mentioned herein may or may not form part of the holdings of Stewart Investors. Holdings are subject to change.

Certain statements, estimates, and projections in this document may be forward-looking statements. These forward-looking statements are based upon Stewart Investors’ current assumptions and beliefs, in light of currently available information, but involve known and unknown risks and uncertainties. Actual actions or results may differ materially from those discussed. Readers are cautioned not to place undue reliance on these forward-looking statements. There is no certainty that current conditions will last, and Stewart Investors undertakes no obligation to correct, revise or update information herein, whether as a result of new information, future events or otherwise.

Source: Stewart Investors investment team and company data. Securities mentioned are all investee companies* from representative Asia Pacific All Cap Strategy, Asia Pacific & Japan All Cap Strategy, Asia Pacific Leaders Strategy, European All Cap Strategy, European (ex UK) All Cap Strategy, Global Emerging Markets (ex China) Leaders Strategy, Global Emerging Markets Leaders Strategy, Global Emerging Markets All Cap Strategy, Indian Subcontinent All Cap Strategy, Worldwide All Cap Strategy and Worldwide Leaders Strategy accounts as at 31 March 2025. *Assets that the strategies may hold which an active decision has not been made, and sustainability assessment does not apply, include cash, cash equivalents, short-term holdings for the purpose of efficient portfolio management and holdings received as a result of mandatory corporate actions. Holdings of such assets will not appear on Portfolio Explorer.

The Stewart Investors supports the Sustainable Development Goals (SDGs). The full list of SDGs can be found on the United Nations website.

Source for Climate Solutions and impact figures: © 2014–2025 Project Drawdown (drawdown.org). Source for Human Development Pillars: Stewart Investors investment team.

Source for climate solutions and human development analysis and mapping: Stewart Investors investment team. Contributions are defined by the team as demonstrable contributions to any solution, either direct (directly attributable to products, services or practices provided by that company), or enabling (supported or made possible by products or technologies provided by that company).

Investment terms

View our list of investment terms to help you understand the terminology within this website.

Investment involves risks. This website is issued by First Sentier Investors (Singapore) whose company registration number is 196900420D and has not been reviewed by the Monetary Authority of Singapore. First Sentier Investors (registration number 53236800B) and Stewart Investors (registration number 53310114W) are the business divisions of First Sentier Investors (Singapore).

Copyright © 2025 Stewart Investors.